SEO Title: Multifamily Cap Rates Explained: Analysis & Trends for Investors

Meta Description: A complete guide to multifamily cap rates. Learn the formula, what drives rates, and how to use this metric for valuation, underwriting, and portfolio analysis.

Meta Keywords: multifamily cap rates, what is a good cap rate, cap rate formula, cap rate trends, commercial real estate, noi calculation, property valuation

A multifamily cap rate is the property's unlevered annual return on investment, calculated as if it were purchased with all cash. For investors, it's the single most critical vital sign for a property's financial health, representing the raw yield before factoring in any financing. Understanding this metric is non-negotiable for anyone serious about real estate.

This guide delivers the essential framework for using multifamily cap rates for deal analysis and valuation. You will learn the formula, the market drivers, and the practical applications that separate professional investors from amateurs.

| Key Takeaway | Description |

|---|---|

| Core Definition | The Net Operating Income (NOI) divided by the property's market value. |

| Risk Indicator | A low cap rate (e.g., 4-5%) signals lower risk and higher value; a high cap rate (e.g., 7%+) signals higher risk and lower value. |

| Industry Standard | It's an unlevered metric, allowing for "apples-to-apples" comparisons between properties regardless of financing. |

| Practical Use | Essential for property valuation, deal underwriting, and strategic portfolio management. |

Mastering the cap rate is the foundation of sophisticated multifamily investment analysis.

What is the function of a multifamily cap rate?

The primary function of a multifamily cap rate, or capitalization rate, is to serve as a valuation metric that allows for the rapid comparison of different real estate investments. It represents the potential rate of return on an investment based solely on the income the property is expected to generate, expressed as a percentage.

Essentially, the cap rate is the property's annual Net Operating Income (NOI) divided by its current market value or purchase price. This simple formula provides a powerful snapshot of performance, allowing investors to assess a deal's profitability relative to its cost.

The cap rate quantifies how the market values an income stream's reliability. A lower cap rate means investors are paying a premium for certainty.

The calculation depends entirely on two key components: income and value.

Cap Rate Components

| Component | Definition | Impact on Cap Rate |

|---|---|---|

| Net Operating Income (NOI) | The property's total annual income (rent, fees) minus all operating expenses (taxes, insurance, maintenance). | Higher NOI increases the cap rate, signaling stronger profitability. |

| Market Value / Price | The current purchase price or estimated market value of the property. | A lower price for the same NOI results in a higher cap rate. |

| The Cap Rate (%) | The final percentage (NOI ÷ Value), representing the unlevered annual return. | Indicates the relationship between income and value; used for comparison. |

Understanding these pieces is the foundation for analyzing any multifamily deal.

The Risk and Return Relationship

A property's cap rate directly reflects its position on the risk-return spectrum. An inverse relationship exists between a property's perceived risk and its cap rate—a dynamic every investor must grasp. A lower cap rate implies a higher valuation and is typically associated with lower-risk, more stable assets. A higher cap rate suggests a lower valuation and often signals a higher-risk, higher-return opportunity.

- Lower Cap Rates (e.g., 4-5%): Often found in prime locations with new, Class A buildings. Investors pay a premium for stability, predictable cash flow, and high-quality tenants.

- Higher Cap Rates (e.g., 7-8%+): More common for older, Class C buildings in secondary or tertiary markets. These properties might require significant capital improvements or have less stable tenancy, offering greater potential upside but with more risk.

Industry Standard Metric

The multifamily cap rate is the universal language of commercial real estate investors, brokers, and lenders because it is unlevered. By excluding debt service from the calculation, it measures the property's intrinsic performance on a level playing field.

This allows for a true "apples-to-apples" comparison between different properties, regardless of how an individual buyer plans to finance their purchase. It isolates the asset's operational efficiency from the investor's capital structure, making it the purest indicator of value.

How do you calculate a multifamily cap rate?

The multifamily cap rate is calculated using the formula: Net Operating Income (NOI) ÷ Current Market Value. The result is a percentage that shows the asset's unlevered annual return. While the formula is simple, its accuracy depends entirely on the integrity of the NOI and value figures used.

This calculation is the bedrock of professional real estate underwriting.

Step 1: Determine Net Operating Income (NOI)

NOI is the property’s total income minus all necessary operating expenses. To find it, you must first calculate the Gross Potential Income (GPI)—the maximum rent you could collect if the property were 100% occupied. From GPI, subtract an allowance for vacancy and credit losses to arrive at the Effective Gross Income (EGI).

From EGI, you subtract all operating expenses. Common expenses include:

- Property Taxes: Annual assessment from the local municipality.

- Insurance: Premiums for liability and property coverage.

- Property Management Fees: Typically 3-5% of EGI for third-party management.

- Repairs & Maintenance: Budget for routine upkeep and repairs.

- Utilities: Costs for common areas not billed back to tenants.

- Administrative & Marketing: Costs to run the office and find new tenants.

Critical Distinction: Debt service (mortgage payments) is never included in operating expenses. The cap rate is an unlevered metric, measuring the property's performance independent of financing. This is what allows for direct comparisons between properties.

Step 2: Find the Current Market Value

The other half of the equation is the property’s value. This is either the purchase price for a new acquisition or the current market value for an existing asset. Investors use comparable sales data ("comps") or specialized real estate valuation software to determine an accurate market value.

A Practical Calculation Example

Consider a hypothetical 20-unit apartment building:

Calculate Gross Potential Income (GPI):

- 20 units x $1,500/month rent = $30,000/month

- $30,000/month x 12 months = $360,000 GPI

Calculate Effective Gross Income (EGI):

- Assume a 5% vacancy and credit loss: $360,000 x 0.05 = $18,000

- $360,000 (GPI) – $18,000 (Loss) = $342,000 EGI

Calculate Net Operating Income (NOI):

- Assume total annual operating expenses are $120,000.

- $342,000 (EGI) – $120,000 (Expenses) = $222,000 NOI

Calculate the Cap Rate:

- Assume the purchase price (Market Value) for this property is $4,036,363.

- $222,000 (NOI) ÷ $4,036,363 (Value) = 0.055

- The multifamily cap rate is 5.5%.

This 5.5% cap rate now serves as the benchmark to compare this deal against other market opportunities. For more detailed breakdowns, it’s worth reviewing advanced methods on how to calculate cap rates for various scenarios.

What factors drive multifamily cap rates?

Multifamily cap rates are driven by macroeconomic forces that set baseline returns and microeconomic factors that price in property-specific risk and growth potential. Understanding these drivers is essential for accurately interpreting market conditions.

Macroeconomic Drivers

These large-scale economic forces influence the cost of capital and the relative attractiveness of real estate as an asset class.

| Driver | Description | Impact on Cap Rates |

|---|---|---|

| Interest Rates | The cost of borrowing set by central banks (e.g., the Federal Reserve). | Higher interest rates increase debt costs, pushing cap rates up as investors demand higher yields. |

| 10-Year Treasury Yield | The return on a U.S. government bond, considered the "risk-free rate of return." | An increase in the Treasury yield forces cap rates up to maintain a sufficient "risk premium" for real estate. |

| Capital Flows | The amount of domestic and foreign capital seeking to invest in multifamily real estate. | High capital availability increases competition and property prices, which compresses (lowers) cap rates. |

| Economic & Job Growth | The health of the overall economy, measured by GDP and employment statistics. | Strong economic growth boosts rental demand and NOI, leading to lower cap rates as investors pay more for quality assets. |

Our guide on how inflation impacts real estate investments explores these dynamics in greater detail.

Microeconomic & Property-Specific Factors

These factors relate to the specific location and physical characteristics of the asset, fine-tuning its cap rate based on perceived risk.

An asset's cap rate is a direct reflection of its perceived risk and future growth potential. Every detail, from the building's age to its location, contributes to this perception.

For example, a CohnReznick analysis of CoStar data shows that national multifamily cap rates jumped by 83 basis points from 2022 to 2023. This was a direct response to the Federal Reserve's aggressive rate hikes, which sent the federal funds rate from near 0% to over 5.25%, demonstrating how a macro driver directly impacts valuations.

The table below breaks down how these micro-level factors influence risk and, consequently, the cap rate.

| Factor | Lower Cap Rate (Lower Risk) | Higher Cap Rate (Higher Risk) |

|---|---|---|

| Asset Class | Class A: New construction, premium amenities, prime locations. | Class C: Older buildings (30+ years), deferred maintenance, basic amenities. |

| Location Tier | Primary Market: Major metro areas like NYC or Los Angeles with high liquidity. | Tertiary Market: Smaller cities with less diverse economies and fewer investors. |

| Property Age | New Construction (0-10 years): Lower maintenance costs, high tenant demand. | Older Vintage (20+ years): Higher capital expenditure needs, potential obsolescence. |

| Rent Growth | High Growth Potential: Located in a rapidly growing submarket with rising wages. | Stagnant or Declining: Area with flat population growth or new supply competition. |

| Tenant Profile | High-income professionals: Stable employment, low turnover. | Lower-income tenants: More sensitive to economic downturns, higher turnover. |

A brand-new luxury high-rise in New York City will trade at a much lower cap rate than a 40-year-old apartment complex in a tertiary market. The market prices the first for its stability and predictability, while the second must offer a higher potential return to compensate for its greater risk.

What are the historical trends for multifamily cap rates?

Historical data shows that multifamily cap rates are highly sensitive to monetary policy and investor sentiment, moving through distinct cycles of expansion and compression. Understanding these cycles provides crucial context for evaluating the current market and anticipating future shifts.

The last 15 years have been defined by the cost of debt and shifting risk tolerance.

The Post-Crisis Expansion (2009-2011)

Following the 2008 Global Financial Crisis, credit markets froze and risk aversion was high. Investors demanded significantly higher returns to compensate for the perceived risk, pushing multifamily cap rates up as the market began a slow recovery. This period of caution set the stage for a prolonged cycle of change driven by new economic forces.

A Decade of Compression (2012-2021)

This period was characterized by historically low interest rates and strong demographic-driven rental demand. The flood of cheap capital created a perfect storm for multifamily real estate, resulting in a long, steady period of cap rate compression, where rates consistently declined.

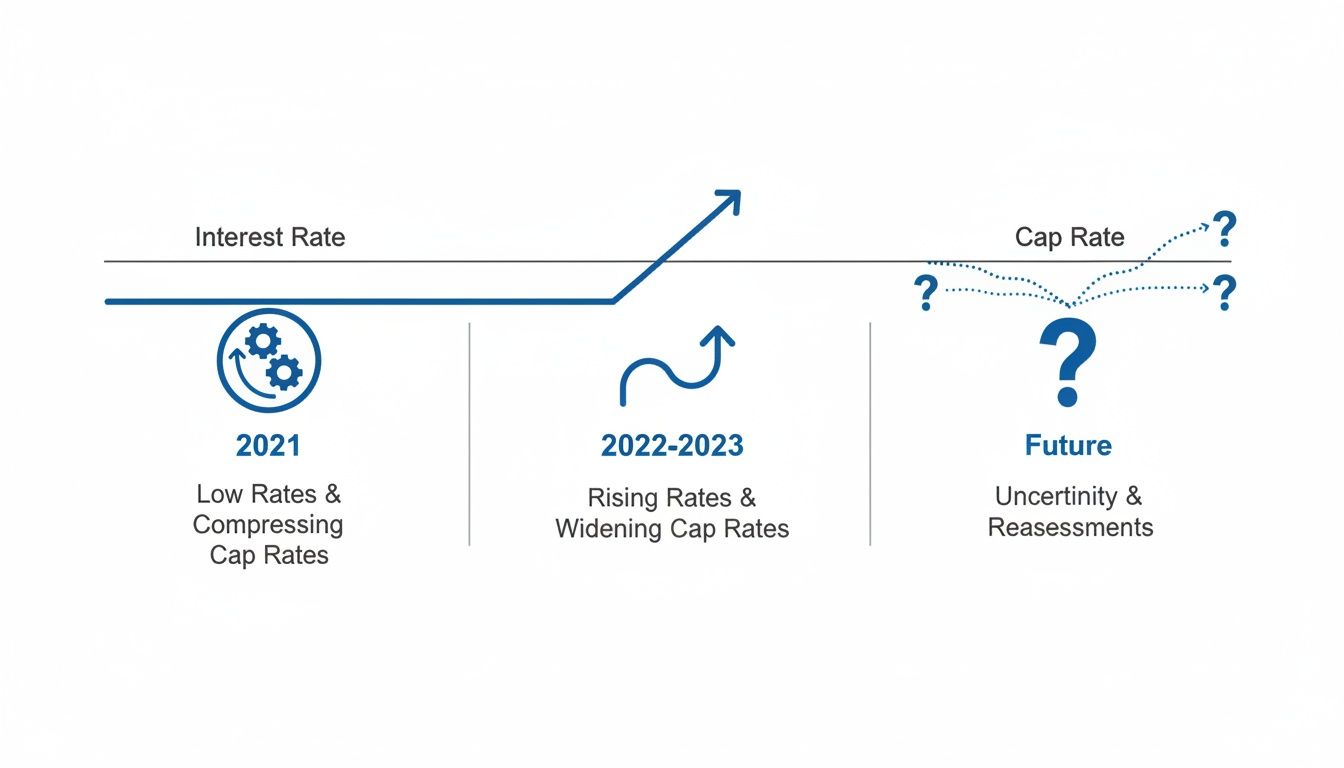

This trend peaked in 2021. According to data from CBRE and Green Street, a decade of recovery and massive capital inflows squeezed average cap rates down to a historic low of 4.1%. However, the pendulum swung back aggressively as the Federal Reserve began hiking rates. Cap rates have since climbed to 5.2%, a full 110 basis point jump. You can read more about these multi-family market fluctuations.

The timeline below illustrates this dramatic shift.

This visual shows the market tightening in 2021, the sharp rate hikes of 2022-2023, and the subsequent period of uncertainty.

The Great Recalibration (2022-Present)

The era of cheap money ended abruptly in 2022 when the Federal Reserve launched an aggressive rate-hiking campaign to combat inflation. This event triggered the "Great Recalibration" in the multifamily market.

- Rapid Expansion: As borrowing costs skyrocketed, investors could no longer justify the low cap rates of the prior year. This forced cap rates to expand (increase) to offer a sufficient return over the new cost of debt.

- Price Discovery: A significant gap emerged between buyer and seller expectations, causing transaction volume to plummet. The market entered a prolonged period of "price discovery" to find a new equilibrium.

- Shift to Fundamentals: With cap rate compression no longer a viable return driver, investors were forced to focus on operational excellence—driving NOI through superior management, expense control, and organic rent growth.

The primary lesson from this cycle is that multifamily cap rates are directly and powerfully linked to monetary policy. They reflect not just a property's income but the broader financial environment in which that income is valued.

How are cap rates used in investment analysis?

For sophisticated investors, the cap rate is not just a calculation but a versatile tool used to drive decisions in property valuation, deal underwriting, and portfolio management. Its true power lies in its application as a universal yardstick for comparing risk and value across different assets and markets.

Application 1: Property Valuation

The most common use of a cap rate is to quickly determine a property's value. By applying the prevailing market cap rate to a property's Net Operating Income (NOI), an investor can arrive at a solid initial valuation.

The formula is a simple rearrangement of the original: Value = NOI ÷ Cap Rate.

For example, if a property generates $250,000 in NOI and comparable buildings in the area are trading at a 5.0% cap rate, the estimated value is $5 million ($250,000 ÷ 0.05). This serves as an immediate sanity check against a seller's asking price.

Application 2: Deal Underwriting

Underwriting involves a deep analysis of a potential investment, and the cap rate is the primary tool. Comparing a target property’s cap rate to market benchmarks immediately reveals whether it is an underpriced opportunity or an overvalued liability.

| Cap Rate Type | Definition | Strategic Consideration |

|---|---|---|

| In-Place Cap Rate | Based on the property's actual, historical performance (trailing 12 months). | This is the true, current unlevered return. Use it as the baseline for all analysis. |

| Pro-Forma Cap Rate | Based on a forecast of potential income after planned improvements or rent increases. | This represents the potential upside. The gap between the in-place and pro-forma cap rates is where the value-add opportunity lies. |

If a property’s cap rate is significantly higher than the market average, an investor must determine why—it could signal deferred maintenance, poor management, or a distressed location. Conversely, a cap rate well below the market average suggests the property is either overpriced or a premium, stabilized asset commanding a lower return. A firm grasp of how to effectively price rental properties is essential, as rent levels are the primary driver of NOI.

Application 3: Portfolio Management

For asset owners, cap rates are a dynamic tool for strategic portfolio management. Monitoring cap rate trends helps determine the optimal time to hold, sell, or refinance a property.

- Cap rate compression (falling rates) increases a property's value, creating equity. This is an owner's best friend.

- Cap rate expansion (rising rates) erodes a property's value, which may signal a good time to sell or reposition an asset.

Imagine you acquired a property at a 7.0% cap rate. If the market heats up and similar properties now trade at a 5.5% cap rate, your building's value has increased significantly. This creates a strategic choice: sell to lock in profits, or refinance to extract the newly created equity tax-free and redeploy it into another investment.

Platforms like BatchData provide the deep property and owner data needed to find accurate comps and market data. This allows investors to benchmark their portfolios professionally and spot opportunities others miss. To take the next step, use our guide to find profitable multifamily markets using data.

What are the future projections for multifamily cap rates?

The consensus forecast for multifamily cap rates points toward a period of slow, gradual compression over the next 12 to 24 months, though this projection is heavily dependent on Federal Reserve policy and credit market stability. After a prolonged period of paralysis, the market is expected to find a new equilibrium.

This cautious optimism follows an unprecedented phase where multifamily cap rates plateaued at 5.7% for seven consecutive quarters—the longest flat streak in 25 years. According to an analysis from First American, this stagnation was caused by investor uncertainty over interest rate volatility, which suppressed transaction volume even as market fundamentals like rent growth improved. You can read the full analysis on cap rate trends from First American for more detail.

The Narrowing Spread

A critical indicator is the spread between multifamily cap rates and the 10-year Treasury yield. This gap represents the risk premium—the extra return investors demand for choosing a real estate asset over a "risk-free" government bond. As the Fed's aggressive rate-hiking cycle appears to be concluding, this spread has begun to narrow, signaling a potential return to normalcy. If Treasury yields stabilize or decline, it creates room for cap rates to compress without investors feeling undercompensated for risk.

The extreme caution that defined the last two years is slowly yielding to a more fundamentals-driven market. As temporary headwinds fade, factors like NOI growth can once again become the primary driver of value.

Potential Scenarios for 2025 and Beyond

Two primary scenarios are likely, both tied directly to monetary policy.

| Scenario | Conditions | Cap Rate Impact |

|---|---|---|

| Modest Compression | Federal Reserve begins cutting rates; credit markets loosen. | Increased liquidity and cheaper borrowing costs will boost transaction volume, leading to higher valuations and lower cap rates. |

| Continued Stability | Inflation remains persistent; interest rates stay "higher for longer." | The bid-ask spread between buyers and sellers will remain wide, keeping transaction volume low and cap rates flat. |

Regardless of the scenario, the era of relying on aggressive cap rate compression for returns is over. The focus for successful investors has shifted to operational excellence: driving value through superior management, strategic capital improvements, and maximizing NOI.

What are the most frequently asked questions about multifamily cap rates?

Here are direct answers to the most common questions investors have about multifamily cap rates.

What is a good multifamily cap rate?

There is no single "good" multifamily cap rate; the appropriate rate is entirely relative to investment strategy, risk tolerance, and the specific market. However, general ranges exist.

| Asset Class / Market | Typical Cap Rate Range | Rationale |

|---|---|---|

| Class A (Primary Markets) | 4.0% – 5.5% | Investors pay a premium for new, stable assets in top-tier cities, accepting a lower initial return for lower risk and appreciation potential. |

| Class B (Secondary Markets) | 5.5% – 7.0% | This segment offers a balance of initial cash flow and value-add potential, attracting a large pool of investors. |

| Class C (Tertiary Markets) | 7.0% and up | The higher return reflects greater perceived risk, such as older buildings requiring more intensive, hands-on management. |

A "good" cap rate is one that adequately compensates an investor for the risk they are taking on.

How does leverage affect cap rate analysis?

Leverage (debt) has zero direct effect on a property's cap rate. The cap rate is an unlevered metric, calculated using Net Operating Income (NOI), which by definition excludes mortgage payments.

This is a critical feature, as it allows for the direct comparison of properties based on their intrinsic operational performance, irrespective of how they are financed. The performance of a deal with financing is measured by other metrics, most importantly the Cash-on-Cash Return, which compares the annual cash flow after debt service to the actual cash invested.

Can a cap rate be negative?

Yes, a cap rate can be negative, but it is extremely rare and signals a severely distressed asset. A negative cap rate occurs when a property's operating expenses exceed its total income, resulting in a negative Net Operating Income (NOI).

An investor purchasing a property with a negative cap rate is not acquiring a cash-flowing asset. They are buying a significant turnaround project that will require a large capital infusion and a complete operational overhaul just to reach break-even.

Ready to stop guessing and start making data-driven decisions? With BatchData, you can access the property-level details, valuation models, and market comps you need to analyze multifamily deals with confidence. Get the accurate data you need to master your market.