SEO Title: Homeowners Title Insurance Cost & Coverage | A Complete Guide

Meta Description: Understand homeowners title insurance costs, why you need an owner's policy vs. a lender's, and how it protects your equity from hidden title defects like liens.

Meta Keywords: homeowners title insurance, what is title insurance, title insurance cost, owner's policy, lender's title insurance, title defects, title claim

Buying a home without homeowners title insurance is like buying a used car without checking if it was ever stolen—it's a gamble against the property's entire hidden history. Homeowners title insurance is a one-time policy that defends your legal ownership rights against financial loss from past events like fraud, undisclosed heirs, or unknown liens. This isn't optional protection; it's the fundamental backstop for your most significant investment.

Unlike insurance that covers future accidents, title insurance is retrospective, shielding you from problems that already exist in the property's title history. It pays for your legal defense and covers financial losses if someone challenges your ownership.

- Core Takeaway: You need an owner's policy. The lender's policy only protects the bank.

- Cost Basis: A one-time fee, typically 0.5% to 1.0% of the home's purchase price.

- Primary Risk: Protects against hidden defects a standard title search can miss, found in an estimated 30% of transactions.

This guide breaks down exactly how it works, what it costs, and why it's a non-negotiable part of modern homeownership.

What Is Homeowners Title Insurance and Why Do I Need It?

Homeowners title insurance is a policy that defends your ownership rights against any claims or issues from the property's past. Before a policy is issued, a title company performs an exhaustive search of public records—deeds, mortgages, tax records, and court judgments—to verify the seller can legally transfer the title to you. To get a foundational understanding of the concept, it's worth exploring what is title insurance in a bit more detail.

Why the Title Search Is Not Enough

Even the most meticulous search cannot unearth every potential problem. The real value of homeowners title insurance is its protection against the unknown—the hidden risks that don't appear in public records.

These are issues that can surface years after you've moved in:

- Forgery & Fraud: A document in the property’s chain of title was forged, or signed by an imposter.

- Undisclosed Heirs: A long-lost heir of a previous owner appears with a legitimate claim to the property.

- Filing Errors: Clerical mistakes in public records cause disputes over who truly owns the property.

- Unknown Liens: A prior owner failed to pay a contractor or property taxes, leaving a debt (a lien) attached to the property—which is now your problem.

A title search is designed to disclose potential defects ahead of time, but it's not a guarantee. The insurance policy is the actual financial backstop that covers losses and legal fees if a hidden risk surfaces and challenges your ownership.

Owner's Policy vs. Lender's Policy

There are two distinct types of title insurance, and understanding the difference is critical. Your mortgage company will mandate you buy a lender's policy, but this policy only protects the bank's financial interest in the property, not your equity. To protect your own investment, you need a separate owner's policy. For a deeper dive, our guide on lender's title insurance breaks down its specific purpose.

| Feature | Owner's Policy | Lender's Policy |

|---|---|---|

| Who It Protects | The homeowner (you) | The mortgage lender (the bank) |

| Coverage Focus | Your equity in the property | The outstanding loan amount |

| Requirement | Optional, but essential | Mandatory for most mortgages |

| Payment Type | One-time premium paid at closing | One-time premium paid at closing |

| Policy Duration | Lasts as long as you or your heirs own the property | Lasts until the mortgage is paid off |

Skipping an owner's policy is a massive gamble. With title issues cropping up in an estimated 30% of real estate transactions, the protection is invaluable. The global title insurance industry is projected to hit $4.15 billion by 2033, driven largely by the U.S. market, which sees over 4 million home sales annually. For insurance carriers and real estate pros using platforms like BatchData, these numbers point to a huge and consistent opportunity. You can see a full breakdown in this detailed title insurance report.

An owner's policy serves two functions: first, it pays the legal bills to defend your title in court. Second, if a claim is valid, it covers your financial loss up to the home's purchase price.

Standard vs. Enhanced Policy

A standard policy is your foundational shield, but an enhanced policy offers a wider net of protection for a slightly higher one-time premium. It covers specific problems that might only surface after you buy the home. For example, an enhanced policy often covers post-policy forgery, where someone tries to fraudulently transfer your title after you've already bought the home, and building permit violations from previous owners.

| Coverage Area | Standard Policy | Enhanced Policy |

|---|---|---|

| Basic Title Defects | Covered (Forgery, liens, errors before purchase) | Covered (Includes all standard protections) |

| Post-Policy Forgery | Not Covered | Covered |

| Building Permit Violations | Not Covered | Covered |

| Subdivision Map Act Issues | Not Covered | Covered |

| Forced Removal of Structure | Covered in limited cases | Covered (For encroachments or zoning issues) |

What Are the Most Common Title Defects?

A title defect is any unresolved claim that calls your right to the property into question. These issues are often invisible during a standard inspection but can emerge years later, turning the dream of homeownership into a costly legal nightmare. The power of homeowners title insurance is how it protects you from these invisible threats.

Unknown Liens and Encumbrances

This is the most common source of title claims. A lien is a legal claim against your property for an unpaid debt, and it stays attached to the property after a sale.

- Contractor Liens: A prior owner fails to pay a contractor for a $15,000 new roof installed right before the sale. That debt could legally become your problem.

- Tax Liens: A previous owner skipped out on property or federal income taxes. The government can place a lien on the property to collect the debt, which takes priority over nearly all other claims.

- Undiscovered Easements: You discover a utility company has a recorded right to dig up your backyard, or a neighbor has a legal path through your driveway, derailing your plans for a new fence.

Title insurance acts as your financial shield. If a valid, previously unknown lien appears, your policy steps in to resolve it, often by paying the debt to clear your title.

Forgery and Document Fraud

Criminal activity in a property’s history can create devastating title issues. A scammer could have forged a dead owner’s signature on a deed years ago, “selling” the property to an accomplice. This single illegal act creates a fatal flaw in the title’s history. When the original owner’s legitimate heirs discover the fraud, they can sue for the property, leaving you in a legal war. For a deeper look, it’s worth reading about quiet title actions.

Clerical Errors and Missing Heirs

Not every defect is malicious. Some result from simple human error or complex family situations.

- Filing Errors: A clerk at the county recorder’s office mistyped a detail or misfiled a document decades ago. This small mistake can create a gap in the ownership chain that clouds your title.

- Missing Heirs: A previous owner dies without a will. Years later, a forgotten cousin or an unknown child appears with a valid claim to a piece of the property, challenging your status as the sole owner.

These scenarios show how vulnerable you are to events that happened long before you saw the house. You can explore other common home title problems to understand the full scope of risks.

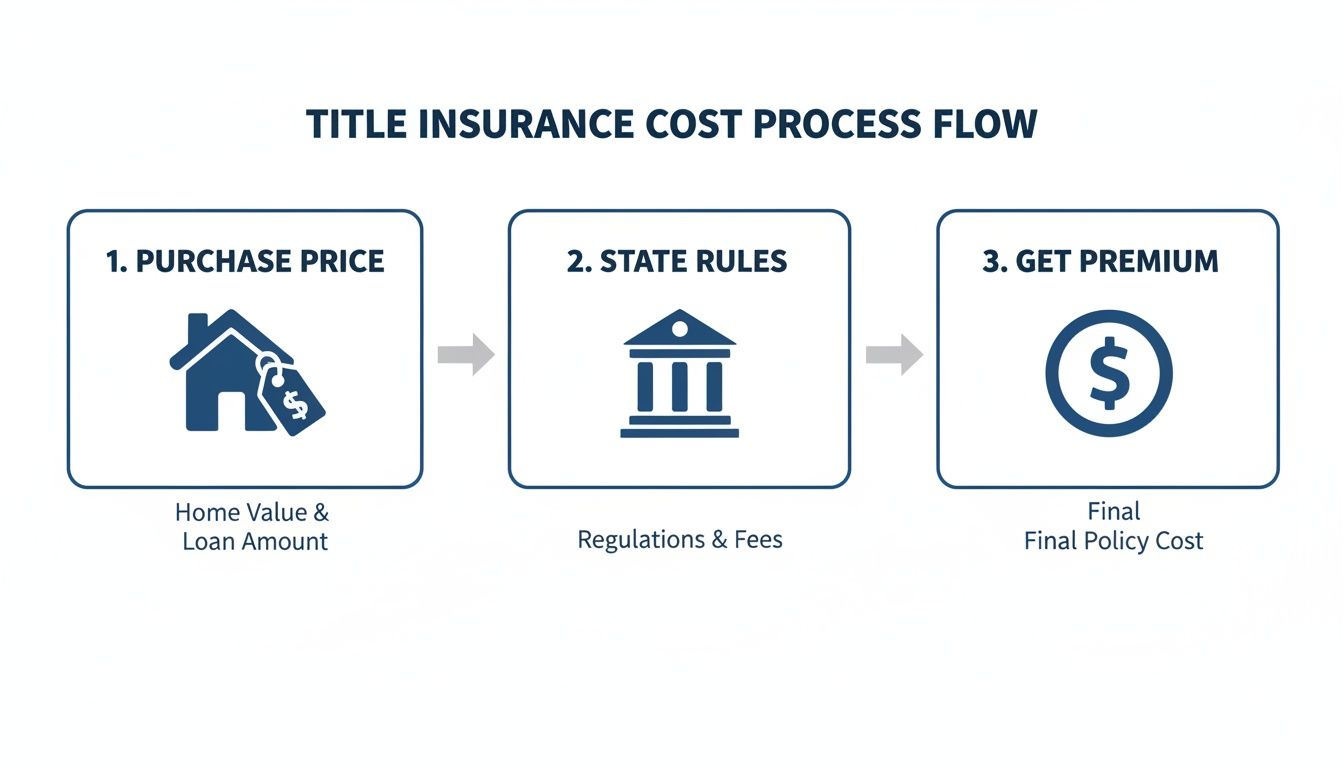

How Is the Cost of Homeowners Title Insurance Determined?

The cost of homeowners title insurance is a one-time premium paid at closing that protects your ownership rights for as long as you or your heirs own the property. The price is determined by two main factors: the purchase price of your home and the regulations in your state.

The home's value is the biggest driver; the more expensive the property, the more financial risk the insurer takes on, so the premium scales up. In some states, governments set fixed "promulgated rates," while in others, insurers compete on price, allowing you to shop around.

Your premium directly reflects the property's value and your location. The fee isn't just for the policy; it covers the exhaustive title search, expert examination of historical records, and the insurance itself.

Estimated Costs and Potential Savings

As a general rule, the one-time premium for an owner's policy falls between 0.5% and 1.0% of the home's purchase price. For a $400,000 home, that works out to between $2,000 and $4,000.

| Home Purchase Price | Estimated One-Time Premium Range (0.5% – 1.0%) |

|---|---|

| $250,000 | $1,250 – $2,500 |

| $500,000 | $2,500 – $5,000 |

| $750,000 | $3,750 – $7,500 |

| $1,000,000 | $5,000 – $10,000 |

You can often reduce this cost with a reissue rate. If the property was sold within the last 5-10 years and already has a title policy, the insurer can offer a significant discount because much of the title search work is already complete. Always ask your title company about reissue rates and bundling discounts (buying the owner's and lender's policies together).

After a market contraction, projections show industry-wide revenue growing by about 5% in 2026 as home sales rebound. For homeowners, this signals a stable shield against over 60 different types of title defects, which lead to roughly $1.5 billion in claims being paid out in the U.S. each year. You can get more details in this 2026 title revenue report.

How Does Property Data Modernize Title Due Diligence?

The traditional title search process is a notorious bottleneck, involving a manual grind through fragmented, outdated public records. The industry is now shifting to proactive, data-driven strategies using property data platforms.

Instead of sending runners to pull dusty files from county offices, modern platforms like BatchData use APIs to aggregate, clean, and deliver a unified stream of property information. This creates a single source of truth, allowing professionals to move faster and with greater confidence.

Automating Risk and Accelerating Decisions

The real game-changer is automation. With instant access to over 1,000 data points for any property, underwriters can build predictive risk scores.

This detailed data includes:

- Complete Ownership History: A clean, chronological record of every transfer that instantly flags gaps or unusual activity.

- All Active Liens: Immediate visibility into mortgages, HELOCs, contractor liens, or tax liens.

- Pre-Foreclosure and Foreclosure Status: Real-time alerts when a property is in distress.

By plugging this data directly into their systems, insurers can automatically flag high-risk files for human review while low-risk properties sail through. This cuts review times by up to 50% and frees up experienced underwriters to focus on complex deals.

For investors buying at scale, this speed is a massive competitive edge. Instead of waiting on slow, one-off searches, they can analyze entire portfolios in minutes, spotting hidden title issues before committing capital. It transforms the entire real estate due diligence checklist from a manual chore into an automated, data-validated process.

From Reactive Claims to Proactive Prevention

Ultimately, high-quality property data marks a fundamental shift from reacting to claims to preventing them. A homeowners title insurance policy is a critical safety net, but the industry's real goal is to reduce the number of things that go wrong in the first place.

Platforms like BatchData give professionals the tools to do exactly that, offering a clear, comprehensive look at a property's entire story.

This kind of interface shows how accessible property intelligence has become, letting users size up opportunities and risks instantly. This empowers lenders to underwrite with more certainty, insurers to price risk accurately, and investors to close deals with confidence.

What Do I Do When I Need to File a Title Insurance Claim?

Receiving a legal notice that challenges your ownership rights is exactly the moment your homeowners title insurance policy was designed for. The process starts the second you receive any communication questioning your right to the property.

Act fast. Do not ignore the notice or try to solve the problem yourself. Your policy is a legal and financial shield, but you must be the one to raise it.

Initial Steps in Filing a Claim

The first 48 hours after receiving a notice are critical. Your job is to get the problem into the hands of your title insurance company.

- Contact Your Insurer Immediately: Pull out your owner's title insurance policy from your closing documents. It will have the underwriter's name and claims department contact info. Call them without delay.

- Submit All Documentation: The insurer will require a formal "Notice of Claim" in writing. Send them a copy of the legal notice, your policy number, and any other relevant documents.

- Cooperate Fully: Your insurer will assign a professional to investigate. Your cooperation is mandatory. Provide any requested information quickly.

This is precisely why you must keep your closing documents in a safe, accessible place. Your owner's title insurance policy is the key to unlocking your financial protection.

Understanding the Resolution Pathways

Once the insurer investigates, the process moves toward a resolution, typically following one of two paths.

- If the Claim is Invalid: The insurer’s "duty to defend" kicks in. They will hire and pay for an attorney to represent you in court and work to have the claim dismissed. You pay nothing for these legal fees.

- If the Claim is Valid: The insurer will step in to "cure" the title defect. This might involve paying off an undiscovered lien, negotiating the release of an easement, or taking whatever action is needed to clear your title.

In a worst-case scenario where the defect cannot be fixed (e.g., serious fraud where you lose the property), the insurer will pay for your financial loss up to the full face value of your policy, which is typically the price you paid for your home.

Frequently Asked Questions About Title Insurance

Here are direct answers to the most common questions about homeowners title insurance.

Is homeowners title insurance required by law?

No, an owner's policy is not legally required. However, your lender will almost certainly mandate a lender's policy to protect their loan. Skipping the owner's policy to save a small one-time fee leaves your entire equity investment exposed to past title defects.

How long does my title insurance coverage last?

An owner's title insurance policy protects you and your heirs for as long as you own the property. It is a one-time fee paid at closing that delivers a lifetime of security against issues from the property's past. The policy does not expire.

Can a title claim really happen after I close?

Yes, and it happens more often than people think. Even with a diligent title search, issues can surface months or years later. These hidden threats are what homeowners title insurance is designed to handle. Examples include a mechanic's lien from a prior owner's unpaid contractor, a forged signature on a 20-year-old deed, or a clerical error at the county recorder's office that clouds your title.

What is the difference between standard and enhanced policies?

A standard policy covers a wide range of problems that existed before your purchase, like unknown liens and ownership claims. An enhanced policy costs slightly more upfront but expands protection to include certain future risks.

| Feature Covered | Standard Policy | Enhanced Policy |

|---|---|---|

| Post-Policy Forgery | No | Yes |

| Building Permit Violations | No | Yes |

| Zoning Mismatches | No | Yes |

| Forced Removal of Structures | Limited | Yes |

An enhanced policy gives you broader peace of mind, covering issues like a neighbor building a fence that encroaches on your property line after you’ve closed. For the small, one-time cost difference, most homeowners find the extra security is well worth it.

Ready to transform your real estate operations with superior property intelligence? With BatchData, you can access over 155 million property records to automate underwriting, accelerate due diligence, and mitigate risk before it becomes a claim. Empower your team with the most accurate and comprehensive data available. Explore the platform at https://batchdata.io.