Foreclosure filings in the US are rising, with 187,659 properties entering the pipeline in the first half of 2025, signaling a market recalibrating from post-pandemic artificial lows. This uptick, driven by persistent inflation and higher interest rates, represents a controlled return to pre-COVID norms rather than a 2008-style crisis. The core insight lies in the simultaneous increase of both new foreclosure starts and completed bank repossessions, indicating more homeowners are entering distress and lenders are completing the process.

Core Takeaways:

- National Rate: One in every 758 homes faced a foreclosure filing in the first half of 2025.

- Key Driver: A combination of inflation, high interest rates, and the expiration of pandemic-era forbearance programs.

- Stabilizing Factor: Over $30 trillion in homeowner equity provides a massive buffer, allowing many to sell rather than face foreclosure.

- Hotspots: States like Delaware, Nevada, and Florida show the highest foreclosure rates, while major metros like Chicago and New York lead in volume.

This guide breaks down the current foreclosure statistics, compares them to historical benchmarks, and explains how to translate this data into actionable intelligence.

What Is The Current State Of Foreclosures In The US?

The US foreclosure market is normalizing after the unprecedented lows during the COVID-19 pandemic, with activity steadily increasing as homeowner protections have expired. The national foreclosure rate for the first half of 2025 was 0.13%, or one in every 758 housing units. This is the new baseline reflecting current economic pressures.

The consistency of the increase is the key indicator of market health. July 2025 saw 36,128 properties with foreclosure filings, an 11% jump from June and a 13% increase from July 2024. This trend demonstrates that economic headwinds like inflation and elevated interest rates are having a material impact on homeowner stability.

A Breakdown Of The Foreclosure Pipeline

Understanding the different stages of the foreclosure process provides critical insight into where pressure is building in the market.

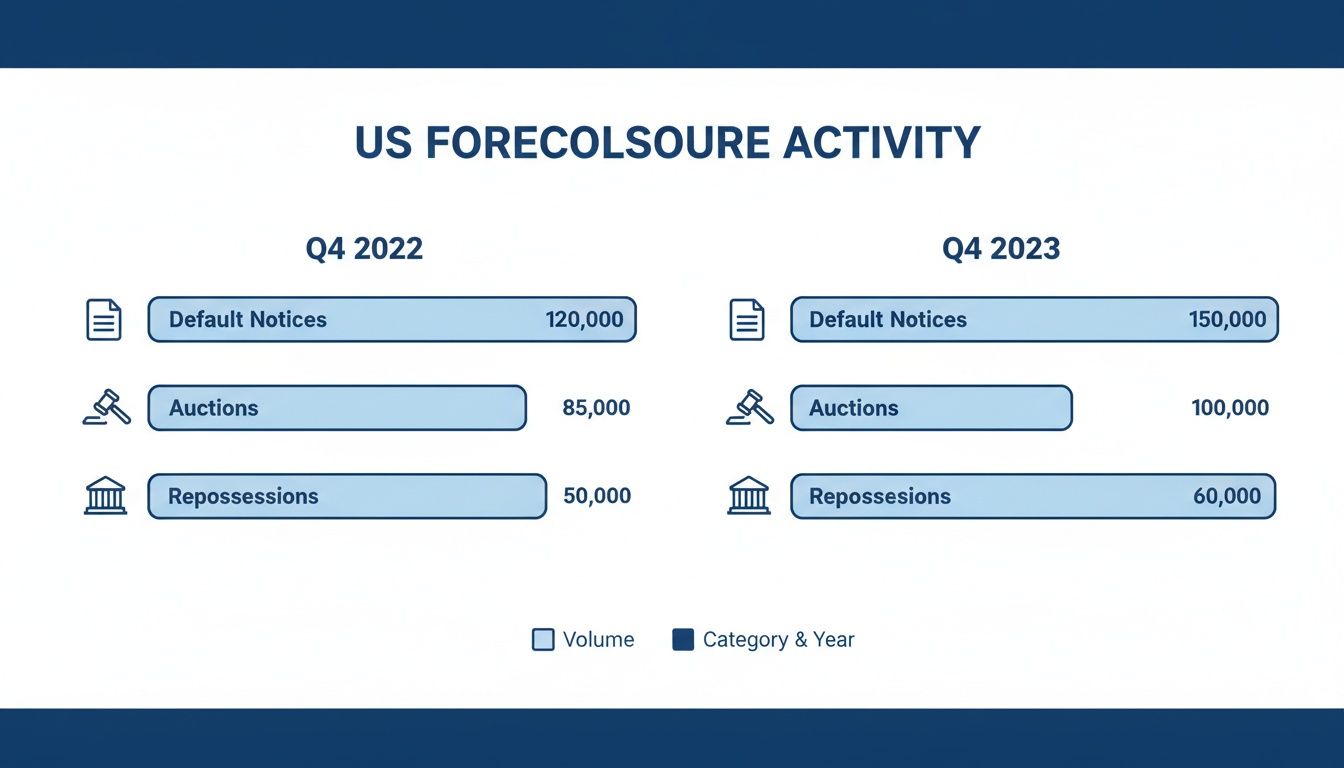

- Foreclosure Starts (Pre-Foreclosure): This is the leading indicator of distress, logged when a lender files the initial notice of default. In the first half of 2025, there were 140,006 foreclosure starts, a 7% increase from the first half of 2024. This signals more properties are entering the distress pipeline. For granular data, see the Active Pre-Foreclosures Report.

- Bank Repossessions (REO): This is the final stage where a lender reclaims a property that fails to sell at auction. Lenders completed 21,007 repossessions in the first half of 2025, up 12% year-over-year. This shows more properties are moving completely through the foreclosure process.

The simultaneous rise in both foreclosure starts and completions is the critical takeaway. It confirms that not only are more homeowners falling behind, but lenders are also processing these defaults through to completion.

Current US Foreclosure Snapshot

This table provides a high-level overview of the most recent national foreclosure metrics.

| Metric | Recent Figure | Year-Over-Year Change |

|---|---|---|

| Total Foreclosure Filings | 187,659 Properties (H1 2025) | +5.8% |

| National Foreclosure Rate | 1 in every 758 units | Increased Distress |

| Foreclosure Starts | 140,006 Properties (H1 2025) | +7.0% |

| Bank Repossessions (REO) | 21,007 Properties (H1 2025) | +12.0% |

The data shows a market in transition, not crisis. For investors and lenders, these statistics are direct signals of emerging risk and potential opportunity.

Which States And Cities Have The Highest Foreclosure Rates?

Foreclosure activity is concentrated in specific geographic hotspots where local economic pressures, such as high property taxes or unstable job markets, disproportionately affect homeowners. Identifying these areas is critical for risk assessment and investment strategy.

In January 2026, US foreclosure filings reached 40,534 properties, a 32% year-over-year increase and the 11th consecutive month of rising activity. Delaware leads the nation with the highest foreclosure rate (one filing for every 1,612 housing units), followed by Nevada (1 in 1,983) and Florida (1 in 2,067). However, by raw volume, Florida had the most foreclosure starts (3,523), followed by Texas (3,116) and California (2,790). To analyze the complete data, explore the full foreclosure market report on attomdata.com.

The growth in both initial defaults and final bank repossessions confirms that lenders are increasingly seeing the foreclosure process through to completion.

Rate vs. Volume

Analyzing geographic foreclosure data requires differentiating between the foreclosure rate and the total volume of filings.

| Metric | Definition | What It Tells You | Best For |

|---|---|---|---|

| Foreclosure Rate | The concentration of filings (e.g., "1 in every X homes"). | The intensity of distress in a specific market. | Identifying targeted acquisition opportunities. |

| Foreclosure Volume | The raw count of total foreclosure filings. | The scale of the problem and market size. | Gauging the breadth of the distressed property pipeline. |

For an investor, a high rate suggests a market ripe for targeted acquisitions, while high volume indicates a broader, more sustained pipeline of distressed properties.

State-Level Hotspots

This table contrasts the states with the highest foreclosure rates against their raw volume of new filings, clarifying where distress is most concentrated.

| State | Foreclosure Rate (1 per X units) | Total Foreclosure Starts |

|---|---|---|

| Delaware | 1 in every 1,612 | Moderate Volume |

| Nevada | 1 in every 1,983 | Moderate Volume |

| Florida | 1 in every 2,067 | 3,523 (Highest Volume) |

| South Carolina | 1 in every 2,351 | Moderate Volume |

| Maryland | 1 in every 2,430 | Moderate Volume |

Florida's data highlights the importance of analyzing both metrics; while its rate is third-highest, its sheer volume of new foreclosures is the largest in the nation.

Metropolitan Areas Feeling The Pressure

Foreclosure trends become more granular at the city level, with major metropolitan statistical areas (MSAs) often showing the highest activity. In the first quarter of 2025, the urban centers with the highest number of new foreclosure filings were:

- Chicago, IL (3,789 starts)

- New York, NY (3,566 starts)

- Houston, TX (3,046 starts)

High housing costs, shifting local job markets, and significant property tax burdens create a perfect storm for distress in these economic hubs. Pinpointing these opportunities requires specific tools, such as using county maps and zip codes to refine your property search.

How Do Current Foreclosure Statistics Compare to Historical Trends?

Today’s foreclosure numbers must be viewed through the lens of two historical extremes: the 2008 subprime mortgage crisis and the artificially suppressed market during the COVID-19 pandemic. This context is essential to determine whether current trends represent a healthy correction or the start of a downturn.

The contrast is stark. The US foreclosure rate peaked at 2.23% in 2010, with over 2.8 million properties receiving filings. In 2021, government forbearance programs pushed the rate to a record low of 0.11%. By 2022, it began normalizing to 0.23%—still 90% below the 2010 peak, cushioned by a record $30 trillion in homeowner equity by 2024. For more historical data, review the foreclosure rate data on Statista.com.

The Great Financial Crisis: A Benchmark for Systemic Failure

The 2008-2010 period serves as the ultimate stress test, driven by systemic failures rather than individual economic hardship.

- Lax Lending Standards: Subprime loans and adjustable-rate mortgages (ARMs) were issued with minimal verification, creating a foundation of unsustainable debt.

- Housing Bubble Collapse: Plunging property values left millions of homeowners "underwater," owing more than their homes were worth and eliminating any incentive to continue paying.

- Economic Recession: Mass layoffs resulting from the housing collapse meant even responsible borrowers could no longer make payments.

This combination caused a foreclosure tsunami. Today's market is structurally different, with stricter lending regulations like the Qualified Mortgage (QM) rule preventing a repeat of such systemic risk.

The Pandemic Anomaly: An Artificial Low

The years 2020-2021 represent the opposite extreme, where foreclosure rates hit all-time lows due to direct government intervention.

- The CARES Act: This legislation enacted a nationwide foreclosure moratorium and granted homeowners the right to enter forbearance, pausing mortgage payments without penalty.

- Economic Stimulus: Multiple rounds of stimulus payments and enhanced unemployment benefits provided a temporary financial safety net.

These measures successfully prevented a foreclosure wave but created an artificial dam. The current uptick is the predictable and necessary market normalization as those protections have expired. To understand these cycles better, see our guide on how to analyze historical property trends.

What Key Factors Are Driving Current Foreclosure Trends?

The current increase in foreclosure activity is driven by a conflict between significant economic pressures and strong stabilizing forces, resulting in a market recalibration, not a collapse. The primary drivers pushing homeowners toward distress are persistent inflation and high mortgage rates, which have removed the safety net of refinancing. This trend began as pandemic-era forbearance programs expired.

However, a solid labor market and an unprecedented $30 trillion in homeowner equity are acting as powerful buffers, preventing a widespread crisis.

Inflation and Interest Rates

Sustained inflation erodes household budgets by increasing the cost of essentials, leaving less disposable income for mortgage payments. Simultaneously, the Federal Reserve's interest rate hikes to combat inflation have eliminated refinancing as a viable option for struggling homeowners.

This affordability squeeze explains the rebound in US foreclosure statistics. After COVID protections ended in 2022, foreclosure filings surged 115% year-over-year. By Q2 2025, New Jersey had the highest foreclosure rate (one filing per 800 housing units), demonstrating how affordability issues—with typical mortgage payments up 50% since 2020—create intense, localized distress.

Stabilizing Forces Preventing a Collapse

Despite these headwinds, two factors are preventing a market crisis.

| Stabilizing Factor | Description | Impact |

|---|---|---|

| Massive Homeowner Equity | The housing boom created an unprecedented wealth cushion. | Allows struggling owners to sell, often at a profit, to avoid foreclosure. |

| Strong Labor Market | Unemployment remains low, allowing most to find new work quickly after a setback. | Enables homeowners to recover from temporary financial shocks and resume payments. |

This balance is why the market is experiencing concentrated pockets of distress rather than a systemic, nationwide meltdown. Analysis of broader economic signals, such as understanding market health through absorption rate, provides a deeper view of the supply and demand dynamics influencing this risk.

How Can Foreclosure Data Be Used For Business?

Raw foreclosure statistics are noise; actionable intelligence is the signal. For businesses, the goal is to convert this data into a competitive advantage by linking granular details—like pre-foreclosure filings and property lien information—to specific outcomes, such as acquiring assets or managing portfolio risk.

This process involves moving beyond national rates to use specific data points for faster, smarter decisions.

Real Estate Investors

For investors, foreclosure data is a direct pipeline to motivated sellers and off-market properties. Acting on the earliest indicators of distress is key.

- Pre-Foreclosure Leads: The initial Notice of Default (NOD) or Lis Pendens filing is the first signal. Monitoring these filings allows investors to contact homeowners early, often offering a cash sale that avoids a damaging foreclosure on their credit report.

- Lien Stacking Analysis: A property with multiple liens (e.g., tax, mechanic's) on top of a mortgage default indicates severe financial distress. This data helps pinpoint highly motivated sellers and calculate accurate acquisition costs.

- Auction Intelligence: Tracking properties scheduled for auction enables thorough due diligence in advance. Researching title history and property condition allows investors to bid with confidence and avoid properties with clouded titles.

The strategy is to shift from reactive to proactive, intercepting opportunities at the pre-foreclosure stage where competition is lower and negotiation power is higher.

Lenders

For mortgage servicers, foreclosure data is a tool for proactive risk management and loss mitigation, not just tracking losses.

By analyzing geographic foreclosure hotspots, lenders can identify where their loan portfolios are most exposed. A spike in foreclosure starts in a specific county allows them to flag those assets for closer monitoring and allocate resources effectively. This data also fuels predictive models that identify at-risk homeowners before they default, enabling servicers to offer loss mitigation options like loan modifications or forbearance, which protects both the borrower and the lender's balance sheet.

Proptech Companies

For proptech platforms, foreclosure data is the raw material for building innovative tools. Integrating this data via an API from a provider like BatchData enables the creation of powerful platforms for investors, lenders, and consumers.

- Powering Predictive Models: Historical and real-time foreclosure data trains machine learning algorithms to predict which properties are likely to enter distress, improving underwriting and risk assessment.

- Enhancing Lead Generation: Pre-foreclosure filings generate high-intent leads for real estate agents and investors who can serve prospects with an urgent need.

- Automating Due Diligence: Integrating foreclosure, lien, and property ownership data into a single platform streamlines the due diligence process from days to seconds.

Ultimately, actionable intelligence means treating foreclosure data as a predictive tool to drive growth and minimize risk.

What Are The Most Common Questions About US Foreclosure Data?

Navigating foreclosure statistics can be complex. Here are direct answers to the most frequently asked questions from investors, lenders, and homeowners.

How is the national foreclosure rate calculated?

The national foreclosure rate is calculated by dividing the total number of properties with a foreclosure filing by the total number of housing units in the country. A "foreclosure filing" includes any of three stages: a Notice of Default (NOD), a Notice of Foreclosure Sale (NFS), or a Real Estate Owned (REO) property. The resulting percentage is often expressed as a more tangible ratio, such as "one in every 4,000 homes."

What is the difference between judicial and non-judicial foreclosure?

The core difference is the requirement of court involvement, which is determined by state law and significantly impacts the foreclosure timeline and cost.

| Foreclosure Type | Process | Common States | Timeline |

|---|---|---|---|

| Judicial | Lender must file a lawsuit and get a court order to foreclose. | Illinois, Florida, New York | Slower, often taking years. |

| Non-Judicial | No court action is needed; lender follows state-mandated notification steps. | Texas, California, Arizona | Faster, often completed in a few months. |

This distinction is the single largest factor in foreclosure timelines. Non-judicial states like Texas average around 135 days, whereas judicial states like Louisiana can average over 3,600 days.

Why do some states consistently have higher foreclosure rates?

Persistently high foreclosure rates in certain states are typically caused by a combination of economic, legal, and environmental factors. For a deeper understanding of this, it is useful to know how long the foreclosure process takes, as this is a direct result of state-specific issues.

| Factor | Description | Impact on Foreclosure Rates |

|---|---|---|

| Judicial vs. Non-Judicial | States requiring court involvement (judicial) experience longer timelines, creating a backlog that inflates the active foreclosure count. | Increases the number of reported filings over a longer period. |

| Economic Dependence | States reliant on volatile industries like tourism or energy see more defaults during sector downturns. | Creates local boom-and-bust cycles for homeowners. |

| Property Taxes & Insurance | High property taxes and soaring insurance premiums, especially in disaster-prone areas, increase the total cost of ownership. | Squeezes household budgets, leaving less for the mortgage. |

| Housing Affordability | Markets where home prices outpaced wages leave homeowners over-leveraged with little financial cushion. | Reduces a homeowner's ability to absorb a financial shock. |

Does a high foreclosure rate mean a housing crash is coming?

Not necessarily. A rising foreclosure rate signals homeowner stress, but it does not automatically predict a 2008-style housing crash. Today's market has critical buffers that did not exist then, most notably over $30 trillion in homeowner equity. This equity acts as a safety net, allowing most struggling homeowners to sell their property, pay off their mortgage, and avoid foreclosure altogether. Tighter lending standards also prevent the systemic risk that fueled the subprime crisis. A rising rate today is more likely to signal a market normalization or regional distress, not a widespread collapse.

Ready to transform raw foreclosure statistics into your next opportunity? BatchData provides the comprehensive property data, pre-foreclosure filings, and verified owner contacts you need to identify distressed assets before anyone else. Access our industry-leading data via API or bulk delivery to power your acquisitions, risk models, and lead generation at scale. Start making faster, data-driven decisions by visiting https://batchdata.io.