Compliance in real estate is more critical than ever, especially with the new FinCEN Residential Real Estate (RRE) Rule, effective March 1, 2026, which ends anonymity in all-cash property transactions. Ignoring compliance can lead to severe financial penalties, legal consequences, and operational disruptions. Here’s a quick summary of the top risks:

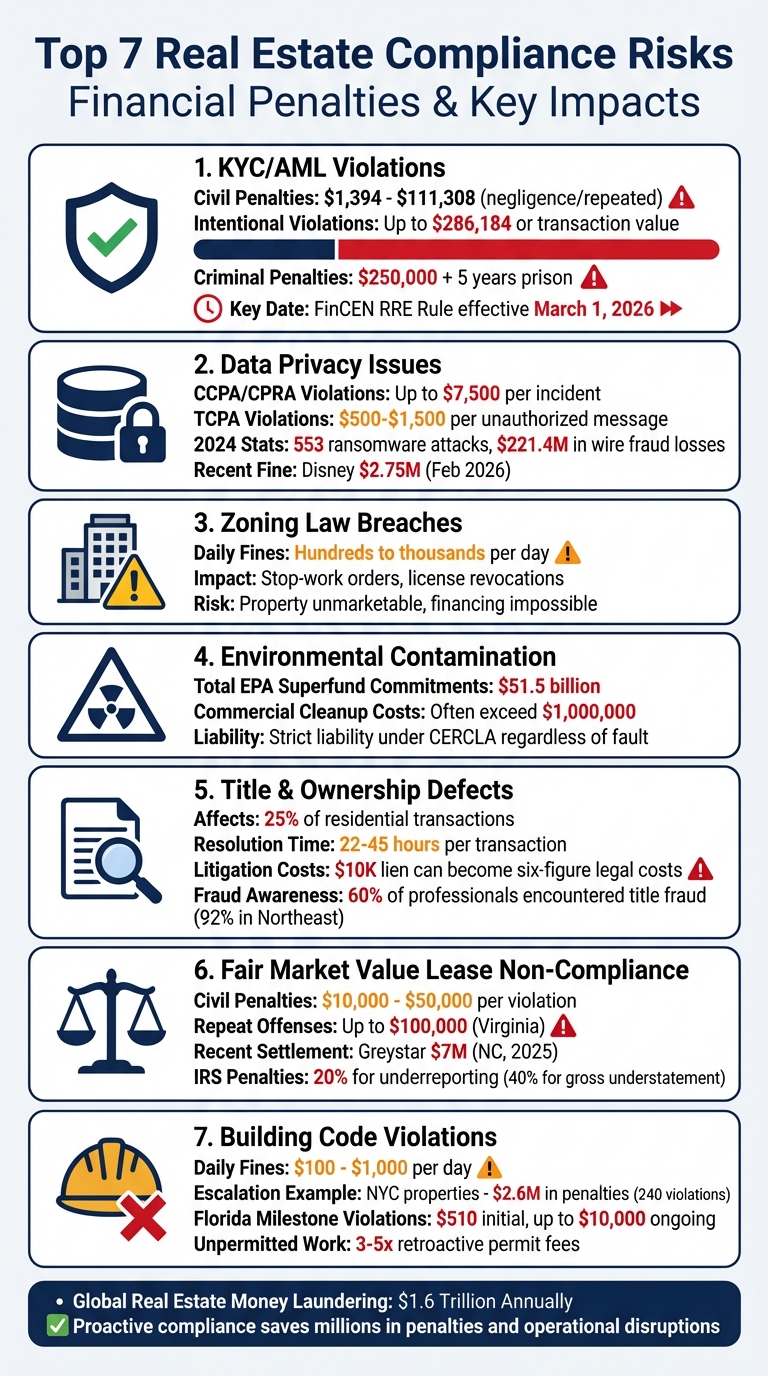

- KYC/AML Violations: New reporting requirements for beneficial ownership in real estate transactions. Penalties can exceed $250,000 or lead to prison time.

- Data Privacy Issues: Strict state laws like CCPA and federal requirements demand secure handling of sensitive information. Fines can reach $7,500 per violation.

- Zoning Law Breaches: Misuse of land or outdated zoning compliance can halt operations and lead to daily fines or lawsuits.

- Contamination Liabilities: CERCLA holds property owners accountable for costly cleanups, even if contamination occurred decades earlier.

- Title Defects: Issues like liens or fraud can stall transactions and cost thousands in legal fees.

- Fair Market Value Lease Non-Compliance: Violations of fair housing laws or improper rent-setting practices can result in fines up to $100,000.

- Building Code Violations: Unpermitted work or safety hazards can lead to stop-work orders, fines, or revoked occupancy certificates.

Failing to address these risks can lead to operational shutdowns, reputational damage, and hefty fines. Proactive measures like risk assessment due diligence, regular audits, and leveraging compliance tools can save businesses from these pitfalls.

7 Critical Real Estate Compliance Risks: Penalties and Financial Impact

1. KYC/AML Violations

Regulatory Impact

KYC/AML compliance has become a critical concern in real estate, especially with the introduction of FinCEN’s RRE Rule, set to take effect on March 1, 2026. This rule eliminates real estate transaction anonymity, replacing the older GTOs that were limited to specific cities. Now, any non-financed residential property transfer to a legal entity or trust must be reported.

The rule outlines a clear reporting hierarchy, assigning responsibility to professionals like closing or settlement agents, document recorders, title underwriters, and others involved in the transaction process. These individuals must collect and verify Beneficial Ownership Information (BOI) for anyone owning at least 25% of the entity or exercising significant control. Reports are due within 30 calendar days of closing or by the last day of the following month – whichever is later.

This regulatory shift highlights the growing scrutiny in real estate transactions.

Financial Penalties

Failing to comply with KYC/AML rules comes with heavy financial consequences, varying based on the nature of the violation. Civil penalties for negligence range from approximately $1,394 to $111,308 for repeated oversights. Intentional violations are far costlier, with fines reaching up to $286,184 or the transaction value, whichever is higher. Criminal penalties for willful violations include fines of $250,000 and up to five years in prison.

A recent example comes from the UK, where the Financial Conduct Authority (FCA) prosecuted WealthTek in December 2024 for laundering £806,500 and £3.9 million through real estate transactions. The case revealed poor validation of funds and inadequate checks on ownership structures.

These penalties, combined with operational challenges, underscore the importance of compliance.

Operational Disruptions

Non-compliance doesn’t just lead to fines – it can also disrupt business operations. Risks include license suspensions, stop-work orders, and significant reputational harm. Professionals are now required to gather detailed information, such as Tax Identification Numbers (TINs), addresses, citizenship status, and payment methods for all parties involved in a transaction. Additionally, firms must retain designation agreements and BOI records for five years.

"AML real estate compliance is no longer optional. The combination of high-value deals, opaque ownership structures, and cross-border activity has made the sector a key focus for regulators." – AiPrise

Mitigation Strategies

To navigate these risks, businesses need targeted strategies. One effective approach is using designation agreements to assign a single reporting party for each transaction. Updating engagement letters and internal procedures to include BOI collection as a standard practice is another critical step. A risk-based approach – adjusting due diligence based on factors like geography, transaction value, and ownership complexity – can also help minimize exposure. Watch for red flags like rushed closings without proper documentation, transactions far from market norms, or the involvement of multiple intermediaries.

For added efficiency, third-party filing services are available, charging around $189 per report. Advanced data tools, such as those offered by BatchData (https://batchdata.io), can further streamline the process of compiling and verifying compliance information.

sbb-itb-8058745

2. Data Privacy Issues

Regulatory Impact

Real estate firms face a growing maze of state privacy laws designed to regulate how personal data is collected, stored, and shared. Key regulations like the California Consumer Privacy Act (CCPA/CPRA), Virginia Consumer Data Protection Act (VCDPA), Colorado Privacy Act (CPA), and Texas Data Privacy and Security Act (TDPSA) each impose their own sets of requirements. By January 1, 2026, new privacy rules came into effect in Indiana, Kentucky, and Rhode Island, while Montana and Connecticut expanded their existing frameworks. California, in particular, has been aggressive in enforcement. In February 2026, the state’s Attorney General’s Office imposed a record $2.75 million fine on The Walt Disney Company for violating the CCPA, signaling how seriously these laws are being enforced.

Real estate companies are especially vulnerable due to the sensitive information they handle, often referred to as "data honeypots." These include Social Security numbers, credit scores, bank statements, and precise location data. Federal laws like the Gramm-Leach-Bliley Act (GLBA) require encryption of financial data during storage and transmission, especially in transactions involving mortgage applications or financial proofs. Meanwhile, the Telephone Consumer Protection Act (TCPA) regulates automated marketing communications, requiring explicit written consent before sending AI-driven texts or calls. The Federal Trade Commission (FTC) also mandates clear disclosure when AI tools interact with customers.

Financial Penalties

Failing to comply with privacy laws can lead to hefty fines. Violations of the CCPA/CPRA and TCPA can result in penalties of up to $7,500 per incident and $500–$1,500 per unauthorized message, respectively. For example, in May 2022, Weichert Realtors paid $1.2 million to settle charges related to three separate data breaches that exposed the information of nearly 11,000 consumers. Investigators found lapses like missing antivirus software and the absence of multi-factor authentication. Similarly, in September 2024, the FTC fined Invitation Homes $48 million for hidden fees and failing to disclose how tenant data was handled between 2021 and 2023.

California’s CPRA also allows residents to file lawsuits if their unencrypted personal data is compromised due to poor security practices. This opens companies up to not just regulatory fines but also the risk of class-action lawsuits.

Operational Disruptions

Privacy violations can wreak havoc on operations, eroding trust and forcing businesses into crisis mode. In 2024 alone, the real estate sector faced 553 ransomware attacks, while wire fraud in property transactions caused $221.4 million in losses. Many state laws require companies to notify affected parties of breaches within 30–60 days, adding pressure to already strained resources.

In December 2025, the Digital Advertising Accountability Program (DAAP) flagged Zillow, Trulia, and HotPads for broken privacy links, missing disclosures on interest-based advertising, and unauthorized collection of location data. Alarmingly, 30–40% of small and medium-sized real estate websites still lack privacy policies, leaving them vulnerable to legal actions and reputational damage.

"The era of ‘fix it later if we have to’ is largely over." – Josh Hansen, Attorney, Shook, Hardy & Bacon

Mitigation Strategies

Protecting data privacy requires proactive measures. AI-powered redaction tools can help strip sensitive details like Social Security numbers and bank account information from tenant applications before sharing them with third parties. Implement role-based access controls to limit data exposure by creating "Service Users" with restricted permissions for AI or third-party tools, instead of granting full CRM access. To comply with the TCPA, update lead capture forms to include timestamped consent checkboxes, and maintain an organized data inventory to streamline responses to data access requests.

Vendor contracts should include clear data protection clauses, such as audit rights and restrictions on subcontracting. Replace email-based document exchanges with secure upload portals to reduce the risk of unauthorized data interception. Additionally, the CCPA requires businesses to update their privacy policies annually, making yearly reviews a smart practice.

"Strong compliance isn’t just protection – it’s a trust advantage in a privacy-conscious U.S. real estate market." – Mark C., TheShift.ai

For companies managing large volumes of property and client data, advanced solutions like BatchData offer automated property enrichment and verification tools, helping streamline compliance efforts. Learn more at BatchData.io.

3. Zoning Law Breaches

Regulatory Impact

Zoning violations happen when property owners use land in ways that don’t align with local zoning rules. Typical examples include running a business in a residential area, building structures that exceed height limits, or ignoring setback requirements. When these breaches occur, local zoning boards often step in with enforcement actions like cease-and-desist orders or stop-work notices, which can bring construction or business operations to a grinding halt.

Things get trickier when it comes to "grandfathered" properties – those that were legally compliant under older zoning laws but no longer meet updated regulations. If owners make significant changes or expansions to these properties, they can unintentionally violate current zoning rules. For example, vague violation notices for grandfathered properties have sparked legal battles in local courts, highlighting the importance of clear enforcement. These uncertainties can lead to major financial risks for property owners.

Financial Penalties

Zoning violations don’t just cause headaches – they can hit your wallet hard. Civil penalties often pile up daily until the issue is resolved, with fines ranging from hundreds to thousands of dollars per day. Beyond fines, unresolved zoning problems can make properties nearly impossible to finance. Most lenders demand proof of compliance before approving loans.

"Unless the real estate developer is paying cash, it won’t be financeable because most lenders require confirmation and proof that the zoning match is the intended use." – Harlan W. Robins, Commercial Real Estate Attorney, Frost Brown Todd LLP

These violations don’t just affect finances; they can also drag down property values and invite lawsuits. Government agencies or neighbors might sue, claiming "special damage" caused by the breach.

Operational Disruptions

The fallout from zoning violations isn’t limited to financial penalties. Owners may face orders to modify or even demolish noncompliant structures. In some cases, municipalities can revoke essential operational licenses, such as fire safety permits, and even block violators from obtaining future permits. These disruptions can complicate property sales too, as potential buyers are often unwilling to take on unresolved legal issues.

Mitigation Strategies

To avoid the financial and operational challenges of zoning violations, preparation is key. Start by conducting thorough due diligence before buying property. Check the local zoning map to confirm the property’s designation, permits, and any restrictions like setbacks or height limits. Consulting land-use experts can also help ensure compliance with local laws.

If your project doesn’t meet zoning codes, consider applying for a variance. An area variance addresses physical changes, while a use variance covers activity-related adjustments. Always secure the necessary permits from the local planning department before beginning construction, and keep track of permit renewal deadlines to stay compliant.

If you receive a violation notice, act quickly. Contact local authorities to understand the steps needed to fix the problem and prevent escalating penalties. Proactive management can save time, money, and a lot of stress in the long run.

4. Environmental Contamination Liabilities

Regulatory Impact

Environmental risks in real estate transactions require the same level of scrutiny as KYC/AML and data privacy concerns. Among these, contamination liabilities stand out as some of the most pressing. Under the Comprehensive Environmental Response, Compensation, and Liability Act (CERCLA), property owners can be held strictly and jointly responsible for the costs of cleaning up contamination – regardless of whether they caused it or when it occurred. This means that even if a property was purchased just 18 months ago, the Environmental Protection Agency (EPA) can demand the current owner pay the entire remediation bill.

"Environmental contamination discovered post-closing can make the buyer a potentially responsible party under the Comprehensive Environmental Response, Compensation, and Liability Act (CERCLA), regardless of who caused the pollution." – Rimkus

To reduce this risk, buyers must conduct "All Appropriate Inquiries" (AAI) before closing. A Phase I Environmental Site Assessment (ESA), following ASTM E1527-21 standards, helps identify recognized environmental conditions (RECs) through document reviews, on-site inspections, and interviews. If RECs are found, a Phase II ESA must follow. This involves invasive testing – such as soil, groundwater, and air sampling – based on ASTM E1903-19 standards to confirm contamination levels. Skipping these steps can lead to severe financial and legal consequences.

Financial Penalties

The financial fallout from environmental liabilities can be staggering. The EPA has reported a total of $51.5 billion in Superfund remediation commitments. For commercial properties, cleanup costs frequently surpass $1,000,000, and a single remediation order can rack up six-figure expenses. Worse yet, these liabilities don’t disappear – they stay tied to the property unless specific legal defenses are successfully argued.

Contaminated properties often face diminished market value and reduced appeal to future buyers, further compounding the financial strain. Without proper due diligence, property owners risk losing the "innocent landowner defense", leaving them vulnerable to enforcement actions at both federal and state levels.

Operational Disruptions

The discovery of contamination doesn’t just hurt financially – it can bring operations to a standstill. Stop-work orders may be issued, halting construction or ongoing activities indefinitely. Daily penalties can pile up until the cleanup is complete. In some cases, properties may even be deemed uninhabitable during remediation, wiping out rental income or operational use entirely. Even after cleanup, restrictions like industrial-only use may remain in place to maintain liability protections, limiting the property’s future utility.

Mitigation Strategies

To protect against these risks, start a Phase I ESA as soon as the contract is signed. Ensure the assessment complies with EPA’s AAI standards, keeping in mind that it’s only valid for one year and requires updates if any part of the report is older than 180 days. It’s also essential to hire an environmental professional who meets the EPA’s qualifications for education and experience.

Contracts should include protective measures such as indemnification clauses, environmental escrow accounts, or adjustments to the purchase price to share the risk of contamination between buyer and seller [33, 37]. Environmental Impairment Liability (EIL) insurance can also provide coverage for unexpected contamination or legal claims after closing. For properties classified as brownfields, state programs may offer liability protections and tax incentives in exchange for specific remediation efforts. Like other regulatory compliance measures, thorough environmental due diligence is crucial to safeguarding real estate investments.

5. Title and Ownership Defects

Regulatory Impact

Title and ownership defects are a major compliance challenge in real estate, impacting 25% of residential transactions. These issues can include unpaid property taxes, unresolved liens, clerical mistakes, fraud, and disputes over ownership. By 2025, 60% of real estate professionals acknowledged encountering title fraud or deed theft, with that number soaring to 92% in the Northeast U.S.. Federal law complicates matters further, as unpaid tax debts can attach to a property through liens, even after ownership changes – leaving unsuspecting buyers financially liable.

"A title defect is any issue that puts the legal ownership of a property into question." – Gomez Law, APC

Fixing these problems isn’t easy. Title companies typically spend 22 to 45 hours resolving defects for a single transaction. In fact, 36% of real estate transactions are categorized as "difficult", requiring extra effort to address issues before closing. Common problems include contractor liens, mortgages that appear unpaid despite being settled, boundary disputes uncovered during new surveys, and inheritance claims with missing or undocumented heirs. These complications create financial and operational risks that can derail transactions entirely.

Financial Penalties

The financial fallout from title defects can be steep. For example, a $10,000 lien can balloon into six-figure litigation costs if a "Quiet Title" action is needed to settle ownership disputes. California law allows judgment liens to remain attached to properties for 10 years, with the option to renew for another decade. Similarly, federal tax liens under 26 U.S.C. § 6323 can transfer to new owners, leaving them responsible for debts they didn’t incur.

Title problems can also make properties unmarketable, reducing their value and scaring off buyers or investors. Unresolved encumbrances can interfere with refinancing, lower an asset’s lending value, or force property owners into higher interest rates – adding to the financial burden. These penalties don’t just impact finances; they can also grind transactions to a halt.

Operational Disruptions

Title defects don’t just cost money – they disrupt the entire real estate process. Lenders often refuse to finance or refinance properties without clear title, delaying deals and revenue cycles. For developers, a single title issue can ripple across multiple projects, freezing negotiations and stalling progress.

"Title issues do more than delay closings – they disrupt entire operational ecosystems." – Legal Support World

Properties with unresolved title problems are also harder to insure, and investors may walk away rather than risk inheriting liabilities. Even after a purchase, undisclosed easements – like shared driveways or utility access rights – can restrict how a property is used and hurt its long-term value.

Mitigation Strategies

Addressing title defects early is key to minimizing risk. Start by ordering a comprehensive title search as soon as the purchase agreement is signed. This allows 10 to 14 days for a "curing period" to resolve issues without delaying closing. Protect yourself further by securing both lender’s and owner’s title insurance, which can cover hidden problems like forged documents, unknown heirs, or clerical errors that surface later.

After paying off a mortgage, confirm within 90 days that a "satisfaction of mortgage" or "reconveyance" has been officially recorded in county records – unreleased mortgages are a frequent issue that complicates future sales. Conduct a professional survey early to identify any boundary disputes or encroachments that don’t match the legal description. With lenders tightening their scrutiny in 2026 and deed fraud on the rise, thorough title checks are no longer optional – they’re essential to safeguarding real estate investments.

6. Fair Market Value Lease Non-Compliance

Regulatory Impact

Lease compliance has become a growing area of scrutiny, much like KYC/AML and data privacy. Regulators are now closely examining practices like algorithmic rent-setting and income requirements that may discriminate against certain groups. For instance, the Department of Justice and state attorneys general are investigating automated pricing tools that rely on non-public competitor data, which could potentially violate antitrust laws. In late 2025, the North Carolina Attorney General reached a $7 million settlement with Greystar Management LLC, requiring the company to stop using non-public data from other landlords in its AI pricing algorithms.

Fair housing enforcement has also ramped up, particularly around "source of income" protections. This includes penalties for landlords who impose income requirements – like asking tenants to earn two or three times the monthly rent – without accounting for housing vouchers. In late 2025, a Washington D.C. landlord faced $10,000 in penalties for violating the Human Rights Act by advertising an income requirement of twice the rent. Similarly, Douglas Elliman settled for $35,000 in civil penalties and established a $15,000 fund to assist prospective voucher applicants.

Financial Penalties

Violating fair housing laws can result in steep financial consequences. Civil penalties alone can range from $10,000 to $50,000, with repeat offenses in states like Virginia potentially leading to fines as high as $100,000. One notable case, the Parkchester Preservation Management settlement, resulted in a $1,050,000 payout for source of income non-compliance in New York.

Legal defense costs can also be substantial, often exceeding $500,000 in class-action lawsuits. Additionally, properties backed by Fannie Mae or Freddie Mac face federal mandates like providing 30-day written notices for rent increases and 5-day grace periods for late fees. Tax compliance issues add another layer of risk, as the IRS imposes a 20% penalty for underreporting fair rental value, which escalates to 40% for gross understatements.

Mitigation Strategies

To avoid fair market value lease violations, proactive measures are essential. Regular audits of automated pricing tools and screening systems can help ensure they don’t use non-public competitor data or introduce statistical bias against protected classes. Centralizing key administrative tasks across multi-state portfolios can also reduce inconsistent practices that might lead to violations.

When determining fair market value, use a CMA (comparative market analysis) based on rentals of three to five similar properties. For high-value or commercial properties, hiring a USPAP-compliant appraiser can provide defensible valuations to help shield against IRS audits. Residential appraisals typically cost $400 to $600, while commercial appraisals range from $1,000 to $3,000. Automated calculators can standardize income qualification processes, ensuring compliance with local source of income regulations.

"Greystar will stop using non-public data from other landlords to set rents." – NC Department of Justice

Additionally, review lease penalty clauses to ensure they meet "liquidated damages" standards. Courts often reject flat fees like "noise fines" or automatic "lockout fees" that don’t reflect actual costs. Conduct internal audits using six months of approval and denial data to identify and document disparities exceeding 10%.

Navigating these complexities is yet another challenge for real estate professionals tasked with maintaining compliance in an increasingly regulated environment.

7. Building Code Violations

Regulatory Impact

Building code violations can cause serious setbacks for property transactions and daily operations. Issues like blocked fire exits, overloaded electrical panels, or unpermitted construction often lead to Stop Work Orders, halting all activity until the problems are resolved. In some cases, municipalities may even revoke a property’s Certificate of Occupancy, forcing tenants to vacate the premises. Outstanding fines can escalate into municipal liens, which attach to the property title. This can create additional challenges, as most title companies refuse to issue insurance for properties with active violations, effectively stalling sales or refinancing efforts.

In light of disasters like the Champlain Towers South collapse, Florida has introduced mandatory Milestone Inspections for older buildings – those 30 years or older, or 25 years for buildings within three miles of the coast. These inspections must then be repeated every 10 years. Such regulations highlight the importance of staying ahead with routine maintenance, which is explored further in mitigation strategies.

Financial Penalties

The financial consequences of code violations can quickly spiral. Fines range from $100 to $1,000 per day, and repeated citations often lead to higher penalties. On top of that, significant liens and retroactive permit fees can dramatically inflate costs. For example, a review of ten properties in New York City uncovered $2.6 million in penalties tied to 240 unresolved violations. Under Florida’s Milestone Inspection law, failing to submit structural recertification reports can result in initial fines of around $510, which can climb to $10,000 per violation for ongoing non-compliance.

Unpermitted work can also become a costly headache. Property owners caught without the necessary permits may face retroactive fees that multiply the original cost by three to five times. One South Florida homeowner nearly lost an $850,000 sale in December 2025 due to a $6,500 lien for unpermitted work. The situation was resolved within 25 days, but only after expedited inspections.

Operational Disruptions

Unresolved violations don’t just hit the wallet – they can also disrupt operations in a big way. Insurance companies may cancel policies on properties with active code violations, leaving owners exposed to financial risks. Addressing violations discovered during property transactions can lead to emergency remediation costs that far exceed the price of regular maintenance. These situations often force owners to work under tight deadlines with limited contractor availability.

"A clean or nearly clean record is a quiet asset when you’re talking to lenders and high-quality buyers." – Alex Taylor, Violation Watch

Municipalities are also leveraging digital platforms for complaint submissions and mobile inspections, speeding up enforcement actions. Additionally, the Americans with Disabilities Act (ADA) mandates the removal of barriers in buildings constructed before 1990. Failing to comply can result in hefty penalties from the Department of Justice, sometimes reaching five figures.

Mitigation Strategies

To avoid these challenges, proactive maintenance is key. Regular building assessments every three years and annual safety walkthroughs can help identify potential issues before they escalate. Scheduling voluntary third-party inspections before listing a property is another smart move – it can uncover unpermitted work or maintenance problems that might surface during title searches.

Make sure contractors secure all necessary permits for structural, electrical, or plumbing work, as Florida law may hold property owners responsible for unpermitted work – even if a contractor completed the job. Keeping a centralized digital record of permits and inspection approvals for at least six years ensures easy access when needed. Lastly, train facility teams to spot immediate hazards like blocked exits, missing GFCIs, or obstructed sprinkler heads to prevent violations before they occur.

Environmental Law Section 101 Series – Navigating CERCLA Liability Risks in Real Estate Transactions

Conclusion

Each regulatory risk in real estate – whether it’s KYC/AML violations or building code issues – brings its own set of challenges. Compliance isn’t optional; it’s a critical safeguard that shields investments from steep financial and legal consequences. Consider this: KYC/AML violations alone can result in penalties exceeding $250,000, while liabilities tied to environmental contamination often climb into the millions. With global real estate money laundering estimated at $1.6 trillion annually and new regulations like FinCEN’s beneficial ownership reporting rule set to take effect on March 1, 2026, the compliance landscape is becoming more complex and demanding.

Skipping due diligence can lead to costs that far outweigh the price of preventive measures. Hidden liabilities – like federal tax liens or Superfund cleanup responsibilities – can saddle professionals with expenses that dwarf the property’s original value. Operational setbacks, such as stop work orders or revoked certificates of occupancy, can halt business activities and chip away at returns.

Leveraging automation and reliable data is key to staying ahead. Tools like BatchData simplify processes by verifying ownership, cross-referencing tax records, and flagging potential issues like liens or zoning conflicts. Transitioning from manual research to automated intelligence reduces human error, minimizes false positives, and grants a competitive edge. This approach not only mitigates risks but also strengthens market positioning.

"Compliance with KYC and AML regulations in real estate is not just about following rules – it’s about building a secure ecosystem where people can truly trust their transactions." – Didit

To stay compliant, maintain clear audit trails, use standardized checklists, and consult third-party experts to address concerns like property price manipulation or uncooperative buyers. Staying informed about regulatory deadlines and embracing automated solutions transforms compliance from a challenge into an opportunity to safeguard and grow your investments.

FAQs

Who must file under FinCEN’s RRE Rule in 2026?

Starting in 2026, anyone participating in non-financed residential real estate transfers to legal entities or trusts will need to comply with filing requirements under FinCEN’s RRE Rule. This applies to professionals like title agents, escrow agents, attorneys, and others managing these transactions.

What’s the fastest way to reduce privacy risk with client data?

The fastest way to minimize privacy risks with client data is by cutting down on data collection, retention, and exposure. Get rid of unneeded information as soon as possible, redact sensitive details before sharing them, and put clear, documented privacy guidelines in place to shape your workflows.

What due diligence should I run before closing to avoid hidden liabilities?

Before wrapping things up, it’s important to go over some key areas to avoid unexpected issues. Start by verifying the title and ownership to ensure there are no disputes. Next, check for any liens or unpaid taxes that could become your responsibility. Make sure the property complies with zoning regulations, and assess any environmental conditions that might affect its use or value. Finally, double-check that all necessary documentation is accurate and complete. Taking these steps during due diligence can help reduce risks and make the transaction process much smoother.