Most flipping companies don't fail in the rehab. They fail in acquisition. Experienced flippers are reported to have an 85% success rate with a target margin of 10 to 15% of ARV, and in 2022 house flipping represented 8.4% of all home sales with an average profit of $67,900 per flip, according to RFP Homes' house flipping guide. Those numbers are big enough to attract attention, but they also prove the point: this business rewards operators who build repeatable systems, not hobbyists who get lucky on one house.

A modern house flipping company is less a construction shop and more an acquisitions and underwriting machine. Renovation still matters. So do financing, sales, and contractor management. But the companies that stay alive through changing markets are the ones that know where to buy, what to pay, how fast to move, and when to walk.

| Core pillar | What matters in practice | What breaks first |

|---|---|---|

| Market selection | Picking submarkets with enough turnover, clean comps, and workable exits | Chasing “hot” zip codes without understanding resale friction |

| Deal sourcing | Building a lead pipeline across MLS, wholesalers, and direct-to-seller outreach | Waiting for obvious deals to hit the open market |

| Capital stack | Matching each deal to the right funding source and timeline | Using expensive money on slow projects |

| Project execution | Tight scope, reliable trades, disciplined change orders | Loose rehab plans and mid-project redesign |

| Tech stack | Clean data, lead management, underwriting, and reporting | Spreadsheet chaos and stale property records |

If you want a useful parallel, review AgentPulse's insights on real estate AI. The same shift is happening here. Operators are replacing guesswork with systems. For a deeper look at the analytics mindset behind that shift, real estate data analytics in practice is worth studying.

Introduction Why a House Flipping Company is Really a Data Company

The companies that keep flipping through tight spreads and choppy resale conditions do not win because they swing bigger hammers. They win because they buy better, price risk faster, and reject bad deals before those deals consume capital and staff time.

Beginner advice often frames flipping as a rehab business with some deal hunting on the side. That model breaks as soon as volume matters. A real house flipping company runs on acquisition flow, underwriting discipline, and current property data. Renovation is still important, but it sits downstream from the decision that matters most: whether the property should have been bought at all.

What experience actually looks like

Earlier results cited in this article already made the basic point. Skilled operators can make flipping work, but the edge comes from process, not optimism.

In practice, experience usually shows up in a few specific ways:

- Tighter buy decisions: The team knows when a “good enough” deal is a thin-margin mistake.

- Sharper scope planning: They can separate repairs that protect resale value from upgrades that only inflate the budget.

- Faster screening: They move through leads quickly because the criteria are already set.

Practical rule: If your team cannot evaluate opportunities quickly and the same way every time, you do not have a company. You have a series of isolated projects.

Why the edge in 2026 starts with data

By 2026, every operator claims to target distressed sellers. That is not an edge. The edge is having a system that ranks opportunities, flags risk early, and keeps the team focused on properties that fit the buy box.

That requires more than a spreadsheet and a few bookmarked MLS searches. It requires current ownership records, listing status, mortgage and lien visibility, neighborhood turnover patterns, comp quality, and a clear read on exit liquidity. Teams that study real estate data analytics for investors and operators usually reach the same conclusion. The acquisition side of the business determines whether the rehab side ever has a chance to perform.

I have seen this firsthand. Bad flips often look fine at the contractor walk-through stage. The underlying problem started earlier with weak comp selection, stale ownership data, or a resale assumption that did not hold once the property hit the market.

The operating system matters more than hustle

A solo flipper can survive for a while on instincts and long hours. A scalable company cannot. Once you are managing lead flow across MLS, wholesalers, direct mail, cold outreach, referrals, and repeat sellers, inconsistency gets expensive fast.

The companies that scale build a repeatable operating system:

- Acquisitions coverage across multiple lead channels, not one source of deal flow

- A defined buy box by property type, price point, geography, and exit profile

- Standard underwriting logic so two team members do not value the same deal two different ways

- Capital discipline tied to timeline risk and projected margin

- Clear project controls before the rehab starts

- Exit planning that accounts for more than the perfect retail resale

That is why this business now looks a lot like a data-driven operating company with a construction arm attached. Teams making that shift are following the same broader pattern covered in AgentPulse's insights on real estate AI. The winners use systems to reduce guesswork, speed up decisions, and keep standards consistent as volume grows.

How Do You Build the Company's Foundation

The foundation starts with two decisions. How the company is structured, and where it will buy. Get either one wrong and the rest of the machine gets noisy fast.

In Q1 2025, 67,394 U.S. homes were flipped, representing 8.3% of all sales, according to ATTOM reporting cited by REI Ink. That volume still matters, but the same report also shows flipping is cyclical. A house flipping company needs a setup that can handle volume swings, not just good months.

Choose a legal structure that matches risk

Most operators start with an LLC because liability isolation matters when you're buying property, hiring contractors, and taking on project risk. Some teams later elect S-Corp taxation for tax treatment reasons, but that decision belongs with a qualified CPA and attorney who understand real estate operations.

The practical point is simpler than the entity debate online:

- Use a clean entity structure: Don't buy houses personally and sort it out later.

- Separate operating accounts: Every project should have clear accounting.

- Use written agreements: Especially if you have partners, lenders, or revenue-sharing arrangements.

- Document authority: Someone must clearly control offers, vendor approvals, and fund releases.

A sloppy company structure creates expensive problems. Not dramatic ones at first. Small ones. Payment disputes, unclear ownership, bad books, weak lender confidence.

For operators building a disciplined business plan, Constructo Marketing business insights offer a useful model for thinking about systems, roles, and operational accountability.

Pick a market with enough signal

Choosing markets by vibe is a common mistake. A flipping company needs a market where you can source enough opportunities, comp them with confidence, and exit without guessing.

Start with a few practical filters:

| Market question | Why it matters | Bad sign |

|---|---|---|

| Are there enough resales? | You need turnover for comps and exits | Sparse sales and stale pricing |

| Are renovated homes moving? | Your buyer needs proof of demand | Nice rehabs sitting too long |

| Are price bands clear? | Tight comp ranges improve underwriting | Wild pricing with no pattern |

| Is investor activity visible? | It shows existing appetite and competition | Either no activity or irrational bidding |

Build a real buy box

Your buy box is the property profile your team is allowed to pursue. Without one, people chase shiny objects.

A good buy box usually defines:

- Property type: Single-family, condo, small multifamily

- Location: Specific zip codes, school zones, or subdivisions

- Condition range: Cosmetic only, moderate rehab, or heavy value-add

- Exit buyer: First-time buyer, move-up buyer, investor

- Deal blockers: Foundation issues, awkward layouts, title complexity, permit sensitivity

A company with no buy box starts underwriting everything. That kills time, morale, and offer quality.

Use market data as a risk control

The job isn't finding the “best” market. The job is finding a market your team can understand thoroughly enough to buy with conviction. That means tracking listing age, resale behavior, ownership patterns, and how quickly your target buyer moves.

The strongest operators narrow their footprint first. Scale comes later.

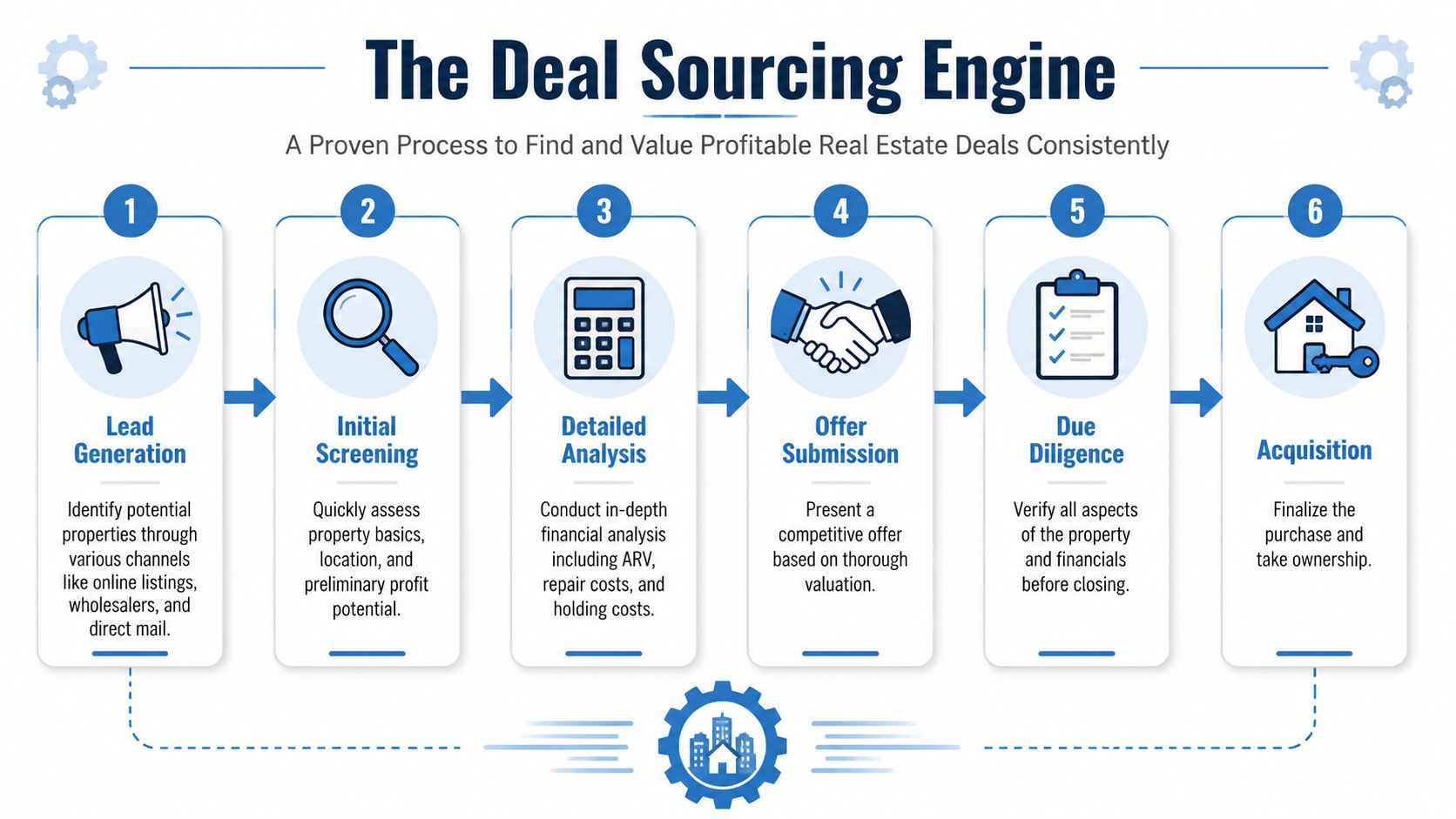

What is the Engine for Sourcing and Valuing Deals

Your acquisition engine is the business. Not the logo, not the contractor list, not the kitchen finishes. If your company can't produce a steady stream of qualified opportunities and value them correctly, everything else becomes expensive theater.

A technically defensible workflow starts with the 70% rule: maximum purchase price = 70% of after-repair value minus estimated repair costs, as explained by Rocket Mortgage's guide to the 70% rule. Their example uses an ARV of $220,000 and repairs of $40,000, producing a maximum purchase price of $114,000. That's a useful guardrail. It is not a substitute for real underwriting.

Why single-channel sourcing stops working

A lot of new operators rely too heavily on the MLS. That works until competition compresses the spread. Once that happens, every average deal gets bid up and every mistake gets punished.

A scalable house flipping company usually sources from multiple channels:

- MLS and stale listings: Good for visible inventory, price drops, failed listings, and agent outreach

- Wholesalers: Useful when you can screen fast and reject aggressively

- Direct-to-seller outreach: Better for building your own pipeline instead of renting someone else's

- Foreclosure and trustee-related opportunities: Strong in some markets, but process-heavy

- Agent relationships: Underused by beginners, highly productive for operators who respond quickly

What matters isn't just channel count. It's the speed and consistency of follow-up.

The data stack that creates speed

Generic advice says “find distressed homes.” That doesn't help an acquisitions manager at scale. Real sourcing needs current records and filters that narrow attention to the owners and properties most likely to produce a workable deal.

That usually means tracking:

- Listing status and days on market

- Ownership history

- Mortgage and lien context

- Equity picture

- Property condition indicators

- Contactability

For firms that need that workflow in one place, BatchData provides property, owner, lien, and listing data that can support sourcing, underwriting, and outreach. If you want a practical primer on one part of that valuation layer, what an AVM means in real estate is a useful starting point.

The real edge isn't knowing that distressed inventory exists. It's knowing which record deserves attention before your competitors call.

A short underwriting video can help align your team on process before they touch live deals:

Underwrite in layers, not in one pass

The biggest valuation mistake is pretending the first comp set is the answer. It isn't. Strong operators underwrite in layers.

Layer one is the screen.

Can the property fit the buy box at all? If not, reject it fast.

Layer two is ARV.

Use comparable renovated sales, not hopeful listings. Adjust for layout, finish quality, lot characteristics, and buyer profile.

Layer three is scope.

Walk the property with a real checklist. Roof, foundation, HVAC, electrical, plumbing, windows, layout friction, deferred maintenance. Cosmetic assumptions destroy margin when the mechanicals are wrong.

Layer four is carry and exit stress.

Add financing cost, utilities, insurance, taxes, closing costs, resale friction, and downside if buyer demand softens.

A simple acquisition workflow that scales

| Stage | What the team should do | Common mistake |

|---|---|---|

| Lead intake | Pull core property and owner facts fast | Reviewing every lead manually |

| Initial screen | Check buy box, rough ARV, obvious blockers | Spending an hour on weak leads |

| Field review | Confirm condition and repair scope | Trusting seller descriptions |

| Full underwrite | Model purchase, rehab, carry, and exit | Ignoring downside scenarios |

| Offer | Present a clean number with terms that solve a seller problem | Negotiating against yourself |

| Follow-up | Revisit leads that don't convert immediately | Assuming no means never |

What works and what doesn't

What works is boring. Tight filters. Fast outreach. Conservative ARV. Honest repair scoping. Immediate rejection of weak deals.

What doesn't work is also predictable. Chasing every wholesale blast, comping off active listings, using the 70% rule as if it were exact, and making offers without understanding title, condition, or exit liquidity.

A house flipping company scales when acquisition becomes a system. Until then, it's just reacting to whatever shows up.

How Should You Structure the Capital Stack for Flips

A profitable deal on paper is worthless if your company can't close fast enough or fund the rehab cleanly. Capital stack decisions affect margin, timeline, and negotiating advantage. They also affect what kinds of deals your company can realistically pursue.

The right funding source depends on speed, certainty, and how much operational control you need. A heavy rehab with a short close window doesn't belong with the same capital strategy as a clean cosmetic project.

House Flip Financing Options Comparison

| Funding Source | Typical LTV/LTC | Interest Rate/Points | Speed to Close | Best For |

|---|---|---|---|---|

| Traditional bank loan | Varies by lender and borrower profile | Usually lower-cost than hard money, but underwriting is stricter | Slower | Borrowers with strong financials, cleaner properties, less time pressure |

| Hard money lender | Varies by lender, asset, and experience level | Usually higher-cost, often with points and shorter terms | Fast | Competitive purchases, distressed assets, short close windows |

| Private money | Negotiated deal by deal | Negotiated between parties | Can be fast if relationship is established | Operators with trust-based investor relationships and flexible structures |

| Self-funding | Not applicable | No lender interest, but capital has an opportunity cost | Immediate once funds are available | Small portfolios, high-control buyers, lower volume operations |

| Partnership equity | Depends on structure | Profit sharing instead of standard loan pricing | Moderate, depends on partner alignment | Teams lacking full capital but strong on sourcing and execution |

What each option is really buying you

Bank financing buys cheaper capital, but it usually costs you time and flexibility. That's fine when the asset is straightforward and the seller isn't demanding speed.

Hard money buys speed and certainty. You pay for that speed. On the right deal, that trade-off makes sense. On a slow project, expensive money can squeeze the life out of the spread.

Private money is attractive when you've built credibility and can explain your process clearly. The primary value is flexibility. The primary risk is weak documentation or unrealistic expectations.

Match the money to the job

Use a simple decision filter:

- Need to close fast? Hard money or established private capital usually fits better.

- Need flexibility on draw structure? Private money can be easier to tailor.

- Working on a lighter rehab with time to spare? Bank debt may improve margins.

- Trying to scale volume? You need more than one source. One lender is not a capital stack.

Cheap money that arrives late is often more expensive than fast money that lets you capture the deal.

The common financing mistake is emotional loyalty to one source. Strong operators stay lender-diverse. They know who can close fast, who requires cleaner files, who works on tougher assets, and who will still fund when a deal gets complicated.

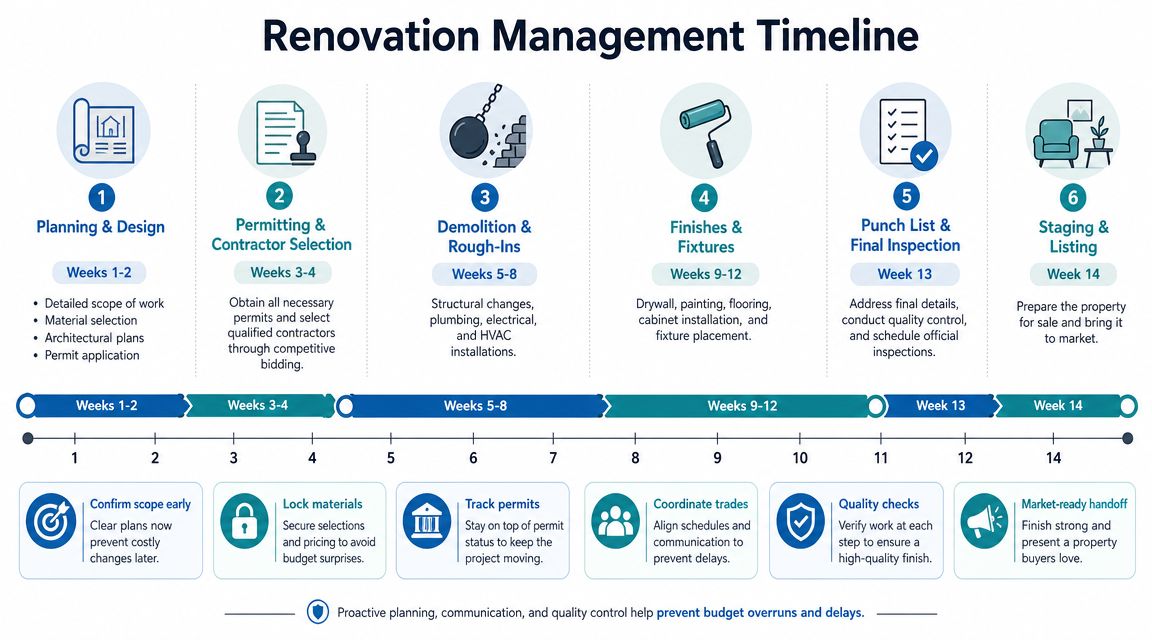

How Do You Systematize Renovation Management

Renovation is where many flipping companies give back the profit they created in acquisition. The pattern is familiar. Scope is vague, contractor communication is loose, decisions happen in the field, and the budget drifts one “small upgrade” at a time.

The fix isn't working harder on site. The fix is running a tighter system before work starts.

Lock the scope before demolition

A serious rehab starts with a statement of work, not a vague conversation. The SOW should define exactly what is being repaired, replaced, installed, painted, moved, or left alone.

At minimum, your SOW should cover:

- Exterior items: Roof, siding, drainage, windows, doors, paint, landscaping

- Mechanical systems: Plumbing, electrical, HVAC, water heater, panel work

- Interior finish standards: Flooring type, cabinet spec, countertop material, paint grade, trim package

- Layout changes: Wall removal, room additions, bathroom conversions, kitchen reconfiguration

- Permit-triggering work: Anything that can slow the job if ignored

If it isn't written down, expect disagreement later.

Build the budget line by line

Don't use a rehab budget that says “kitchen,” “bathrooms,” and “miscellaneous.” That's not a budget. That's hope.

A working renovation budget should break out labor and materials by trade and by phase. It should also include a contingency reserve. The point of contingency isn't to encourage sloppy planning. It's to keep one surprise from blowing up the entire job.

A useful budget structure looks like this:

| Budget bucket | What to include | Why it matters |

|---|---|---|

| Pre-construction | Demo, dumpsters, permits, inspections, design changes | These costs show up before the visible progress |

| Core trades | Framing, plumbing, electrical, HVAC, roofing | The expensive mistakes usually happen here |

| Finishes | Cabinets, countertops, flooring, paint, fixtures, appliances | Scope creep hides in finish selections |

| Closeout | Cleaning, punch list, staging prep, listing readiness | Projects often stall at the very end |

Manage contractors with milestones, not trust alone

Good contractors matter. So do written controls. Even strong crews need clear expectations on schedule, payment, quality, and communication.

Use this operating approach:

- Bid from a written scope. Bids are useless if every contractor priced a different job.

- Use milestone payments. Tie draw releases to completed work, not calendar dates.

- Require change orders in writing. No verbal “while we're here” upgrades.

- Inspect weekly. Photos help. Site walks matter more.

- Track material decisions early. Delays often come from late fixture and finish selections.

The fastest way to lose control of a rehab is letting the project manager, contractor, and acquisitions person carry different versions of the plan.

What actually protects margin

The winning move on most flips isn't making the house nicer. It's making it easier to sell at the right standard for that submarket. Over-renovation is a real tax on inexperienced operators.

Protecting margin usually comes down to three disciplines:

- Fix what buyers notice and appraisers support

- Avoid custom work unless the neighborhood justifies it

- Finish cleanly instead of endlessly upgrading

The rehab should serve the exit. Not your personal taste, not your contractor's preferences, and not some fantasy comp no buyer has proven.

What Are the Best Disposition and Exit Strategies

Disposition starts before you close on the purchase. If your company only has one exit plan, you're taking more risk than you think.

The default path is still a traditional resale with an agent. That works when the property fits the buyer pool, the pricing is disciplined, and the market is liquid enough to absorb another renovated listing. But smart operators always keep backup exits ready.

The primary exit for most flips

A standard retail listing usually gives you the broadest buyer pool. To make that path work, focus on execution, not just exposure.

That means:

- Choose an agent who knows investor resale comps

- Price from the actual market, not your break-even need

- Use professional photography and clean staging

- Launch with a complete property story, not half-finished marketing

- Respond fast during inspection and appraisal

A lot of flippers lose money at the end because they treat listing as a formality. It isn't. The disposition phase is where your spread becomes cash.

Backup exits reduce bad decisions

If the retail exit gets weaker, the company needs options. Useful frameworks for thinking through those alternatives appear in investment exit strategies for 2025, especially for operators who need flexibility across changing market conditions.

Common backup exits include:

| Exit path | When it fits | Trade-off |

|---|---|---|

| Retail resale | Strong buyer demand, clean finishes, financeable asset | Most exposed to buyer sentiment and inspection noise |

| Sale to another investor | Retail demand softens or project isn't ideal for owner-occupants | Usually lower upside |

| Seller financing | Property or buyer pool needs more flexible terms | More complexity and longer collection horizon |

| Hold as rental | Retail spread shrinks but cash-flow or long-term hold still works | Capital stays tied up |

Watch distressed resale channels too

Some operators overlook trustee-related opportunities on the buy side and the exit side. Understanding how those sales work helps with acquisition timing, title review, and competitive positioning. If your market includes foreclosure-related inventory, what a trustee's sale means in real estate is worth understanding.

The key disposition rule is simple. Don't wait until the listing goes live to decide what your alternatives are. If the market shifts, indecision gets expensive fast.

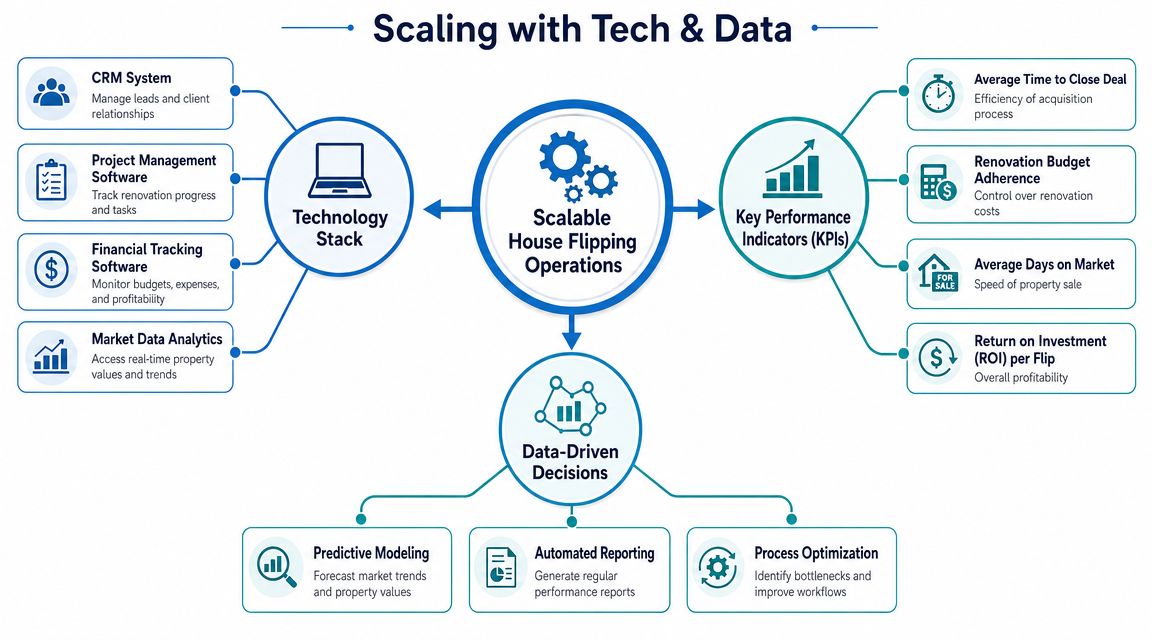

How Do You Scale with a Modern Tech and Data Stack

Scale comes from repeatable decisions. A house flipping company that wins in 2026 is built more like an acquisitions and risk management platform than a construction shop. Renovation still matters, but it sits downstream from lead quality, valuation discipline, and capital velocity.

That matters most when spreads tighten. Operators who keep buying on old assumptions get punished fast. Recent practitioner guidance points to stricter underwriting and wider discounts, and that only works if your team can track local sales velocity, permit friction, and liquidation risk in near real time, as discussed in this market risk discussion for flippers.

The minimum operating stack

A scalable stack does one job well. It keeps acquisitions, rehab, finance, and disposition working from the same property record.

That does not require a huge software bill. It requires clean handoffs, clear ownership, and one source of truth.

A practical setup usually includes:

- CRM: HubSpot, Pipedrive, or another system that tracks lead source, status, follow-up cadence, and seller communication

- Project management: Asana, Trello, Monday.com, or Buildertrend for rehab tasks, approvals, change orders, and deadlines

- Accounting: QuickBooks or a comparable system with project-level job costing and draw tracking

- Shared documentation: Google Drive, Dropbox, or a structured file system for scopes, bids, photos, permits, insurance, and closing docs

- Property data layer: A source for ownership, liens, listing changes, equity signals, and valuation support

I see the same failure pattern over and over. The acquisitions team works from one set of notes, construction keeps a separate spreadsheet, and finance closes the month with stale numbers. Once that happens, management loses the ability to see margin drift early.

Track KPIs that change behavior

Back-end profit reports are useful for accounting. They are weak operating tools.

A management dashboard should show where the system is slowing down before the project reaches the closing table. Focus on a short list of metrics your team can act on every week.

| KPI | What it tells you | Why it matters |

|---|---|---|

| Lead-to-offer rate | How efficiently the team screens opportunities | Low conversion often points to weak list quality or a buy box that is too broad |

| Offer-to-contract rate | Whether pricing, follow-up, and seller handling are working | Soft conversion can mean your pricing is off or your reps are losing motivated sellers |

| Average project cycle time | How quickly capital turns | Longer turns reduce annualized returns and create financing pressure |

| Budget adherence | Whether rehab execution is under control | Repeated overruns usually come from poor scopes, weak bid discipline, or contractor drift |

| Days on market after listing | Exit efficiency and pricing discipline | Slow exits erode margin through carrying costs and price cuts |

One sentence matters here. Every KPI needs an owner. If no one is responsible for improving a metric, the dashboard becomes decoration.

Data should drive operating decisions

Collection is easy. Standardizing decisions is harder.

Use your stack to run closed-loop feedback across the business:

- Acquisitions: Narrow or expand the buy box based on contract conversion, rehab variance, and resale performance by submarket

- Renovation: Identify contractors, materials packages, and scope categories that create delays or change-order creep

- Dispositions: Adjust pricing and timing faster when comparable absorption weakens

- Capital allocation: Send capital toward deal types and neighborhoods that turn cleanly with fewer surprises

Scaling typically falters at this stage. Teams add volume before they build feedback loops. Then they mistake activity for throughput.

A good system answers practical questions fast. Which lead source is producing signed contracts at acceptable margins. Which ZIP codes are creating the most permit drag. Which PM is delivering projects closest to budget. Which exit type is slowing capital recycling.

Build for resilience, not just volume

A company can look efficient during a forgiving cycle and still be fragile. Rising insurance, slower permits, tighter labor, and longer marketing times expose weak systems fast.

The operators that hold margin have structure around a few hard rules:

- Buy tighter when uncertainty rises

- Favor cleaner scopes over heroic renovations

- Underwrite longer hold times before the deal is approved

- Set backup exits before closing

- Escalate stalled jobs and stale listings early

That difference shows up at the company level. A hustle asks whether one deal can be saved. The business asks whether the model still works when debt costs stay high and exits slow down.

If you're building a house flipping company that depends on clean acquisition data, current ownership records, and faster underwriting, BatchData is worth evaluating as part of your operating stack. The platform is built for real estate teams that need property records, valuations, owner contacts, lien and listing data, and workflow support for sourcing, due diligence, and portfolio monitoring at scale.