Interest rates directly impact property values by influencing borrowing costs, affordability, and investment returns. Here’s what you need to know:

- Higher interest rates make mortgages more expensive, reducing buyer demand and property values. Sellers may also hesitate to list homes due to "lock-in effects", where their current low-rate mortgage is more appealing than a new higher-rate loan.

- Lower interest rates increase affordability, enabling buyers to purchase more expensive properties and driving up demand. This often results in higher property values.

- For investors, interest rates affect capitalization rates (cap rates), which are used to value income-generating properties. Higher rates lead to higher cap rates and lower property values, while lower rates have the opposite effect.

- Historical trends show that rising rates often slow market activity, while falling rates boost it.

Understanding these dynamics is critical for navigating real estate markets, especially as interest rates fluctuate. Utilizing a real estate data provider can help you track these changes effectively.

How Interest Rates Impact Property Values and Monthly Mortgage Payments

What Are Interest Rates and How Do They Affect Real Estate?

Understanding Interest Rates

Interest rates are essentially the cost of borrowing money, shown as a percentage of the loan’s principal amount. In the U.S., the Federal Reserve plays a key role in setting these rates as part of its efforts to maintain stable prices and support employment. When the Fed adjusts its benchmark rate, the effects ripple through the economy, influencing everything from credit card rates to the interest on a $400,000 mortgage.

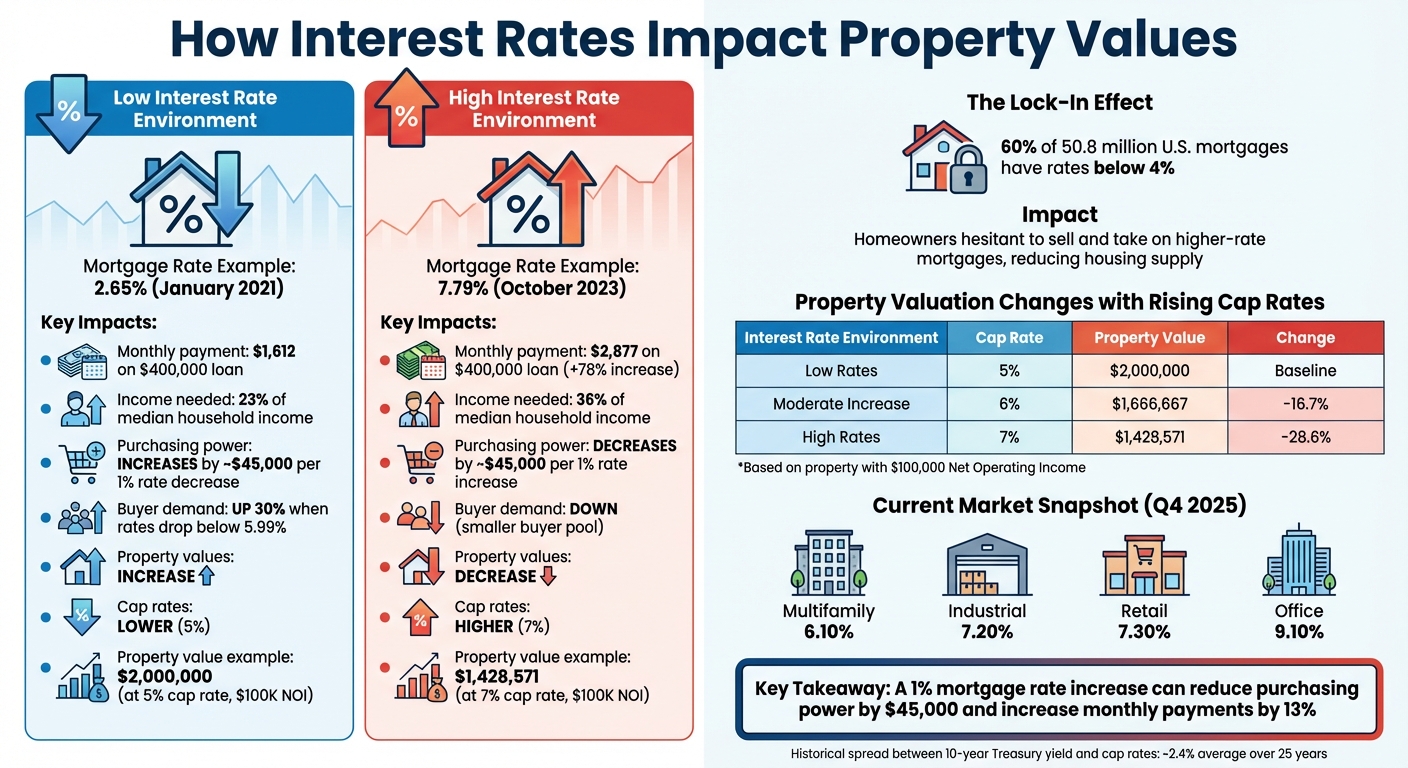

In real estate, this is especially important because mortgage affordability is directly tied to interest rates. Even a 1% increase can push monthly mortgage payments up by about 13%. For instance, on a $400,000 loan, a rate increase from 4% to 5% reduces purchasing power by around $45,000. That could mean the difference between buying your dream home or settling for something smaller or less ideal.

Interest rates also affect how much capital flows through the real estate market. Low rates encourage lenders to extend more credit, often with higher loan-to-value (LTV) ratios that require smaller down payments. But when rates rise, lenders tighten their requirements, asking for larger down payments and offering less favorable terms. These changes in borrowing costs create waves that influence both buyer activity and housing supply. Professionals often use property search tools to track these inventory shifts in real-time.

How Interest Rates Influence Supply and Demand

Higher interest rates tend to cool buyer demand by making homeownership more expensive. Between January 2021 and October 2023, mortgage rates jumped from 2.65% to 7.79%. For someone financing $400,000, this increase caused monthly payments for principal and interest to rise by 78% – from $1,612 to $2,877. By late 2024, households needed to allocate about 36% of their monthly income to afford a median-priced home, compared to just 23% in early 2021.

This affordability crunch also impacts sellers, creating a "lock-in effect." Nearly 60% of the 50.8 million active mortgages in the U.S. have interest rates below 4%. Homeowners with these low rates are hesitant to sell and take on a new mortgage at 6% or 7%. This reluctance reduces the number of homes available for sale, which can keep prices high despite weaker demand.

Conversely, lower interest rates tend to boost both demand and supply. Buyers can afford larger loans, developers find it cheaper to fund new construction projects, and investors gain easier access to capital for property acquisitions. This heightened activity often drives property values up as competition intensifies. These shifts in borrowing costs, combined with changing market dynamics, also influence capitalization rates and overall property valuations.

sbb-itb-8058745

Interest Rates And Home Value Appreciation | Amol Heda

Understanding these shifts is essential for real estate investing success in changing markets.

How Do Interest Rate Changes Affect Property Values?

Interest rate fluctuations have a clear and direct impact on property values, influencing both what buyers can afford and how investors evaluate returns. When rates drop, property values tend to rise. Conversely, when rates climb, values often stagnate or fall. Grasping these dynamics is crucial for real estate professionals aiming to predict market trends and guide clients effectively. Let’s break down how these changes affect the market.

When Interest Rates Decrease

Falling interest rates make borrowing cheaper, which boosts affordability and increases buyers’ purchasing power. For example, a 1% rate decrease on a $400,000 loan could allow buyers to afford about $45,000 more in property value. This expanded affordability often fuels competition, driving up demand and, subsequently, property prices.

Take January 2021, when mortgage rates hit a record low of 2.65%. At that time, buyers spent only about 23% of the median household income on mortgage payments for principal and interest. Additionally, homeowners who refinanced between January and October 2020 collectively saved an estimated $5.3 billion annually. Bill Banfield, Chief Business Officer at Rocket Mortgage, highlighted the psychological effect of lower rates:

"When rates fall below 5.99%, Rocket typically sees demand rise by about 30%… this is clear evidence that rates starting with a five flip a psychological switch".

Lower rates also encourage investors to shift their capital from bonds to real estate, seeking better returns. This inflow of investment capital further drives up property values. Developers, too, benefit from reduced financing costs, enabling more construction activity.

When Interest Rates Increase

On the flip side, rising interest rates reduce affordability and dampen market activity. Between January 2021 and October 2023, mortgage rates surged from 2.65% to 7.79%, causing monthly payments to skyrocket. By late 2024, households needed to allocate roughly 36% of their monthly income to afford a median-priced home, up from just 23% in early 2021.

Luke Babich, CEO and Co-founder of Clever Real Estate, explained the impact of higher rates:

"Rising interest rates result in a decreased demand for homes and sellers may be facing a smaller pool of potential buyers".

This reduced demand often leads to longer listing times and price reductions as sellers try to attract buyers. Compounding the issue is the "lock-in effect", where nearly 60% of active mortgages in the U.S. have rates below 4%. This discourages homeowners from selling and entering a higher-rate market.

For investors, higher rates push up capitalization rates (cap rates). As financing costs rise, investors demand greater returns. For example, a property generating $100,000 in net operating income valued at $2 million with a 5% cap rate would see its value drop to approximately $1.67 million if the cap rate increases to 6%. These shifts force investors to reassess property income and valuation models. Michael Fratantoni, Chief Economist at the Mortgage Bankers Association, shared his perspective:

"MBA’s forecast has been for mortgage rates to remain in a relatively narrow trading range for the foreseeable future, likely remaining between 6% and 6.5% for 30-year conforming loans".

Next, we’ll dive deeper into how these interest rate changes influence cap rates and overall property valuations.

Interest Rates, Cap Rates, and Property Valuation

Interest rates and cap rates work hand in hand to influence property valuation. Cap rates act as a link between borrowing costs and property prices, guiding investor decision-making.

Earlier, we discussed how rising interest rates can lower property values. Now, let’s dive into the cap rate mechanism that drives this effect.

What Are Cap Rates?

The capitalization rate, or cap rate, is a simple ratio: a property’s net operating income (NOI) divided by its market value or purchase price. Here’s the formula: Cap Rate = NOI ÷ Property Value.

For example, if a property generates $100,000 in annual NOI and is sold for $2,000,000, the cap rate is 5%.

Cap rates help investors understand how long it might take to recover their initial investment purely through income. A property with a 10% cap rate would take about 10 years to break even. Lower cap rates generally suggest lower risk and more stable income, while higher cap rates indicate higher risk and the need for greater returns. As Investopedia puts it:

"The capitalization rate indicates the property’s intrinsic, natural, and unlevered rate of return".

How Interest Rates Affect Cap Rates

Typically, interest rates and cap rates tend to move in the same direction. When the Federal Reserve raises interest rates, the 10-year U.S. Treasury yield – often used as the "risk-free rate" – also rises. Since cap rates are essentially the risk-free rate plus a risk premium, they must increase too, ensuring investors continue to receive an acceptable return. Historically, this spread has averaged around 2.4% over the past 25 years.

Higher interest rates make borrowing more expensive, which reduces the pool of available investment capital. Trey Webb, a partner at Bennett Thrasher, explains:

"As interest rates increase, investors typically demand higher returns to compensate for the increased cost of capital and the availability of alternative investments with better yields".

This creates an inverse relationship between cap rates and property values. For example, if a property’s NOI remains steady but the cap rate rises from 5% to 6%, its value drops from $2,000,000 to roughly $1,666,667 – a loss of $333,333. And that’s without any change in the property’s income performance.

However, private market cap rates often lag behind interest rate changes because they rely on periodic appraisals and sales data. For instance, in early 2023, real estate investment trust (REIT) implied cap rates increased by 1.6%, while private market cap rates rose by just 0.2%.

Example: Cap Rates in Different Interest Rate Environments

Let’s see how a property generating $100,000 in NOI changes in value as cap rates shift due to varying interest rate conditions:

| Interest Rate Environment | Cap Rate | Property Value | Change from Baseline |

|---|---|---|---|

| Low Rates (Baseline) | 5% | $2,000,000 | – |

| Moderate Rate Increase | 6% | $1,666,667 | -$333,333 (-16.7%) |

| High Rate Environment | 7% | $1,428,571 | -$571,429 (-28.6%) |

As of Q4 2025, national average cap rates varied widely by property type: multifamily properties averaged 6.10%, industrial properties 7.20%, office properties 9.10%, and retail properties 7.30%. Between Q4 2024 and Q4 2025, office cap rates rose by 0.2%, while multifamily cap rates remained steady. These differences highlight variations in risk, tenant stability, and income predictability across real estate sectors.

Real estate professionals should keep an eye on the spread between the 10-year Treasury yield and local cap rates. This spread can indicate whether the current risk premium adequately accounts for market volatility. In a rising rate environment, focusing on boosting NOI – whether through rent growth or cutting expenses – can help counteract the pressure of increasing cap rates on property values.

U.S. Interest Rate Trends and Property Valuation Over Time

Looking back at U.S. interest rate trends reveals how they’ve shaped property values over the years. Two periods stand out: the early 1980s, when rates skyrocketed past 16%, and the post-2008 era, which saw rates drop to historic lows.

High Interest Rates and Market Slowdowns

The early 1980s illustrate the dramatic effects of soaring interest rates. With mortgage rates climbing above 16% as the Federal Reserve tackled 1970s inflation, the housing market slowed significantly. While nominal home prices still rose, real prices – adjusted for inflation – declined in many areas. As Bryan Prewitt from The Prewitt Team explains:

"When adjusted for inflation, real house prices actually declined in many areas of the U.S. during the early 1980s. This means that, in terms of purchasing power, homes became cheaper".

This high-rate environment led to a sharp drop in home sales, stalled construction projects, and a shift toward rentals, which created an oversupply. Prices fell further, and some homeowners faced negative equity. Regional disparities emerged, with places like New England and California experiencing pronounced boom-bust cycles. From September 1979 to March 1982, home price appreciation slowed from 12.9% to just 1.1%.

Fast forward a few decades, and the market dynamics shifted dramatically.

Low Interest Rates and Market Expansion

Following the 2008 financial crisis, mortgage rates plummeted, making homes more affordable despite rising prices. Rates hit a record low of 2.65% in January 2021. This drop reduced monthly payments, allowing buyers to stretch their budgets. For instance, principal and interest payments accounted for about 23% of median household income in January 2021, down from 26% in 2019.

These low rates fueled a property value surge. Homeowners who refinanced between January and October 2020 collectively saved an estimated $5.3 billion annually. By late 2024, nearly 60% of the 50.8 million active U.S. mortgages carried interest rates below 4%, discouraging homeowners from selling when rates began to climb again.

The affordability shift is striking: in January 2021, monthly payments on a median-priced home were $1,359, but by October 2023, they had jumped to $2,891.

What This Means for Real Estate Professionals Today

These historical patterns provide valuable insights for today’s market. Data shows that for every 1-percentage-point rise in 30-year fixed mortgage rates, house prices typically drop by -1.6% within a year and by 4.4% over a decade. Alexander Chudik and Anil Kumar from the Federal Reserve Bank of Dallas highlight:

"Regions more sensitive to mortgage rate changes will experience larger declines in house prices and home equity, reducing their borrowing capacity in the face of an economic slowdown".

As of January 29, 2026, the 30-year fixed-rate mortgage average stands at 6.10%. While this is far below the peaks of the 1980s, today’s market is more sensitive to rate shifts. Factors like stricter land-use regulations, which limit housing supply, and the growing share of investor-owned properties amplify this sensitivity.

Tools like BatchData‘s advanced real estate data solutions help professionals navigate these challenges. By tracking regional rate sensitivities, monitoring inventory, and identifying areas with tight supply, real estate experts can better predict where prices might hold steady or fluctuate. Manufacturing-heavy regions and areas with high investor activity often show greater price swings during rate changes, offering opportunities for strategic investments.

Conclusion

Interest rates play a key role in shaping property values by influencing borrowing costs, buyer affordability, and investor return expectations. When rates climb, financing becomes pricier, reducing purchasing power and prompting investors to seek higher returns – both of which can drive property values down. On the flip side, lower rates make borrowing cheaper, improve affordability, and compress cap rates, often pushing prices upward. As discussed earlier, higher rates not only increase borrowing costs but also decrease purchasing power, amplifying their effect on property values.

Cap rates, which connect market returns to borrowing costs, are crucial for understanding property value trends. These rates, factoring in the risk-free rate and a market risk premium, tend to shift alongside interest rates, directly impacting valuations. For instance, in Q4 2025, cap rates averaged 6.10% for multifamily properties and 9.10% for office properties. By tracking the spread between cap rates and Treasury yields, investors can assess whether real estate risks are being adequately rewarded. Together, these factors highlight the importance of precise market analysis.

BatchData’s real estate tools equip professionals with the insights needed to navigate these market dynamics and uncover strategic investment opportunities. With access to detailed property data, users can evaluate regional sensitivities to interest rates, spot value-add properties trading 12–20% below national averages, and analyze ownership trends that may indicate supply constraints. Whether you’re studying the "lock-in effect" among homeowners with sub-4% mortgages or planning for future investments by assessing exit cap rates, having accurate data can turn interest rate volatility into a strategic advantage.

FAQs

How do changes in interest rates affect my ability to buy a home?

Interest rate fluctuations can significantly affect how much house you can afford. When rates rise, your monthly mortgage payments increase, which can shrink your budget and limit the homes you can consider. On the flip side, when rates fall, borrowing becomes less expensive. This might mean you qualify for a larger loan or save money on your monthly payments.

Even slight changes in interest rates can make a big difference over the life of your loan. That’s why keeping an eye on rate trends is crucial. Combining this awareness with accurate real estate data can help you decide when to buy and find the right property that fits your budget.

How do interest rates impact cap rates in real estate?

Interest rates and cap rates share a close link in real estate valuation. For example, when interest rates – like the 10-year Treasury yield – go up or down, cap rates tend to shift accordingly. Generally, a 100-basis-point change in interest rates can lead to cap rate adjustments of anywhere from 41 to 78 basis points, depending on the property type.

This connection matters because cap rates are a key tool for investors to assess property value and potential returns. When interest rates climb, borrowing becomes more expensive, which often drives cap rates higher and can lead to lower property values. On the flip side, when interest rates drop, borrowing costs decrease, cap rates tend to fall, and property values may rise.

How do changes in interest rates affect property values, and how can I predict future trends?

Interest rate fluctuations play a key role in shaping property values by directly affecting housing affordability and demand. When interest rates climb, borrowing costs increase, which often dampens homebuyer demand and slows the pace of property value growth. On the flip side, lower interest rates make borrowing more affordable, leading to increased demand and pushing property values higher.

Understanding these dynamics requires a close look at historical data and market behavior. Examining past interest rate shifts can shed light on how property values responded in specific areas, revealing useful patterns. Advanced tools like geospatial mapping and automated valuation models (AVMs) further enhance this analysis by incorporating factors such as interest rates, rental trends, and other key market indicators. These insights empower investors, lenders, and policymakers to make well-informed decisions in the ever-changing property market.