SEO Title: What Is a Title Insurance Policy and How It Works

Meta Description: Learn what a title insurance policy covers, how owner’s and lender’s policies differ, what it costs, and how data is changing underwriting.

Meta Keywords: what is a title insurance policy, owner’s title insurance, lender’s title insurance, title insurance cost, ALTA policy, title underwriting, property data, real estate due diligence

Title defects aren't edge cases. In high-volume property datasets, title and ownership discrepancies show up in up to 25% of preliminary title reports according to the NAIC overview at https://content.naic.org/article/consumer-insight-vitals-title-insurance-what-you-need-know.

If you're buying, lending on, or underwriting real estate, that's the frame to use. A title insurance policy is not just a closing line item. It's a financial backstop against defects buried in the property's past. It protects against problems such as liens, fraud, forgery, recording errors, and unknown heirs that can surface long after closing.

For operators and investors, the more useful question isn't just what is a title insurance policy. It's when the policy is enough, when it isn't, and where modern data can reduce risk before a claim ever exists.

| Core issue | What matters |

|---|---|

| What it is | A one-time insurance product covering title defects that existed before purchase |

| Two policy types | Owner's policy protects buyer equity. Lender's policy protects the mortgage lender |

| Cost reality | Pricing is shoppable, and buyers can often reduce costs by comparing providers |

| Modern shift | Better property data helps teams catch risk earlier, before it turns into a title problem |

A useful market lens comes from BatchData's Investor Pulse report, because title risk doesn't sit in isolation. It shows up alongside lien activity, ownership complexity, and broader acquisition signals.

Your Guide to Title Insurance in 2026

Title insurance is a one-time policy that protects against old title problems, not future property damage or future ownership behavior.

That distinction matters because many buyers still compare it to homeowners insurance. It isn't. A title policy addresses defects already embedded in the chain of title before closing. If the issue predates the deal and is covered, the insurer steps in.

The practical summary is simple:

- Owner's policy: protects the buyer's equity and legal position.

- Lender's policy: protects the lender's loan balance.

- Real value: a large part of the premium funds the title search and exam work done before closing.

- Modern edge: data-rich underwriting can flag messy ownership histories, liens, and risk signals earlier.

Quick facts

| Topic | Practical answer |

|---|---|

| When it's paid | At closing, as a one-time premium |

| What it covers | Covered title defects such as liens, fraud, forgery, clerical errors, and unknown-heir claims |

| How long it lasts | Owner's coverage generally lasts as long as the owner or heirs hold the property |

| Why claims are relatively uncommon | Title companies spend heavily on prevention before the transaction closes |

For a proptech founder, the important takeaway is that title insurance sits at the intersection of legal history and operational data quality. For an investor, it tells you where the hidden downside lives. For a lender, it's table stakes. The industry has relied on this model since the first U.S. policy was issued in 1876, and by 2023 it was writing over $20 billion in annual premiums through a market tied to 5 to 6 million U.S. home sales each year according to First American's overview of title insurance at https://www.firstam.com/home-buying-guide/what-is-title-insurance-and-why-do-i-need-it/.

How Does a Title Insurance Policy Work?

A title insurance policy is a one-time premium insurance product that protects real estate owners and lenders against financial losses from defects in the property's title existing prior to purchase.

That's the clean definition. The operating model is what makes title insurance different from almost every other insurance product.

It insures the past

Casualty insurance assumes future risk. Title insurance examines historical risk. The policy covers issues such as liens, forgeries, fraud, clerical errors, and claims from unknown heirs that already existed but weren't identified or resolved before closing.

Consider it a legal background check on the asset.

A house can look fine physically and still carry a broken ownership history. That's where title work lives. Professionals trace deeds, mortgages, judgments, tax records, releases, and recorded instruments to build a chain of title and identify defects.

The product has two layers

Search and examination

- Title professionals review public records.

- They identify problems that can be cleared before closing.

- This is why a large portion of the fee goes to preventive work, not just claim reserves.

Insurance coverage

- If a covered defect slips through or can't be discovered in time, the policy covers the insured party according to its terms.

- That can include legal defense costs and financial loss up to the policy limits.

Practical rule: The title policy is only part of the value. The title search is the other part, and in many deals it's the part doing the critical work.

Why claims are comparatively rare

Claims are rare for a structural reason. Title companies try to fix the problem before the deed records. If they can clear an unreleased lien, resolve a recording error, or identify a probate issue upfront, there may never be a later claim.

That prevention-heavy model is why title insurance feels expensive to people who compare it to other policies by payout ratio alone. They're looking at the wrong benchmark. Much of the cost is tied to reducing the chance of a future dispute in the first place.

Where this matters in practice

For proptech and institutional buyers, the operational insight is straightforward:

- Messy ownership history slows closings

- Unreleased liens create underwriting friction

- Recording errors create downstream servicing and resale risk

- Fraud risk is no longer theoretical in digital workflows

If your diligence stack only starts at the title commitment, you're already late. The best teams use title insurance as the last legal backstop, not the first signal that something is wrong.

What Are the Main Types of Title Insurance Policies?

There are two main types of title insurance policies: owner's title insurance and lender's title insurance.

The difference is not technical. It's financial. One protects your equity. The other protects the bank.

Owner's Policy vs. Lender's Policy Comparison

| Feature | Owner's Title Insurance | Lender's Title Insurance |

|---|---|---|

| Who it protects | Buyer or property owner | Mortgage lender |

| Coverage amount | Typically the purchase price, plus covered legal costs under the policy | Typically the loan amount |

| Why it exists | Protects the owner's financial stake and property rights | Protects the lender's collateral position |

| How long it lasts | Can continue as long as the owner or heirs hold the property | Declines with loan payoff and ends when the mortgage is satisfied |

| Required in financed deals | Usually optional from a legal standpoint | Required in 99% of financed U.S. transactions according to the NAIC at https://content.naic.org/article/consumer-insight-vitals-title-insurance-what-you-need-know |

The misunderstanding that costs buyers money

A lot of people assume that if the lender requires title insurance, they're covered too. They're not.

A lender's policy does not insure the homeowner's equity. It insures the lender against title defects that impair the enforceability or priority of its mortgage. If a title problem wipes out value or triggers litigation, the lender can be protected while the owner still absorbs loss.

That's why an owner's policy matters. It protects the capital you've put into the deal.

What happens when a defect surfaces

The economics of title claims are unusual. Industrywide, claims payouts average under 4% to 5% of premiums collected, and defense costs make up 90% of expenditures because insurers often litigate to perfect title rather than write a simple check, as described by the NAIC in the same consumer overview.

That matters because the policy isn't just a reimbursement mechanism. It's also a legal-defense mechanism.

If you're evaluating a financed acquisition, assume the lender's policy is protecting the lender's balance sheet, not yours.

Which one should an investor or operator buy

For financed acquisitions, the practical answer is simple:

- Lender's policy: you'll almost certainly have it because the lender will require it.

- Owner's policy: buy it if you care about preserving equity, resaleability, and defense support.

For cash buyers, the lender's policy drops out. The owner's policy becomes even more important because there is no lender forcing title discipline into the process.

Skipping the owner's policy can look rational on a spreadsheet when the property appears clean. It stops looking rational when an heirship claim, forged deed, or recording mistake surfaces years later and the legal bill starts before you even know whether you still own clear title.

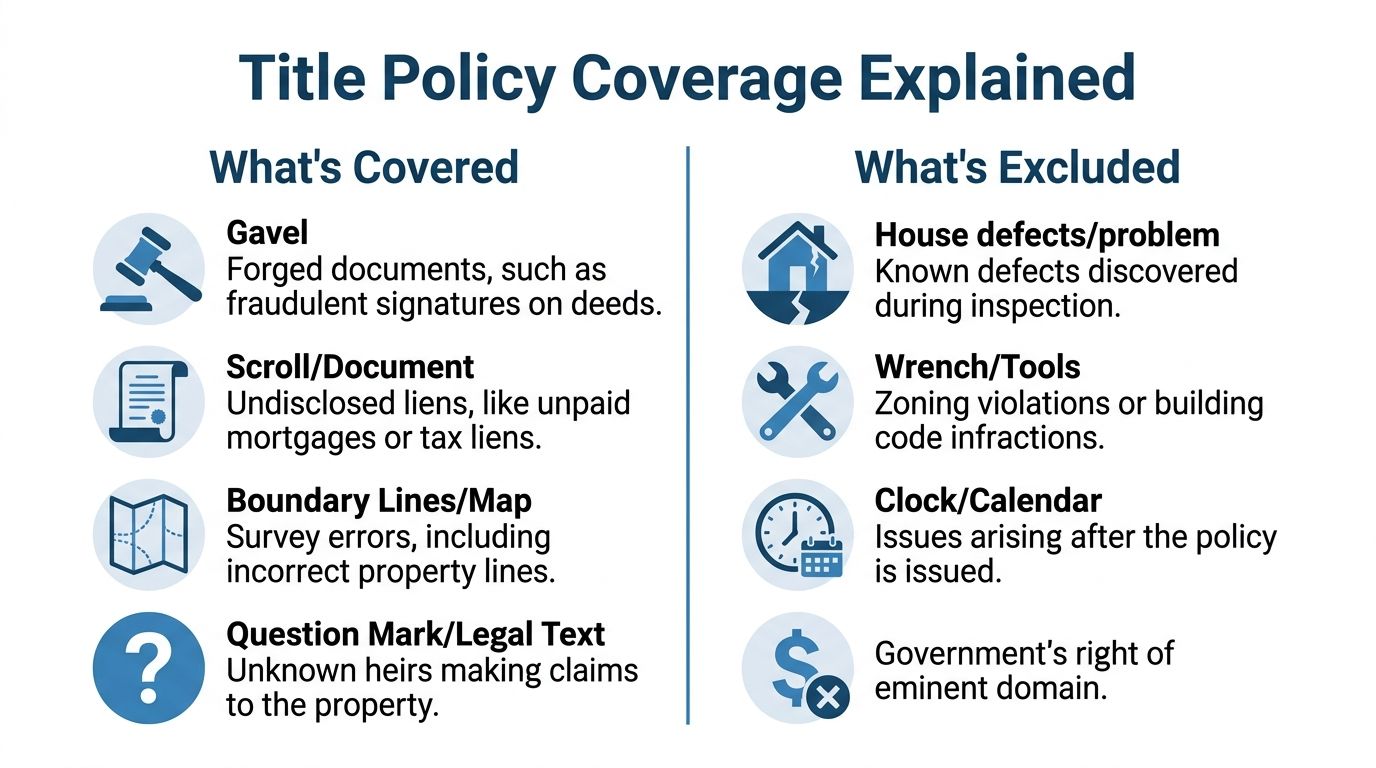

What Does a Title Policy Cover and Exclude?

A title policy covers specified title risks listed in the policy, and it does not cover exclusions and property-specific exceptions.

That's the key to reading it correctly. Most buyers only look at the premium. The useful parts are Schedule A, covered risks, exclusions, and Schedule B exceptions.

The structure matters

A standard ALTA-style policy isn't just a generic promise to help. It's a defined legal instrument.

- Schedule A: identifies the insured, policy amount, legal description, estate type, and effective date.

- Covered risks: lists the title defects the insurer agrees to cover.

- Exclusions: removes broad categories that the policy will never cover.

- Schedule B exceptions: removes specific matters tied to that property that the title company found and did not clear.

If Schedule B lists an easement, unreleased mortgage, use restriction, or survey issue as an exception, don't expect coverage for that item.

What's usually covered

Covered risks commonly include:

- Forgery: fraudulent signatures or fabricated deed activity

- Undisclosed liens: prior claims that weren't properly identified or released

- Clerical and recording errors: mistakes in public records

- Unknown heirs: later ownership claims through inheritance defects

- Invalid documents: improperly executed or legally defective instruments

What's usually excluded

Exclusions are different. These are broad categories the insurer doesn't want to own.

| Policy area | Usually treated as |

|---|---|

| Governmental regulations and eminent domain | Exclusion |

| Defects created or agreed to by the insured | Exclusion |

| Known matters listed for the property | Schedule B exception |

| Some use, permit, or zoning issues | Often excluded unless enhanced coverage modifies the risk |

Standard policy versus enhanced Homeowner's Policy

Here, much generic content falls short. Not all owner's policies are equivalent.

The enhanced Homeowner's Policy extends standard coverage with post-policy protections, graduated liability increasing to 125% of the policy amount over 5 years, and smooth trust transfers, for a premium uplift of around 15%, according to Old Republic Title's explanation of the owner's policy at https://www.oldrepublictitle.com/blog/understanding-your-owner-s-policy/.

That trade-off is practical, not theoretical. Standard policies can terminate on certain transfers and don't provide the same post-policy safeguards. Enhanced coverage is often the better fit for owner-occupants who want broader protection against later-asserted defects and transfer friction.

Underwriting lens: Don't ask whether a title policy exists. Ask which form, what exceptions remain, and whether the insured structure matches the hold strategy.

If you're acquiring through trusts, planning estate transfers, or worried about deed fraud risk, those details matter more than the base label on the closing package.

How Are Title Insurance Costs Determined?

Title insurance cost is usually a one-time closing expense based on the property's value, the policy type, the state rate environment, and the provider you choose.

The broad cost range is established. Premiums typically range from 0.5% to 1.0% of the purchase price, and Fannie Mae data cited by First American puts average title and settlement services, including the lender's policy, at $1,900 per transaction. For a median home price around $400,000, that translates to roughly $2,000 to $4,000, with the average policy cost often around $1,000 when broken out from bundled closing services.

What drives the price

Title pricing isn't one variable. It's a stack of variables:

- Purchase price or insured amount

- Whether you're buying an owner's policy, lender's policy, or both

- State regulation

- Local closing norms

- Endorsements or enhanced coverage

- Whether the provider gives a combined issue discount

Who pays can also vary by market custom and negotiation. In some areas sellers commonly pay one policy and buyers pay the other. In others, the buyer carries most of the burden. Treat this as negotiable, not fixed.

The biggest mistake buyers make

They assume the rate is fixed or that the lender's recommended title company is the only option.

The CFPB says consumers can save up to 50% or more on title insurance by comparing providers. It also notes that for a $300K home, average premiums are around $1,000 to $2,500, and rates can vary by 20% to 70% between insurers. That consumer guidance is at https://www.consumerfinance.gov/ask-cfpb/what-is-owners-title-insurance-en-164/.

That's not a rounding error. That's a material closing-cost spread.

A useful way to benchmark shopping conditions is to look at regional patterns in property markets, such as this California-focused Investor Pulse report, because fee sensitivity tends to rise in expensive markets where every closing cost gets scrutinized.

How to shop without wasting time

Use a short checklist:

- Ask for the exact policy type. Standard and enhanced aren't priced the same.

- Ask whether simultaneous issue pricing applies. Buying both policies together can reduce total cost.

- Review the title commitment, not just the quote. Cheap isn't useful if exceptions are poorly handled.

- Confirm you can choose the provider. Many buyers don't realize they can.

A low premium isn't automatically a better deal. If the title search is weak or unresolved exceptions are sloppy, you may be buying a future legal problem at a discount.

How Data is Revolutionizing Title Underwriting

Title insurance is reactive by design. Modern property data makes risk mitigation more proactive.

That shift matters because the old workflow assumes a defect appears during title review or after closing. Data platforms let insurers, lenders, servicers, and investors identify some of those issues earlier, at scale, before they become surprises.

Why the old model is under pressure

Digital transaction volume has increased the value of speed, but speed creates exposure when record quality is uneven. One notable pressure point is deed fraud. Emerging trends show a 15% year-over-year increase in claims related to digital deed fraud from AI-generated forgeries, based on the Stewart overview at https://www.stewart.com/en/what-we-offer/title-insurance/what-is-title-insurance.

That isn't just a claims issue. It's a data-verification issue.

Property teams now want to know:

- Does the ownership chain look normal?

- Are lien records current?

- Has mortgage activity changed unexpectedly?

- Are there signs of distress or transaction irregularity?

- Does the asset need deeper manual review before it reaches closing?

What data changes in practice

Data doesn't replace the legal function of title insurance. It changes the sequence.

Instead of waiting for a title commitment to reveal complexity, teams can screen parcels and portfolios earlier using ownership history, mortgage and lien detail, transaction signals, and geographic context. That's especially useful in acquisition funnels, correspondent lending, servicing transfers, and portfolio monitoring.

A related workflow trend shows up in adjacent insurance operations too. This overview of AI in the insurance industry is useful because it frames the broader shift from manual review toward automated triage and decision support.

Where this becomes operationally valuable

Stewart's title insurance overview also notes that daily-updated mortgage and lien details across 155M U.S. records can support advanced risk scoring workflows. For underwriting and servicing teams, that means you can move from file-by-file detection to portfolio-level monitoring.

Use cases include:

| Workflow | Data-driven advantage | Why it matters |

|---|---|---|

| Acquisition screening | Flag properties with lien or ownership complexity before contract execution | Reduces wasted diligence spend |

| Underwriting review | Cross-check chain-of-title signals against loan file assumptions | Improves exception handling |

| Portfolio monitoring | Watch for new encumbrances or distress indicators after acquisition | Helps teams respond before disputes escalate |

Geospatial context is part of that evolution too. This analysis of how geospatial analysis enhances automated valuation models is relevant because title risk doesn't exist in a vacuum. Location, parcel relationships, and local recording patterns shape both diligence and valuation outcomes.

For a quick visual on how these workflows fit into the modern stack, this short explainer is useful:

The bottom line is straightforward. Insurance still matters, but the competitive advantage now comes from finding trouble before legal defense is required.

The Final Word on Protecting Your Investment

Title insurance remains essential, but using it as your only risk-control tool is outdated.

A serious answer to what is a title insurance policy has to do two things. It has to explain the legal product, and it has to explain where that product fits in a modern diligence stack.

The legal product is clear enough. A title policy protects against covered defects in the property's past. It does that through a mix of pre-closing title examination and post-issue defense or indemnity if a covered problem still surfaces. That's why the distinction between owner's coverage and lender's coverage matters so much. One protects the lender's position. The other protects your equity.

The operational lesson is broader. Title defects are often data problems before they become insurance problems. A broken chain of title, an unreleased lien, a forged instrument, or a bad record match usually leaves signals somewhere in the property record ecosystem. Teams that surface those signals early underwrite better, close cleaner files, and spend less time reacting after the fact.

For investors, that means fewer ugly surprises tied to ownership history. For lenders and servicers, it means better file quality and stronger collateral control. For proptech platforms, it means building workflows that don't wait for a title exception to reveal what upstream data should have caught.

Insurance is the backstop. Diligence is the edge.

Use title insurance because the legal risk is real and the cost of being wrong can be severe. But don't stop there. The smarter approach is layered. Start with better data, verify the ownership story early, inspect exceptions carefully, and treat the policy as the final shield, not the first line of intelligence.

If your team wants to underwrite, monitor, or diligence property risk with more precision, BatchData gives you access to 155M+ U.S. property records, daily-updated mortgage and lien data, ownership history, valuations, and portfolio monitoring tools that help surface title-related risk before it turns into a claim.