SEO Title: Broward Property Taxes Guide for Investors and APIs

Meta Description: Learn how property taxes in Broward work, how to calculate them, track exemptions, manage payments, and use tax data in underwriting workflows.

Meta Keywords: property taxes in broward, broward property tax calculation, broward millage rate, broward homestead exemption, broward property tax payment, broward tax data api, broward assessment appeal, broward investors tax guide

A single number explains why property taxes in Broward deserve close attention: the average single-family tax bill reached approximately $5,300 in 2020, up 13% from $4,700 in 2019 as home values moved above $400,000 amid stable nominal tax rates, according to ATTOM’s Broward County analysis.

That’s the pattern that confuses people. They see a stable posted rate and expect a stable bill, then assessed values rise and the tax bill follows. Homeowners feel it, but investors, servicers, insurers, and proptech teams need to model it with much more precision.

This guide is built for that. It walks through the calculation logic, the local millage stack, exemption and deferral mechanics, payment workflows, appeal discipline, and the practical side of pulling Broward tax data into underwriting and portfolio systems. If you’re also evaluating total carrying costs on a Florida property, it’s worth pairing tax analysis with adjacent cost drivers like Florida solar incentives and local market context from the Florida Investor Pulse report.

Quick takeaways

- Your bill starts with taxable value. Assessed value is reduced by exemptions before millage is applied.

- Millage is layered. County tax is only one piece of the final bill.

- Timing matters. Billing, discounts, and delinquency dates directly affect cash management.

- Deferral isn’t forgiveness. It creates a lien and changes downstream risk.

- APIs matter for scale. Portfolio monitoring breaks when tax data stays manual.

Introduction

Property taxes in Broward aren't hard because the formula is mysterious. They’re hard because several moving parts interact at once, and each one can distort what an owner or analyst expects.

A homeowner may focus on market value. A lender may focus on escrow. An investor may care about post-acquisition reset risk. An insurer may care about delinquency signals. All of them are looking at the same tax system, but from different operational angles.

That’s why a useful Broward guide has to do two jobs at the same time. It has to explain the basics in plain language, and it has to translate those basics into decisions you can automate, underwrite, and monitor.

Where readers usually get tripped up

Most confusion comes from four terms that sound similar but mean different things:

- Market value is what the property may be worth in the market.

- Assessed value is the value placed by the Property Appraiser for tax purposes.

- Taxable value is the assessed value after exemptions are applied.

- Millage rate is the rate charged per $1,000 of taxable value.

Property taxes in Broward are not a single county number. They are a stacked local bill built from multiple taxing authorities.

If you keep that distinction clear, the rest gets easier. If you blur those terms together, every estimate starts to drift.

Why this matters beyond homeowners

For operators, tax data is more than a bill. It’s an underwriting input.

- Investors use it to estimate carry and exit economics.

- Mortgage teams use it to set and adjust escrow.

- Insurance and risk teams use it to spot distress or lien exposure.

- Proptech teams use it to enrich parcel-level models with public tax fields.

That’s the practical lens for the rest of this article.

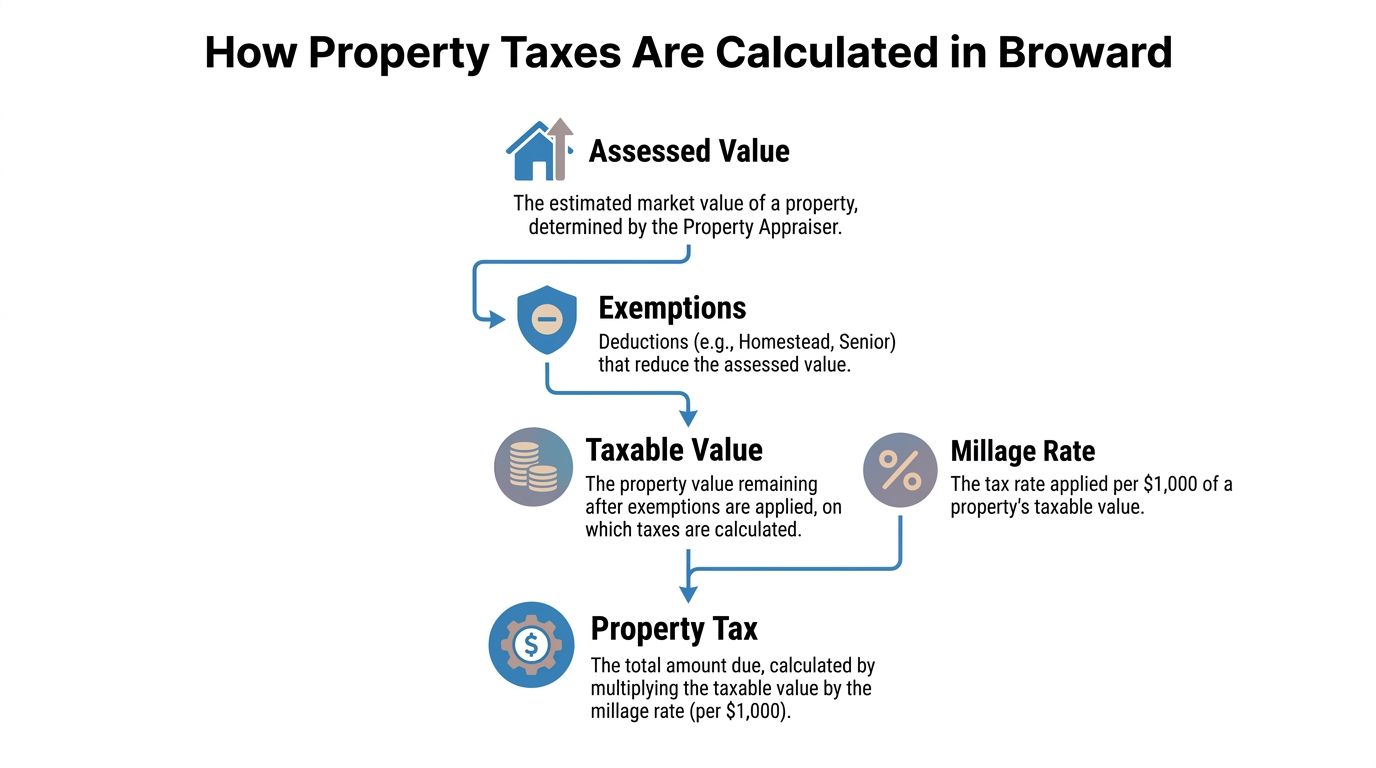

How are property taxes calculated in Broward

Property taxes in Broward are calculated by taking taxable value and applying the total millage rate. Broward’s tax estimator framework states that taxable value equals assessed value minus exemptions, and that for FY2021 the BCC rate was 5.669 mills, which produced $567 in county taxes on $100,000 of taxable value, according to the Broward tax estimator reference.

A clean visual helps before we get into the mechanics.

The formula in plain English

The core formula is simple:

- Start with the assessed value.

- Subtract any qualified exemptions.

- The result is taxable value.

- Apply the combined millage rate for that parcel.

- Divide by $1,000 because millage is quoted per thousand.

That’s it. The complexity comes from knowing which exemptions apply and which taxing authorities are included.

The four inputs you must verify

If you’re calculating a Broward estimate, verify these inputs first:

- Parcel identity: Pull the right parcel by address or parcel ID. Misidentification breaks the whole estimate.

- Assessed value: Use the current assessed figure from the Property Appraiser’s record.

- Exemptions: Confirm whether homestead or other exemptions are active.

- Millage stack: Don’t stop at the county line item. Local layers matter.

Practical rule: Never calculate from sale price alone. Broward taxes are based on tax records, exemptions, and jurisdiction-specific millage, not your gut sense of market value.

A simple worked example

Use a hypothetical property with a $300,000 assessed value and a $50,000 homestead exemption.

The flow looks like this:

| Item | Amount |

|---|---|

| Assessed value | $300,000 |

| Less homestead exemption | $50,000 |

| Taxable value | $250,000 |

| Apply total millage | Parcel-specific |

You can calculate the county portion the same way the BCC example works. If county tax is charged per $1,000 of taxable value, then taxable value is reduced first, and the county rate is applied after.

That distinction matters. People often subtract an exemption after computing taxes. That’s wrong.

A video explanation can help if you want a second format for the same logic.

Common calculation mistakes

The errors are predictable:

- Using market value instead of assessed value

- Forgetting that exemptions reduce taxable value

- Applying only the BCC millage and ignoring other jurisdictions

- Assuming a stable millage rate means a stable bill

If you’re teaching this to a junior analyst, make them write the formula in words before they touch a spreadsheet. That usually fixes most mistakes fast.

What are the local millage rates and timelines

Broward property taxes are built from multiple local rates, and the payment calendar matters almost as much as the rate itself. For FY2025-26, the Broward County Commission reduced its millage rate to 5.6658 mills, the first decrease since 2018, while overall tax bills still rose because property values surged, as reported by WLRN’s Broward property tax coverage.

That single fact explains a lot of taxpayer frustration. The posted county millage can edge down while the actual bill still goes up.

What makes up the Broward millage stack

Your bill usually includes several categories:

- County commission levy

- School-related levy

- Municipal levy

- Special district levy

The county line item is important, but it isn’t the entire story. On many parcels, the school and municipal layers are just as important to the final bill.

Broward Millage Components and Deadlines

| Jurisdiction | Rate (mills) | Billing Date | Penalty Start |

|---|---|---|---|

| Broward County BCC | 5.6658 | November 1 | April 1 |

| School levy | Varies by parcel | November 1 | April 1 |

| Municipal levy | Varies by city | November 1 | April 1 |

| Special districts | Varies by parcel | November 1 | April 1 |

The dates that actually drive cash management

Broward’s tax calendar has a rhythm you need to respect:

- Bills are issued by November 1

- Taxes are due by March 31

- Early payment discounts can reach up to 4% in November

- Unpaid taxes become delinquent on April 1

- After delinquency, the charge includes 3% plus fees

If you manage escrows, acquisitions, or servicing operations, these dates are not administrative trivia. They affect customer communications, reserve planning, and delinquency control.

Why stable rates can still mean rising bills

Readers often ask the same question: if the rate didn’t move much, why did the tax bill rise?

The answer is taxable value growth.

A millage rate is only one side of the equation. If assessed or taxable values increase, the total bill can rise even with a flat or slightly lower millage figure. That’s what happened in Broward. The county commission rate moved down modestly for FY2025-26, but higher property values still pushed bills higher.

Don’t judge tax pressure by millage headlines alone. Pull the prior and current taxable values for the parcel and compare both.

What to track operationally

Different users should watch different fields:

| User type | Primary concern | What to monitor |

|---|---|---|

| Homeowner | Bill timing | Billing date, discount window, due date |

| Investor | Carry cost drift | Taxable value changes and full levy stack |

| Servicer | Escrow adequacy | Updated bill amount and delinquency timing |

| Insurer | Lien exposure | Payment status and tax-sale progression |

The practical point is simple. If you only store one annual tax number, you won’t know why that number changed.

Which exemptions can lower your property tax bill

Exemptions lower your bill by reducing taxable value, and deferrals change when taxes must be paid. Florida’s homestead deferral under Fla. Stat. 197.252 lets qualified owners delay ad valorem taxes as a lien with interest until sale or death, requires annual affidavits, and can materially reduce upfront non-school tax costs, according to the Broward Tax Collector FAQ on property tax deferrals.

That sentence includes three ideas people often lump together. Exemption reduces the tax base. Deferral postpones payment. Lien means the tax obligation still follows the property.

The exemption categories most people care about

Start with the common buckets:

- Homestead exemption

Reduces taxable value for qualifying primary residences. The Broward tax estimator materials reference a homestead example of up to $50,000. - Senior-related exemptions

Available in some qualifying circumstances and tied to eligibility rules. - Disability-related exemptions

Can reduce taxable value if the owner qualifies under the governing rules. - Veterans exemptions

Certain veterans may qualify based on disability-related criteria. - Deferrals

These don’t erase taxes. They postpone payment and create a lien structure.

Where owners get confused

A lot of owners hear “tax relief” and assume every program works the same way. It doesn’t.

| Tool | What it does | Main risk if misunderstood |

|---|---|---|

| Homestead | Reduces taxable value | Owner assumes it applies automatically |

| Senior or disability relief | May reduce taxable value further | Owner misses documentation or timing |

| Veterans relief | Can lower taxable value based on eligibility | Owner uses outdated eligibility assumptions |

| Deferral | Postpones payment as a lien | Owner treats it like forgiveness |

Deferral deserves extra caution

Deferral can help with cash flow, but it changes risk.

- The tax doesn’t disappear. It becomes a lien with interest.

- Annual filings matter. The affidavit requirement is ongoing.

- Trigger events matter. Sale, death, ownership change, or loss of eligibility can force resolution.

A deferred tax bill is still part of the property’s balance-sheet reality. Underwriters and buyers need to treat it that way.

A practical sorting approach

If you’re reviewing a Broward parcel, ask these questions in order:

- Is this the owner’s primary residence?

- Is homestead active on the record?

- Are there any senior, disability, or veteran-related benefits shown?

- Has the owner elected a deferral that creates a lien?

- If yes, who needs to know right now. Buyer, lender, servicer, or insurer?

That workflow keeps exemptions and deferred liabilities from getting mixed together.

How to look up and pay property taxes in Broward

To look up property taxes in Broward, start with the property record, confirm the parcel details, then move to the tax payment portal to review the current bill and payment status. Most user errors happen before payment, not during payment.

Lookup starts with identity, not payment

Use the parcel ID or the property address and verify that the record matches the property you expect.

Check for:

- Owner name consistency

- Property address match

- Assessed and taxable value fields

- Exemption status

- Tax year alignment

If your parcel pull is wrong, every later step becomes noise. This is common in condos, similar street names, and parcels with recent transfer activity.

Then review the tax bill

Once you have the right property, look at the current tax view for:

- Bill amount

- Whether the bill is paid or unpaid

- Any installment or escrow handling

- Due timing

- Any delinquency indicators

Broward bills are issued by November 1 and due by March 31, with early payment discounts available before that due date and delinquency starting April 1, as noted earlier in this guide.

The practical payment channels

Readers usually want to know what methods are available. The county supports common channels such as:

- Online payment

- In-person payment

- Mortgage escrow payment when applicable

If you’re paying directly, save your confirmation details and make sure the parcel reference is correct. If a mortgage servicer is supposed to pay, don’t assume it already happened. Verify the tax status.

Avoid the usual mistakes

These are the errors that cause preventable trouble:

- Wrong parcel number

This happens more often than people admit. - Expired card or failed online submission

Always confirm completion, not just form submission. - Ignoring escrow assumptions

Borrowers often think the lender paid when the account wasn’t set up that way. - Waiting until the end of March

That leaves no room to fix a rejected payment.

A simple payment discipline

Use this sequence:

- Confirm parcel identity.

- Confirm the tax year.

- Verify whether taxes are already escrowed.

- Pay early enough to preserve any available discount.

- Save proof of payment.

- Recheck posted status.

That’s not glamorous, but it prevents most avoidable disputes.

How to appeal your Broward County tax assessment

To appeal a Broward assessment, start with the property record, identify exactly what looks wrong, and build evidence before you file anything. Most weak appeals fail because the owner argues from frustration instead of documented valuation support.

What an appeal is really about

An appeal is not a complaint about taxes being high. It’s a challenge to the assessed value, classification, or exemption treatment used for tax purposes.

That distinction matters. If values increased because the local market moved, saying “my bill jumped too much” doesn’t prove the assessment is wrong.

A disciplined review process

Use a sequence like this:

- Audit the record

Check the parcel facts, exemptions, and classification. - Identify the issue

Is the problem value, exemption status, or something else in the tax record? - Gather support

Use comparable property data, income support where relevant, and anything else that directly addresses the assessed value question. - Request informal review

A direct conversation can sometimes resolve obvious record issues. - Escalate if needed

If the issue remains, prepare the formal petition path.

What evidence carries weight

Useful evidence tends to be specific and property-centered:

- Comparable sales

- Income and expense support for income-producing property

- Proof that the record contains incorrect physical details

- Evidence of exemption eligibility if the issue is exemption-related

Weak evidence usually sounds like this:

- “Values in the area feel inflated.”

- “Taxes are hurting owners.”

- “My neighbor said their bill looks lower.”

The appeal file should read like an analyst’s memo, not a grievance letter.

The timing problem

Appeal opportunities are time-sensitive, and owners often act too late because they wait until the bill arrives. By then, the practical review window may already be tighter than expected.

The right habit is to monitor notices and tax record changes early, then decide quickly whether an informal correction request or a formal filing is warranted.

When an appeal is worth the effort

An appeal is usually more sensible when:

| Situation | Appeal logic |

|---|---|

| Record facts appear wrong | Strong reason to push for correction |

| Exemption was missed or removed incorrectly | High priority review item |

| Market evidence clearly undercuts the assessment | Possible value challenge |

| Bill is simply higher than expected | Not enough by itself |

The strongest appeals are narrow, documented, and timely.

How do investors lenders and insurers leverage Broward tax data and APIs

Investors, lenders, and insurers use Broward tax data to automate underwriting, monitor carry-cost drift, and detect emerging risk at the parcel level. A November 2025 report found that proposed legislative reforms, HJR 205 and HJR 207, could erase up to 11% of Broward’s tax base countywide, with outsized effects in senior-heavy cities, according to WLRN’s report on Broward tax reform risk.

That’s not just a policy headline. It’s a modeling input.

What teams actually pull from tax datasets

A practical Broward tax payload usually includes:

- Parcel identifier

- Assessed value

- Taxable value

- Exemption indicators

- Current and historical tax amounts

- Jurisdictional tax breakdown

- Payment or delinquency status where available

The reason to use API delivery isn’t novelty. It’s repeatability. Manual lookups fail once you scale beyond a handful of properties.

A documentation-style visual helps frame what a tax integration usually looks like.

A minimal API workflow

At a high level, technical teams usually do this:

- Match a property by address or parcel ID.

- Pull tax and assessment attributes.

- Normalize county and municipal fields into your internal schema.

- Join tax data to ownership, mortgage, valuation, and geography layers.

- Trigger alerts when monitored fields change.

Example logic in Python

parcel_id = "example_parcel_id"

tax_record = get_tax_record(parcel_id)

assessed_value = tax_record.get("assessed_value")

taxable_value = tax_record.get("taxable_value")

exemptions = tax_record.get("exemptions")

millage_components = tax_record.get("millage_components")

current_tax = tax_record.get("current_tax_amount")

if tax_record.get("delinquent"):

create_alert(parcel_id, "Tax delinquency review")

This isn’t tied to a single vendor schema. It shows the operational shape of the problem.

Example logic in JavaScript

async function reviewParcel(parcelId) {

const taxRecord = await getTaxRecord(parcelId);

return {

parcelId,

assessedValue: taxRecord.assessed_value,

taxableValue: taxRecord.taxable_value,

exemptions: taxRecord.exemptions,

currentTax: taxRecord.current_tax_amount,

delinquent: taxRecord.delinquent

};

}

Why API tax data matters for each audience

Different teams use the same fields differently.

| Team | Use case | Why tax data matters |

|---|---|---|

| Investors | Acquisition and hold analysis | Taxes affect yield and carry |

| Mortgage servicers | Escrow management | Tax drift can create shortages |

| Insurance teams | Risk review | Delinquency and liens change exposure |

| Real estate portals | Consumer display and search | Accurate tax context improves property understanding |

Joining taxes to other datasets

Tax data gets more useful when combined with:

- AVMs and pricing models

- Ownership records

- Mortgage data

- Geospatial layers

- Permit or improvement records

That’s where geospatial context becomes useful. Tax burden rarely exists in isolation, and parcel-level modeling improves when tax fields are analyzed alongside location intelligence, as described in this piece on how geospatial analysis enhances automated valuation models.

If you’re underwriting rehab or resale property, tax analysis also pairs well with renovation economics. For example, bathroom scope can alter total project math, and this discussion of bathroom renovation ROI is useful when you’re combining tax carry with improvement budgeting.

One modeling issue many teams still miss

Legislative reform risk can change local revenue assumptions without changing your current parcel data immediately.

If proposed changes can reduce the countywide tax base materially, then analysts should stress test:

- Municipal service stability

- Local fiscal pressure

- Tax burden redistribution

- Downstream valuation sensitivity in specific submarkets

For teams building this into systems, BatchData is one example of a property data platform that can deliver assessment, ownership, valuation, and related parcel attributes through APIs or bulk delivery so tax signals can be joined with the rest of the underwriting stack.

If your monitoring only stores “last year taxes” and “this year taxes,” you’re not modeling the cause of change. You’re just observing the outcome after the fact.

What are the next steps to use Broward tax data effectively

The next step is to turn property taxes in Broward from a once-a-year bill into a repeatable operating process. That means calculation discipline, exemption review, payment control, and data integration all have to work together.

A practical checklist by role

| Role | First priority | Second priority | Ongoing task |

|---|---|---|---|

| Homeowner | Confirm exemptions | Pay on time | Watch assessment notices |

| Investor | Model full tax stack | Review carry assumptions | Track parcel-level changes |

| Lender or servicer | Verify escrow treatment | Monitor updated tax bills | Watch delinquency risk |

| Insurer | Review lien exposure | Check payment status | Monitor policy-sensitive areas |

What to do first if you own one property

Keep it simple:

- Pull the current record

Confirm assessed value, taxable value, and exemption status. - Read the bill line by line

Don’t focus only on the total. - Pay with timing in mind

Discounts and delinquency dates matter. - Review changes promptly

If something looks off, act before deadlines close in.

What to do first if you manage a portfolio

Portfolio work needs a system, not reminders in a calendar.

- Standardize parcel IDs

Tax data gets messy when identifiers don’t match cleanly. - Store historical fields

Keep prior assessed value, taxable value, exemptions, and tax amounts. - Create alert rules

Flag exemption changes, delinquency status, or major bill movement using your internal thresholds. - Separate owner-occupied and investor logic

Homestead and deferral treatment can change interpretation.

What to monitor over time

For ongoing management, watch for changes in:

- Taxable value

- Exemption status

- Jurisdictional bill components

- Payment status

- Local policy proposals

A static annual export won’t do much for this. Ongoing review is the only way to catch drift before it turns into a borrower issue, a missed underwriting assumption, or a portfolio surprise.

Where to keep learning

If you want a broader market-level view, the Investor Pulse reports library is a useful place to compare statewide and regional housing signals against tax and valuation workflows.

The bigger point is this: Broward tax management is a data discipline. Owners need clarity. Investors need repeatable models. Lenders and insurers need alerts tied to real parcel changes. If you build around those needs, the tax system becomes manageable.

If you need property tax, assessment, ownership, and valuation fields in one workflow, BatchData is worth evaluating as a practical data source. Teams use it to pull parcel-level records through APIs or bulk delivery, then connect those records to underwriting, servicing, monitoring, and marketing systems without relying on manual county-by-county lookups.