Real estate equity is the single most powerful wealth-building tool available to the average person. It is the portion of your property you actually own—the current market value minus any outstanding mortgage debt.

This is not an abstract number; it is your home's net worth and the cash you would receive after selling the property and paying off all loans. As you reduce your mortgage principal and the market appreciates, your equity grows, turning a monthly housing payment into a significant financial asset. For real estate investors, equity is the primary vehicle for leveraging one property to acquire the next.

| Key Takeaway | Description |

|---|---|

| Definition | Your home's market value minus the total debt you owe on it. |

| How It Grows | Through mortgage principal payments and property market appreciation. |

| Why It Matters | It acts as a forced savings account and a leverageable financial tool. |

This guide breaks down exactly how equity works, how to calculate it, and how to use it as a strategic financial tool.

What is equity in real estate and why is it important?

Equity is the monetary value of your ownership stake in a property. It represents the portion of your home that is completely debt-free. As you pay down your mortgage and property values appreciate, that ownership stake increases, creating a tangible financial resource.

In the United States, where BatchData provides data on over 155 million properties, homeowner tappable equity—the amount available to borrow while maintaining a 20% equity cushion—recently hit $11 trillion, according to Federal Reserve data. This massive pool of capital underscores equity's role as a cornerstone of personal wealth. For a detailed analysis of market trends, see the global real estate market outlook.

At its core, real estate equity acts as a forced savings account that grows with each mortgage payment and appreciates with the market, turning a monthly housing expense into a powerful asset.

Understanding this mechanism is the first step toward using your home not just as a place to live, but as a financial instrument for building serious wealth.

Core Components of Equity

Equity is determined by two primary components: what your property is worth and what you owe on it.

- Current Market Value (CMV): The price your property would realistically sell for in the current market. This value is influenced by location, condition, recent comparable sales (comps), and broad economic trends. It is typically determined by a professional appraisal or an Automated Valuation Model (AVM).

- Outstanding Debt: The total amount you owe on the property. This includes the primary mortgage balance plus any secondary loans such as a home equity loan or a Home Equity Line of Credit (HELOC).

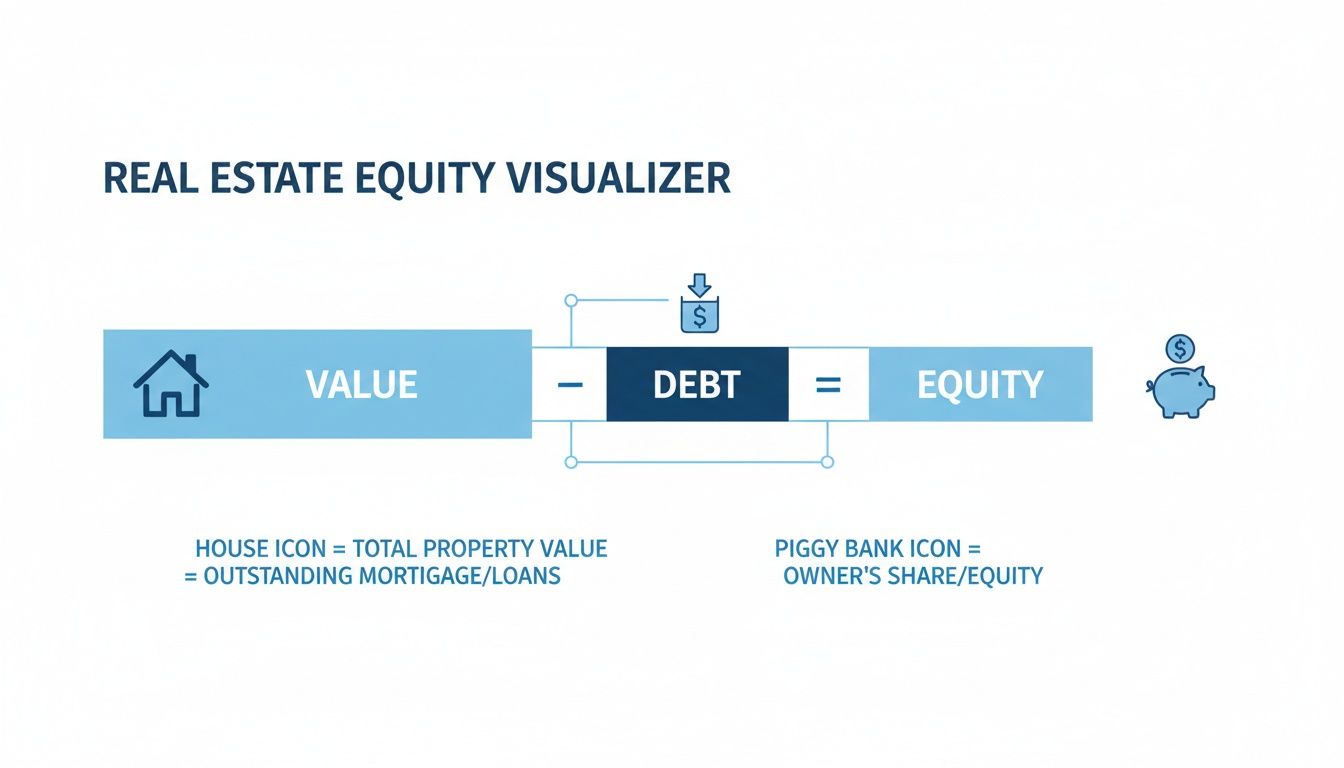

Your financial stake—your equity—is the simple result of subtracting your total debt from the current market value.

Real Estate Equity at a Glance

| Component | Definition | Example |

|---|---|---|

| Market Value | The price a property would sell for today. | Your home is appraised at $500,000. |

| Mortgage Balance | The total amount you still owe to your lender. | You have $300,000 left on your mortgage. |

| Your Equity | The difference between the two values. | Your equity is $200,000 ($500k – $300k). |

Monitoring your equity provides a real-time report card on your investment's performance and is the foundation for unlocking your home's financial potential.

How do you calculate real estate equity?

You calculate real estate equity using a simple formula: Current Market Value – Outstanding Debt = Your Equity. This calculation reveals your precise financial position in a property.

To demonstrate how this works in practice, we'll walk through three distinct scenarios. These examples show how equity changes at various stages of ownership due to both market appreciation and principal reduction.

As the infographic illustrates, equity is the value remaining after all debts against the property are settled. It is your true slice of the asset.

Three Real-World Equity Calculation Examples

The New Homeowner (Year 1): An individual buys a home for $400,000 with a 5% down payment ($20,000), financing the remaining $390,000. After one year, they have paid down $5,000 in principal, and the market value remains unchanged.

- Market Value: $400,000

- Outstanding Debt: $385,000 ($390,000 – $5,000)

- Calculated Equity: $15,000

The Mid-Term Owner (Year 10): A homeowner purchased their house for $350,000 ten years ago. Consistent payments have reduced their mortgage to $250,000. A strong local market has increased the property's value to $550,000.

- Market Value: $550,000

- Outstanding Debt: $250,000

- Calculated Equity: $300,000

The Long-Term Owner (Year 25): An owner is near the end of a 30-year mortgage on a house bought for $200,000. The remaining loan balance is only $40,000. Decades of market growth have pushed the home's value to $700,000.

- Market Value: $700,000

- Outstanding Debt: $40,000

- Calculated Equity: $660,000

These examples show that equity is a dynamic figure, influenced by both your actions (paying the mortgage) and external market forces. For an instant valuation, a modern property value calculator can provide immediate insight.

The Loan-to-Value Ratio (LTV)

Lenders view the equity relationship from the opposite perspective, using a metric called the Loan-to-Value (LTV) ratio to assess their risk.

The LTV ratio is the percentage of a property's appraised value that is financed by a loan. It is the inverse of your equity percentage. The formula is: (Mortgage Amount / Appraised Property Value) x 100 = LTV Ratio.

Lenders rely on the LTV ratio to make underwriting decisions. A lower LTV signifies that the borrower has more "skin in the game," which reduces the lender's risk and typically results in more favorable loan terms.

Let’s calculate the LTV for our three homeowner scenarios:

| Owner Scenario | Mortgage Amount | Property Value | LTV Calculation | LTV Ratio | Equity Stake |

|---|---|---|---|---|---|

| The New Homeowner | $385,000 | $400,000 | ($385k / $400k) x 100 | 96.25% | 3.75% |

| The Mid-Term Owner | $250,000 | $550,000 | ($250k / $550k) x 100 | 45.45% | 54.55% |

| The Long-Term Owner | $40,000 | $700,000 | ($40k / $700k) x 100 | 5.71% | 94.29% |

Lenders typically require an LTV of 80% or lower for conventional loans to avoid Private Mortgage Insurance (PMI). When accessing equity via a HELOC or cash-out refinance, lenders often limit the combined LTV (original mortgage plus new loan) to 85% to protect against market downturns.

What are the primary drivers of equity growth?

Equity growth is driven by three primary forces: principal paydown, market appreciation, and forced appreciation. Understanding these mechanisms allows an owner to shift from passively holding a home to actively managing a wealth-building asset.

Some of these drivers work automatically, while others require direct action. A strategic owner or investor leverages all three to maximize their financial position.

Principal Paydown

This is the most reliable method for building equity. Each mortgage payment is divided between interest (the cost of borrowing) and principal (the portion that reduces your loan balance).

During the initial years of a mortgage, the majority of the payment covers interest. However, through a process called amortization, an increasing portion of each subsequent payment is applied to the principal, accelerating equity growth over time. It is the slow-but-guaranteed method of wealth accumulation.

Paying down your principal is a forced savings plan. It converts a portion of your housing expense into tangible wealth, one payment at a time, guaranteed.

Market Appreciation

This is the passive increase in a property's value due to external economic factors, not from any improvements made by the owner. It is driven by supply and demand.

Key factors include:

- Economic Growth: Areas with strong job growth and infrastructure investment typically see faster appreciation.

- Supply Constraints: When new construction fails to meet population growth, existing home values are driven upward. For example, U.S. multi-housing starts recently fell by over 75% from their peak, tightening supply.

- Inflation & Interest Rates: Macroeconomic trends directly impact property values. You can learn how interest rates and property valuation are connected in our guide.

The impact of appreciation on wealth is significant. U.S. homeowners' tappable equity recently hit record highs, unlocking an estimated $1.2 trillion in potential home equity lines of credit as prices stabilized.

Forced Appreciation

This is the active process of increasing a property's value through strategic physical improvements. The goal is to make targeted investments where the value added exceeds the cost of the renovation.

| Strategy | Description | Real-World Example |

|---|---|---|

| Renovations & Remodels | Upgrading key areas to meet modern buyer expectations. | A $25,000 kitchen remodel increases the home's value by $40,000. |

| Adding Square Footage | Physically expanding the property's usable living space. | Converting an unfinished basement into a legal bedroom and bathroom suite. |

| Curb Appeal | Improving the exterior to create a strong first impression. | Professional landscaping, a new front door, and updated exterior paint. |

Exploring effective strategies to increase property value helps you maximize this powerful tool. Combining steady principal paydown with market and forced appreciation creates a robust engine for building substantial real estate equity.

How can you use your real estate equity?

You can use real estate equity by borrowing against it with a loan or line of credit, or by realizing it as cash through the sale of the property. Your equity is not merely a number; it is a financial tool that can be deployed for renovations, debt consolidation, or new investments.

Each method of accessing this value involves specific costs, risks, and use cases. Matching the right financial product to your goal is critical to avoid taking on unnecessary risk.

Accessing Equity Without Selling

Several financial products allow you to borrow against your equity while retaining ownership of the property. The three most common methods are Home Equity Lines of Credit (HELOCs), home equity loans, and cash-out refinances.

- A Home Equity Line of Credit (HELOC) functions like a credit card secured by your home. You receive a maximum credit limit and can draw funds as needed during a 5-10 year "draw period," paying interest only on the amount used. Its flexibility is ideal for ongoing projects with variable costs, such as a major renovation.

- A home equity loan provides a single lump sum of cash upfront. You repay it with fixed monthly installments over a set term, typically 5 to 15 years. The predictable payments and fixed interest rate make it suitable for large, one-time expenses like debt consolidation or tuition.

- A cash-out refinance replaces your existing mortgage with a new, larger one. You receive the difference between the new loan amount and your old mortgage balance in cash. This is most effective when interest rates have fallen, allowing you to access cash while potentially securing a lower rate on your entire mortgage.

Comparing Equity Access Methods

| Feature | HELOC | Home Equity Loan | Cash-Out Refinance |

|---|---|---|---|

| Funds Distribution | Revolving line of credit; draw as needed. | Single lump-sum payment. | Single lump-sum payment. |

| Interest Rate | Typically variable; tied to a prime rate. | Fixed rate. | Fixed or variable rate. |

| Repayment Structure | Interest-only payments during draw period. | Fixed principal and interest payments. | Replaces original mortgage with a new one. |

| Best For | Ongoing projects, emergency funds. | Large, one-time expenses. | Lowering mortgage rate while accessing cash. |

Selling Your Property

The most direct method to access 100% of your equity is to sell the property. Upon sale, the proceeds are used to pay off the remaining mortgage, other liens, and closing costs. The remaining amount is your realized equity—cash in hand.

Selling is often the final step in an investment cycle but is also the most disruptive. It requires careful market timing and involves significant transaction costs, including real estate agent commissions that typically range from 5% to 6% of the sale price.

The primary risk when using equity is over-leveraging. Borrowing too much against your home can lead to negative equity if property values decline, a situation where you owe more than the home is worth.

How does accurate equity data power real estate decisions?

Accurate equity data provides a competitive edge by enabling lenders, investors, and proptech platforms to identify opportunities and mitigate risk. Generic or outdated information leads to missed deals, while competitors use fresh data from over 155 million properties to target high-intent leads and make data-driven decisions.

This data is especially powerful during market shifts. For instance, following a market correction of 20-25%, savvy investors identify prime buying opportunities. The global real estate market recently demonstrated this resilience, posting positive returns for four consecutive quarters as new construction slowed dramatically. U.S. multi-housing starts are down over 75% from their peaks, and logistics deliveries have dropped 42%, supporting the value and equity of existing properties. For more on this, review the 2025 real estate mid-year outlook from Morgan Stanley.

Uncovering High-Intent Borrowers

For lenders, homeowner equity data is a direct path to the most qualified customers. A homeowner with significant equity is a prime candidate for a HELOC or cash-out refinance.

- Equity Filtering: Lenders can instantly pinpoint homeowners with a loan-to-value (LTV) ratio below 70%, signaling substantial tappable equity.

- Life-Event Triggers: Combining equity data with triggers like construction permits or empty-nester status identifies homeowners with an immediate need for capital.

- Risk Mitigation: Screening for properties with no existing liens ensures the lender maintains a primary lien position, significantly reducing underwriting risk.

Finding Motivated Sellers

For investors, accurate equity and lien data is the map to off-market deals. A property with high equity but a pre-foreclosure notice or tax lien often indicates a distressed owner. They have a valuable asset but need a fast exit—the definition of a motivated seller.

For an investor, knowing a property's equity is like knowing a company's cash on hand. It reveals financial health, potential for negotiation, and the owner's likely next move.

Modern property intelligence platforms provide this data instantly.

A dashboard like this consolidates equity, value estimates, and mortgage data into a complete financial snapshot, allowing an investor to qualify a property in seconds.

Enhancing Proptech Platforms

For real estate portals and proptech companies, user engagement and data accuracy are paramount. Integrating a powerful data API allows these platforms to deliver the reliable Automated Valuation Models (AVMs) and equity estimates that users demand.

This not only improves the user experience but also creates new revenue streams, such as connecting users with lending partners. Success depends on understanding the nuances between data accuracy versus AVM reliability. A strategic use of this equity is to use a 1031 exchange to transition from long-term rentals to short-term rentals when shifting investment strategies.

What are the most frequently asked questions about equity?

What is the difference between equity and profit?

Equity is your ownership stake today, while profit is the cash realized after a sale. Equity is a dynamic value tied to the asset, fluctuating with the market and mortgage payments. Profit is a final calculation: Sale Price – (Original Purchase Price + Total Costs). A property can have high equity but yield a low profit if sold in a down market.

What is negative equity?

Negative equity occurs when you owe more on your mortgage than the property is worth. Often called being "underwater," this is a high-risk position. If forced to sell, you would need to bring cash to closing to cover the shortfall. It also makes refinancing or obtaining a home equity loan nearly impossible. Approximately 2.1% of mortgaged U.S. homes are currently considered seriously underwater.

Negative equity traps a homeowner, freezing their ability to move or refinance and leaving them financially vulnerable until property values rise or they pay down sufficient principal.

How quickly can you build real estate equity?

The speed of equity growth depends on four factors:

- Down Payment: A 20% down payment provides a significant equity cushion from day one versus a 5% down payment.

- Loan Term: A 15-year mortgage builds equity significantly faster than a 30-year loan because a larger portion of each payment reduces principal.

- Market Conditions: A strong market can increase equity by tens of thousands of dollars in a single year through appreciation alone.

- Extra Payments: Making bi-weekly payments or adding extra to the principal each month can shave years off the loan and accelerate equity growth.

Can you have equity in a rental property?

Yes. Equity in a rental property is calculated the same way as in a primary residence: Market Value – Outstanding Debt = Equity. For investors, this equity is often the capital used to acquire additional properties. A common strategy is to use a cash-out refinance on a high-equity rental to fund the down payment for the next purchase, which is the core principle of the BRRRR (Buy, Rehab, Rent, Refinance, Repeat) method.

Does a HELOC affect your home equity?

Yes, a HELOC directly reduces your available home equity. When you open a Home Equity Line of Credit, the lender places a second lien on your property for the full credit line amount. Even if you haven't drawn any funds, this lien impacts the total equity available for other loans or a sale. As you draw from the line of credit, your total debt increases, and your net equity decreases dollar-for-dollar. Repaying the HELOC principal restores your equity over time.

Unlock the full potential of your real estate strategy with BatchData. Access comprehensive data on over 155 million U.S. properties, including precise equity estimates, AVMs, and lien details to identify high-intent leads and make smarter, faster decisions. Visit https://batchdata.io to see how our data can power your growth.