Franklin County property tax analysis breaks down fast if you start with one countywide number. The county average is useful for screening, but billing risk sits at the parcel level, where school districts, municipalities, and other taxing authorities change the final rate.

That distinction matters in Columbus more than many buyers expect. Two properties with similar market values can carry meaningfully different tax loads because they sit in different taxing districts. For underwriting, appeals review, or product design, a single "Franklin County Ohio tax rate" is a rough benchmark, not an input you can trust on its own.

I treat countywide figures as a market signal. I treat parcel-level district data as operating data.

Quick takeaways

- There is no single professional-use Franklin County property tax rate. Accurate estimates depend on the parcel's assessed value, classification, and taxing district.

- District variability drives the spread. If your model ignores school district and local levy differences, projected taxes will miss actual carrying costs.

- Sales tax is a separate question. Franklin County's combined sales tax varies by jurisdiction, which matters for retail underwriting and tenant cost analysis, as shown by TaxHero's county breakdown.

- County averages still have value. They help compare Franklin County with other Ohio counties, but they do not replace parcel research during due diligence.

- Parcel-level tooling matters. Buyers, lenders, and proptech teams need address-specific tax data, not a recycled county average. For market context and inventory discovery, Cyber Homes' Columbus real estate solutions can support the front end of that workflow.

The practical question is simple: which taxing district applies to this parcel, and how does that district change the bill? That is the difference between a quick estimate and a usable tax projection.

An Introduction to Franklin County's Tax Landscape

A one-line "Franklin County Ohio tax rate" can miss the mark by a wide margin because the bill is set at the taxing-district level, not by a single county figure.

That distinction matters immediately in underwriting. Two parcels with similar values can carry different annual tax loads if they sit in different school districts, municipalities, or special levy areas. For investors, that changes yield and debt coverage. For a proptech team, it changes whether the product produces a rough market signal or a usable estimate.

Franklin County also forces a basic but important split between real property taxes and sales taxes. Property taxes attach to the parcel and depend on valuation, classification, and the applicable taxing district. Sales taxes apply to transactions and follow a different jurisdictional stack. Mixing those two systems in analysis creates bad comps, weak operating assumptions, and avoidable diligence errors.

Countywide averages still have a place. They help compare Franklin County with other Ohio counties and give analysts a first pass on tax burden at the market level. They do not tell you what a specific parcel will owe, and they should never be treated as a billing proxy.

I use county figures for screening. I use district and parcel records for pricing risk.

That is the practical divide. A developer evaluating two sites in the Columbus area may be looking at similar rents, similar lot sizes, and similar exit assumptions, but the tax line can still diverge enough to affect land residuals or stabilized value. If you need neighborhood context before you move into parcel research, Cyber Homes' Columbus real estate solutions can support that first pass. The tax estimate still has to come from the parcel's actual district setup.

What professionals need to confirm first

A usable Franklin County tax workflow starts with three checks:

- Identify the tax type. Property tax and sales tax are separate systems with different governing jurisdictions.

- Identify the controlling geography. County labels are too broad for valuation work. The taxing district usually drives the property rate that matters.

- Identify the authoritative record. Parcel tax work should trace back to county parcel and district records, not a recycled county average from a listing feed or summary table.

Those checks sound basic. In practice, they separate a quick approximation from analysis you can defend in an investment memo or build into a reliable tax-data product.

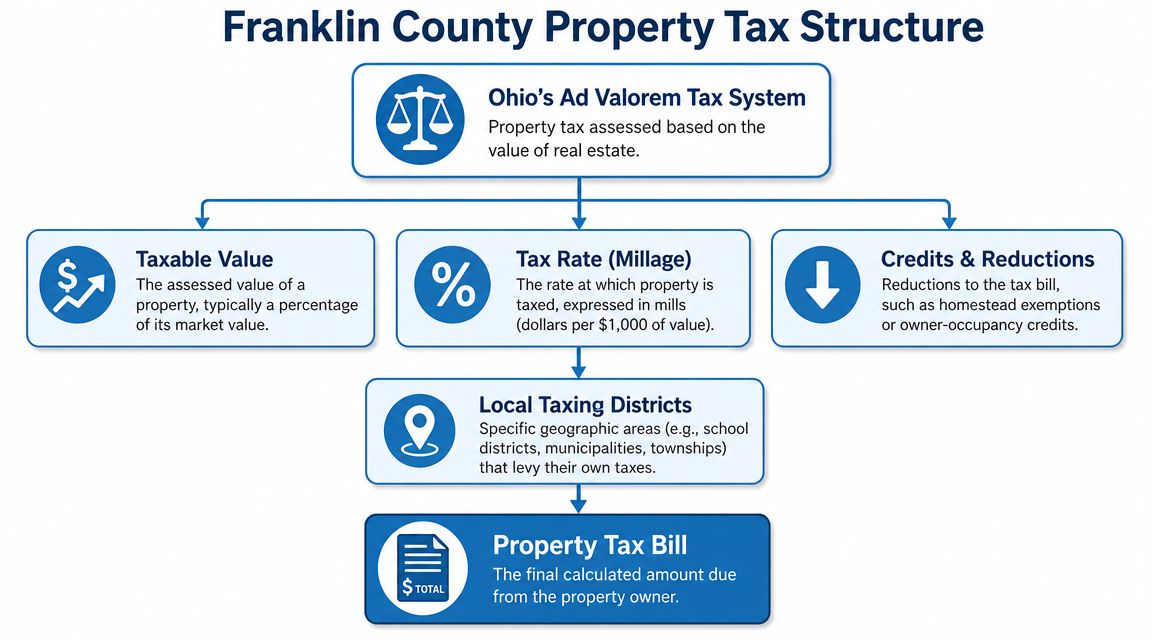

How Are Franklin County Property Taxes Structured

A small district boundary can change the tax outcome on an otherwise similar parcel. That is why Franklin County property tax analysis starts with structure, not with a county-wide rate.

Franklin County real property taxes follow Ohio's ad valorem framework. The bill is tied to the auditor's value and the levies attached to the parcel's taxing district. For underwriting, that means location has to be read at the district level, not just the county or mailing-city level.

The structure professionals use

Three parts control the system:

- Appraised value is the value assigned by the county auditor.

- Taxing district is the parcel's jurisdictional assignment, which determines the levy mix.

- Final tax bill reflects that district levy structure plus any reductions or credits that apply to the owner or property.

That structure matters because the county does not impose one flat real estate tax rate across all parcels. School districts, municipalities or townships, and special districts all affect the final burden. Two sites in the same submarket can pencil differently if one falls into a different district stack.

Where analysts make mistakes

The common error is using a county summary figure as if it were a billing rate. That shortcut can survive a rough market screen, but it does not hold up in acquisition models, tax comps, or parcel-level product design.

A Franklin County tax bill is built from layers such as:

- School district levies

- Municipal or township levies

- Library and other special district levies

- Credits or reductions that affect the amount payable

I treat district assignment as a control field, not as descriptive metadata. If the parcel-to-district match is wrong, the tax estimate is wrong, and the valuation error usually shows up late, after the team has already anchored on a projected NOI.

That same logic matters in escrow analysis. For teams demystifying escrow for loan originators, a weak tax estimate does not just distort underwriting. It can also distort payment setup and reserve assumptions.

Practical implications for valuation and tooling

For investors, the workflow is straightforward.

- Pull the parcel's auditor value.

- Confirm the exact taxing district tied to that parcel.

- Review the levy stack for that district.

- Apply owner-specific reductions only after the base district burden is clear.

For software teams, district identifiers should be stored as queryable tax attributes with version control and audit traceability. ZIP code, city name, and neighborhood label are not reliable substitutes. Franklin County taxes are assigned through official parcel geography, and the structure only becomes usable once the parcel is matched to the correct district.

How Do You Calculate a Property Tax Bill

You calculate a Franklin County property tax bill by starting with the parcel's auditor value, applying the taxing district's rate structure, and then accounting for any reductions that apply to that owner or property.

Without the parcel record and district assignment, any result is just an estimate. That's the part new investors usually underestimate.

A practical calculation workflow

Use this sequence every time:

Confirm the parcel record

Pull the address-matched parcel and make sure the site and mailing details align with the asset you're underwriting.Read the auditor's value

Use the current appraised value listed for that parcel.Identify the taxing district

This is the control variable. If you skip it, the rest of the math is noise.Pull the district levy detail

The total tax burden comes from the district's applicable levies, not from a generic county assumption.Apply credits and reductions last

Owner-occupancy status and other reductions affect the final payable amount, not the location-based structure of the bill itself.

Sample tax calculation

Because a parcel-specific levy schedule and reduction detail can vary, the right way to document the process is as a workflow table rather than a fabricated universal example.

| Step | Description | Example Value |

|---|---|---|

| Parcel identification | Match the subject property to the correct auditor parcel | Specific parcel for a home in Columbus City Schools |

| Appraised value | Use the auditor's listed appraised value | Auditor-listed value for that parcel |

| Taxing district | Confirm the parcel's district assignment | Columbus City Schools district |

| Levy review | Pull the district levy detail attached to that parcel | District-specific levy stack |

| Final bill adjustment | Apply any listed reductions or credits that actually apply | Owner-specific reductions if eligible |

What usually goes wrong

The most common errors are operational, not mathematical.

- Wrong parcel match: Condo units, split lots, and new construction are easy to mis-key.

- Wrong district assumption: A Columbus mailing address doesn't guarantee the same tax treatment as another Columbus mailing address.

- Wrong escrow estimate: Loan teams often need a working payment number before a full audit is complete. That's where tax estimates can drift into monthly payment issues.

For lenders and originators, escrow communication becomes part of the risk-management process. If your borrower doesn't understand how taxes feed the monthly payment, a plain-language explainer like demystifying escrow for loan originators can help align expectations before closing.

Underwriting note: Treat tax estimates as provisional until you've verified the district and current parcel record.

What works is disciplined record matching. What doesn't work is copying last year's seller disclosure, a listing-site estimate, or a neighboring parcel's bill and calling it close enough.

Which Taxing Districts Drive Your Final Rate

Two parcels on the same street can carry materially different tax bills in Franklin County because the rate is built from the parcel's taxing district, not from a single county number.

That point matters more than the county headline rate for underwriting, acquisition models, and any product that estimates carrying costs. A countywide figure is a rough reference. It is not a pricing tool.

Why a county-level rate leads to bad estimates

Franklin County property taxes are assigned through taxing districts that combine local jurisdictions and levy layers. For practical analysis, the county name tells you almost nothing about the final bill without the district assignment.

I see four recurring failure points in tax modeling:

ZIP code matching

ZIPs are mail routes. They are not tax boundaries.City-name assumptions

A Columbus mailing address can still sit in a different school or township tax setup than a nearby Columbus address.School-district shortcuts

School district attachment often changes the result more than investors expect, especially when nearby comps cross a district line.Loose spatial joins

District edge errors show up fast in bulk analysis, especially on redevelopment sites, splits, and newly created parcels.

Teams building maps or automated tax estimators should review parcel boundaries against district layers, not just neighborhood or ZIP overlays. For that workflow, county maps and ZIP code reference methods are useful as a supporting check.

The local layers that usually move the bill

The final rate usually reflects a stack of local authorities, and the mix varies by parcel.

School district levies

This is often the biggest driver of differences between otherwise similar properties.Municipality or township location

Two comparable assets can sit in different local tax environments based on jurisdictional linework alone.Special districts and voter-approved levies

Library, fire, park, and other local-purpose levies can change the effective burden enough to matter in valuation.

For investors, the trade-off is simple. County-level assumptions are fast, but they are noisy. Parcel-level district matching takes more effort, yet it produces numbers you can use for bid discipline, escrow planning, and yield projections.

Here's a quick explainer that helps visualize why boundary-level tax differences matter in practice:

The parcel is taxed by its district assignment, levy stack, and jurisdictional overlays. The county label alone is too broad for due diligence.

What professionals check before trusting the rate

A usable tax number starts with parcel-specific verification:

- Confirm the current taxing district

- Check whether the parcel was split, replatted, or newly improved

- Review the levy stack attached to that district

- Test neighboring comps for district mismatch before using them in analysis

That is the difference between a quick screen and a defensible tax estimate.

How Can You Manage or Reduce Your Tax Liability

You manage Franklin County property-tax liability by verifying the assessment, checking whether any credits or exemptions apply, and appealing value when the record doesn't reflect market reality.

Not every owner has the same tools. A homeowner, a landlord, and a developer won't approach the bill the same way. But the process discipline is the same. Start with the record, not the complaint.

A practical checklist

Assessment review first

Compare the auditor record to the actual property. If the site characteristics or classification look wrong, fix that foundation before you argue about value.Owner-specific relief second

Some reductions depend on occupancy or owner status. Those don't change the district structure, but they can change the amount due.Appeal only with evidence

A strong challenge is evidence-driven. A weak one is just frustration in document form.

For readers who want a broader primer on how assessments work before they evaluate a bill, this overview of property tax assessment is a useful baseline.

What tends to work

A solid challenge usually rests on concrete support such as:

- A recent sale that reflects market value

- Physical-condition issues that affect value

- Record discrepancies between the parcel file and the actual property

- Comparable evidence used carefully and consistently

What doesn't work is arguing from affordability. Tax bills can feel high without being incorrectly assessed.

Decision test: If you can't point to a factual problem in value or record data, you probably don't have an appeal argument yet.

Deadlines and payment discipline

Owners also need a process for timing. Appeals, credits, and payment windows all run on administrative calendars. Missing a filing window is often more expensive than losing an argument on the merits.

The same goes for routine payment planning:

- Watch the county billing schedule

- Coordinate lender escrow if applicable

- Recheck the bill after ownership or occupancy changes

- Track changes after new levies or district updates

For investors, the operational takeaway is simple. Don't wait for a surprise bill to start reviewing tax exposure. Make tax review part of acquisition, refinance, and annual portfolio monitoring.

Where Can You Find Parcel-Level Tax Data

The best source for Franklin County parcel tax data is the county auditor's property search, but it works best for one-off research, not high-volume analysis.

That distinction matters. If you're checking one address before making an offer, the official county tool is usually the first place to go. If you're monitoring a portfolio, building an API product, or evaluating a market at scale, manual lookup becomes the bottleneck.

The manual route

The Franklin County Auditor's parcel search gives you the essentials tied to a specific property record:

- Parcel identification

- Appraised value

- Taxing district information

- Detailed record fields useful for validation

This is the right method when accuracy on a single property matters more than speed.

Manual versus automated workflows

| Method | Best use case | Main limitation |

|---|---|---|

| County auditor parcel search | Single-property due diligence | Slow for repeated or portfolio-wide work |

| Spreadsheet-based manual compilation | Small batches and ad hoc review | Error-prone joins and weak update discipline |

| API or bulk property data workflow | Portfolio monitoring and product development | Requires data integration and schema planning |

If you're evaluating automated tax pipelines, this guide to real-time tax data for real estate investors is a practical reference for thinking through update cadence and operational use.

What changes at scale

At volume, the problem isn't finding one tax record. It's maintaining a reliable stream of parcel-linked tax, assessment, and ownership data without breaking your models every time a record changes.

That's where professionals shift from browsing public portals to structured data delivery. The public system is authoritative for lookup. It isn't designed to be your production-grade monitoring layer.

If you need Franklin County tax, assessment, and parcel data in a format your team can use, BatchData is built for that workflow. It helps investors, lenders, and proptech teams move from manual parcel searches to scalable tax and property-data pipelines for underwriting, monitoring, and due diligence.