SEO Title: Property Risk Assessment Guide for Modern Teams

Meta Description: Learn how property risk assessment works, which data matters, how scores are calculated, and why stale or bad location data breaks models.

Meta Keywords: property risk assessment, property risk scoring, geospatial risk modeling, address validation, hazard data integration, real estate risk analysis, underwriting property data, portfolio risk monitoring

Most property risk failures don't start with the hazard. They start with process gaps, and one of the clearest signs is that 42% of organizations reported risk management wasn't involved in decisions about building or acquiring new facilities.

That single fact reframes the topic. Property risk assessment isn't just a technical exercise for underwriting teams. It's a decision system for acquisitions, lending, insurance, operations, and asset management. If risk only shows up after a site is chosen or a loan file is assembled, the model is already being asked to clean up a business process problem.

A modern approach fixes that. It uses verified location data, parcel-level attributes, hazard overlays, property condition inputs, and continual refreshes so teams can make repeatable decisions instead of arguing over anecdotes.

What matters most in practice

- Property risk assessment is operational. It informs underwriting, premium setting, loan terms, inspection strategy, and loss control.

- Bad location data breaks everything downstream. If the address or parcel match is wrong, the hazard score is noise.

- Static models miss real exposure. Roof age, occupancy changes, maintenance drift, and regulatory changes can alter risk faster than annual reviews catch them.

- Scoring is only useful if it's transparent. Teams need to know what was weighted, why, and what action each score triggers.

- The workflow matters as much as the model. Clean ingestion, identity resolution, review rules, and monitoring usually determine whether the program works at scale.

Many teams know the risk categories. Fewer know where the model fails.

Introduction to Modern Property Risk Assessment

Modern property risk assessment is the shift from broad, judgment-heavy screening to property-level, continuously updated analysis.

The old method was simple. Pull a few public records, glance at a hazard map, note the neighborhood, and let a human reviewer bridge the gaps. That still happens, and it's why many organizations end up with inconsistent decisions across portfolios.

The more useful model is narrower and more demanding. It starts with the exact asset, not the ZIP code. It asks whether the property identity is verified, whether the parcel match is correct, whether the building condition is current, and whether the hazard, operational, and regulatory inputs are fresh enough to trust.

Why the old approach keeps failing

A lot of organizations still treat property risk as an insurance subtask instead of an enterprise discipline. That mindset shows up in process design, ownership, and timing. Risk gets asked for an opinion after the important business decision has already been made.

Practical rule: If the risk team enters after acquisition, site selection, or credit structuring, the assessment is being used as documentation, not control.

That creates predictable failure points:

- Late involvement: The team reviewing risk isn't shaping the decision.

- Overreliance on static records: The model reflects what the property used to be, not what it is now.

- Patchwork data assembly: Different systems disagree on the same asset.

- False confidence in scores: A polished risk score can still be built on the wrong building.

What a modern program should deliver

A working property risk assessment program should give a senior operator four things:

| Output | What it should answer | Why it matters |

|---|---|---|

| Asset identity | Are we analyzing the correct property and structure? | Prevents bad parcel matches and wrong hazard linkage |

| Current exposure | What can happen to this asset given its location and condition? | Supports underwriting, lending, and inspection decisions |

| Decision signal | What action should this score trigger? | Enables routing, pricing, review, and mitigation |

| Change detection | What has changed since the last review? | Keeps the model useful after origination or acquisition |

Property risk assessment is no longer just about estimating damage potential. It now sits inside pricing, due diligence, servicing, and portfolio surveillance. The teams that treat it as a living operating system tend to get cleaner decisions than the teams still treating it like a once-a-year report.

What Is Property Risk Assessment Really About

Property risk assessment is the disciplined process of identifying, quantifying, and updating the exposures tied to a specific property so a business can make better decisions with less guesswork.

That definition matters because many teams still frame it too narrowly. They think of it as an underwriting checklist or a compliance form. In practice, it's closer to a control system for asset quality.

It's not just an insurance task

A lender uses property risk assessment to decide whether collateral quality supports loan terms. An insurer uses it to refine pricing, inspection priority, and loss-control actions. An investor uses it to pressure-test assumptions behind acquisition and hold strategy. An operator uses it to identify where maintenance, occupancy, or system age is subtly increasing exposure.

That broader view changes what gets measured.

A weak process asks, "Is this property in a risky area?"

A strong process asks, "Are we looking at the correct structure, what can affect it, what condition is it in, what has changed, and what decision should follow?"

The real unit of analysis

The practical unit isn't a neighborhood and it isn't an address string by itself. It's the verified physical asset tied to coordinates, parcel context, building characteristics, use, and current condition.

That distinction is where a lot of new teams get tripped up. They import an address, join a flood layer, and assume they're done. They aren't. Mixed-use buildings, condo structures, subdivided parcels, and stale assessor records can all produce a technically complete but operationally wrong answer.

A model that scores the wrong structure with perfect math is still a failed assessment.

What good assessment protects

A mature property risk assessment program protects more than downside. It improves capital allocation. It helps teams avoid overpricing or underpricing risk. It surfaces where a site visit is warranted and where automation is enough. It also creates a common language across credit, underwriting, operations, and portfolio management.

Use this as the mental model:

- Insurance tells you how loss may be transferred

- Property risk assessment tells you whether the asset should be accepted, priced differently, inspected, remediated, or monitored

That difference is why strong teams build assessment into front-end workflows, not just post-decision review.

Understanding the Four Core Categories of Property Risk

Property risk falls into four broad categories: physical, financial, legal or regulatory, and market risk.

Each category captures a different failure mode. The mistake is treating them as separate silos. In real portfolios, they interact. A physically exposed property with strong maintenance may be manageable. A moderate hazard asset with poor upkeep, title issues, and weak local demand may be the worse risk.

Physical risk

Physical risk is the chance that the property itself suffers damage or operational impairment.

This category includes natural hazards, but it also includes the condition of the asset. That second part gets underestimated all the time.

Key indicators include:

- Hazard exposure: Flood, wildfire, and earthquake overlays tied to the specific location

- Building condition: Roof age and material, building age, visible maintenance issues

- Occupancy and use: The way the property is used can alter ignition, load, wear, and loss severity

- Mitigation controls: Drainage, protective systems, and repair history

The important point is interaction. Hazard layers tell you what can strike the asset. Condition and mitigation influence how much loss materializes.

Financial risk

Financial risk is the chance that the property's economics weaken the value or performance of the asset.

Some teams ignore this because it looks less technical than geospatial modeling. That's a mistake. A property can be structurally sound and still be a bad risk if the financial signals around it are deteriorating.

Common indicators:

| Indicator | What it may signal | Why teams care |

|---|---|---|

| Mortgage and lien complexity | Encumbrances or repayment stress | Affects collateral quality and recovery assumptions |

| Transaction history | Pricing volatility or unresolved issues | Helps validate current valuation assumptions |

| Insurance and financing sensitivity | Exposure to tighter terms | Influences affordability and disposition options |

Financial risk usually doesn't replace physical analysis. It sharpens it.

Legal and regulatory risk

Legal and regulatory risk covers compliance failures, title problems, zoning issues, and new rules that change the property's obligations or insurability.

This category matters more than many models acknowledge because regulation often changes faster than review cycles. A property can move from acceptable to problematic without any storm, fire, or structural event if disclosure obligations shift or local requirements tighten.

Look for:

- Title or ownership ambiguity

- Zoning or land-use conflicts

- Permit gaps or unresolved violations

- New resilience or disclosure requirements

Market risk

Market risk is exposure created by the surrounding economic and competitive environment.

The same physical building can perform very differently depending on location, demand, and neighborhood trajectory.

Examples include:

- Local demand shifts: Buyer or tenant preferences move away from a location or asset type

- Area decline: Deteriorating neighborhood conditions can weaken asset performance

- Competitive pressure: New supply can reduce pricing power or occupancy stability

A useful assessment doesn't flatten these categories into a generic score too early. Analysts should inspect them separately first, then combine them with rules that reflect the business decision at hand.

Which Data Sources and Metrics Actually Matter

The most important data in property risk assessment isn't the hazard layer. It's the asset identity layer.

That's the contrarian point many teams resist. They want to start with flood, wildfire, imagery, or predictive modeling because that's where the obvious risk story sits. But if the property record is incomplete, mismatched, or geocoded to the wrong structure, the rest of the workflow is compromised from the start.

A major blind spot in practice is address data integrity. Industry guidance stresses that a complete assessment must begin with address verification and rooftop geocoding, because imagery and remote sensing are useless when they're tied to the wrong parcel or building, especially in dense urban areas and mixed-use settings, as explained in this address verification discussion for real estate risk management.

Start with identity, not exposure

Before pulling any hazard score, confirm:

- Address normalization: Standardize the property address into a consistent format

- Rooftop geocoding: Tie the record to the actual structure, not a street centroid

- Parcel resolution: Confirm the correct parcel boundary and relationship to the building

- Record reconciliation: Align tax, insurance, inspection, and transaction records that may refer to the same property differently

If you're resolving ownership and event history across fragmented records, a tool like a transaction identification API can help link transaction events back to the correct asset identity. That matters because transaction mismatches often look like market or title risk when they are data stitching errors.

The data categories that carry the model

The core data stack is broader than most intake forms suggest.

| Data Category | Key Attributes | Purpose in Risk Assessment |

|---|---|---|

| Property identity and location | Standardized address, rooftop coordinates, parcel boundaries, unit or structure match | Ensures all downstream scoring is tied to the correct asset |

| Property characteristics | Building age, roof age and material, occupancy, use, maintenance indicators | Captures asset-specific vulnerability and likely loss severity |

| Hazard and geospatial context | Flood, wildfire, earthquake, crime, infrastructure context | Measures what external exposures can affect the property |

| Ownership and transaction data | Ownership history, sale records, mortgage and lien details | Supports due diligence, collateral review, and financial context |

| Operational change signals | Renovations, occupancy changes, natural-event aftermath | Detects when the prior score is no longer reliable |

| Market context | Comparable activity, neighborhood conditions, local trends | Adds commercial relevance to the final decision |

Freshness beats volume

Teams often ask for more data when they really need cleaner and newer data. A bloated dataset with stale records creates false precision. A smaller dataset with verified identity, current condition, and recent changes usually produces a better operational outcome.

If you're evaluating hazard ingestion options, this overview of APIs for hazard risk data integration is useful because it shows how teams assemble hazard inputs without manually stitching dozens of feeds.

What works: A unified property record with explicit confidence in address match, parcel match, and recency.

What doesn't: Pulling public records, hazard layers, and imagery into one dashboard and assuming the joins are correct.

The best analysts I know spend more time questioning joins than admiring models. That's usually the right instinct.

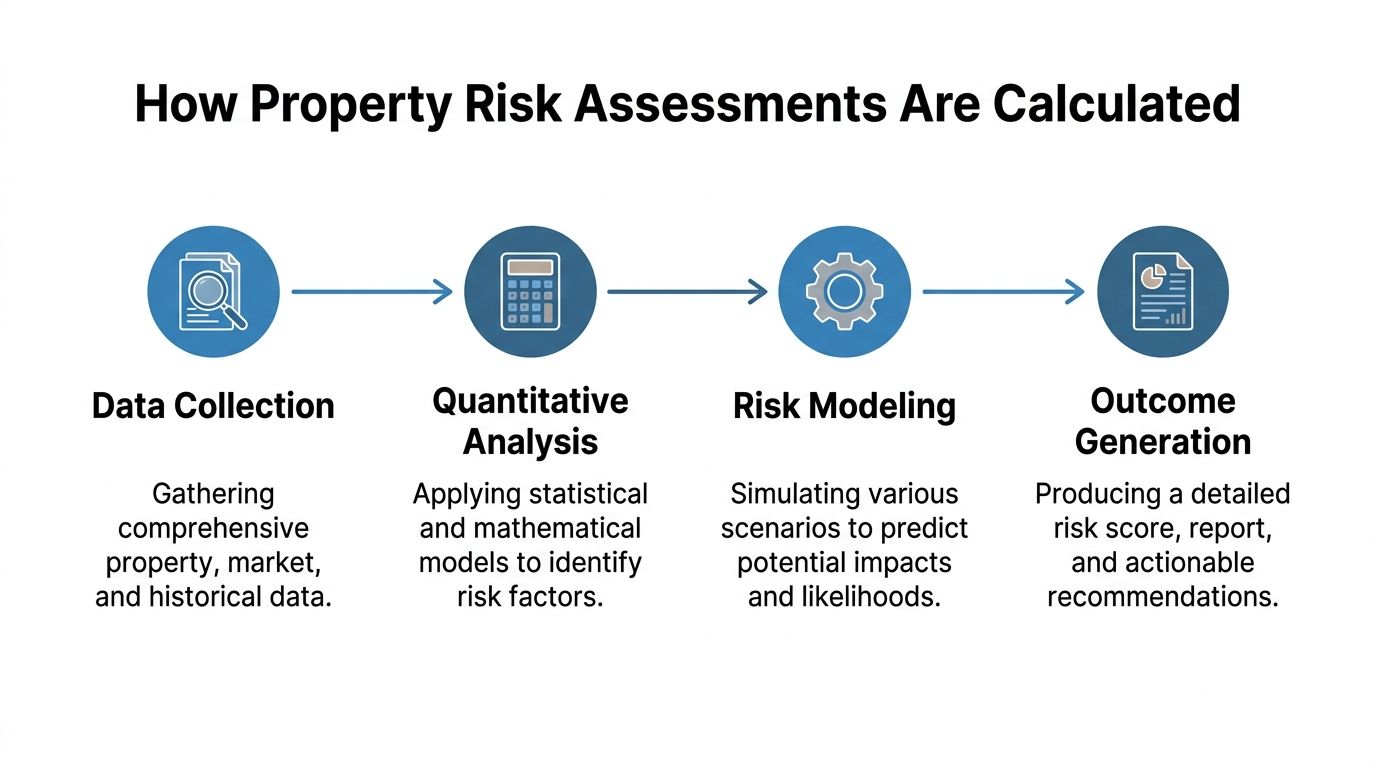

How Property Risk Assessments Are Calculated

Most property risk assessments are calculated by combining standardized inputs into a weighted score that can be repeated, audited, and updated.

The score itself isn't the point. The point is whether the method is transparent enough that two analysts, using the same inputs, would reach the same conclusion.

Weighted scoring is the common backbone

A practical model assigns weights to factors based on their relevance to the decision. One example of a weighted scheme assigns 25% to environmental hazards, 20% to crime and safety, 20% to infrastructure condition, 15% to flood risk, and 20% to earthquake risk, as shown in this explanation of location-based property risk scoring.

That doesn't mean every portfolio should use those exact weights. It means the model should make weighting explicit.

A straightforward workflow looks like this:

- Normalize inputs: Convert raw records into standard fields and ranges.

- Score each factor: Rate hazard, condition, neighborhood, and other components individually.

- Apply weights: Multiply each component by its assigned importance.

- Generate an overall score: Produce a final value tied to decision rules.

- Route the file: Trigger approval, escalation, inspection, or mitigation based on thresholds.

Geospatial modeling adds context

Weighted scoring is usually paired with geospatial analysis. That means taking coordinates or parcel boundaries and overlaying them against hazard layers and local context datasets. Parcel accuracy matters. A near miss in geocoding can place the building on the wrong side of a hazard boundary or attach the wrong neighborhood signal.

Some teams also use predictive methods, but even then the logic should stay explainable. If the model says the property is high risk, the reviewer should be able to see whether that signal came from condition, hazard interaction, location, or a recent change event.

Transparent beats clever

A black-box model can be mathematically complex and still be operationally weak. Senior reviewers need to understand why a file moved from low review to manual inspection.

For underwriting teams building these pipelines, this guide to property data for insurance underwriting and risk assessment APIs is a practical reference because it maps data inputs to insurer workflows instead of treating scoring as an isolated analytics task.

A defensible score is one you can explain to underwriting, credit, operations, and compliance without changing the story for each audience.

That's the standard worth holding.

How to Implement a Risk Assessment Workflow

A workable property risk assessment workflow turns raw property data into repeatable business decisions and then keeps those decisions current.

Most implementations fail because they focus on model design before they settle operational ownership. Decide who owns identity resolution, who approves data overrides, what triggers reassessment, and which score bands map to which actions. Without that, the workflow becomes an analytics project with no control function.

Define the decision before the score

The first question isn't "How do we score properties?" It's "What decision will this score govern?"

The same asset can be acceptable for one use case and unacceptable for another. A lender, insurer, and acquisition team won't necessarily use the same thresholds. Set that upfront.

Good implementations define:

- Decision objective: Origination, renewal, acquisition, servicing, inspection triage, or portfolio watchlist

- Risk tolerance: Which conditions trigger automation, exception review, or decline

- Escalation rules: Who reviews borderline or conflicting cases

- Evidence standards: What data fields are required for a score to be considered valid

Build a controlled intake and matching layer

This phase is where most hidden errors enter. Teams often spend heavily on hazard feeds and then underinvest in matching logic, key management, and field lineage.

Use a structured intake:

- Ingest source records from tax, transaction, market, inspection, and geospatial systems.

- Normalize identifiers so addresses, parcels, and ownership entities can be reconciled.

- Resolve duplicates and conflicts with explicit rules, not analyst guesswork.

- Create a master property record that the score engine uses.

If your team is stitching records from multiple vendors and internal systems, this guide on how to integrate data without breaking keys or grain is worth reading because key integrity problems are one of the fastest ways to poison a risk workflow.

Run the model and force an action

Once the record is clean, apply the model and attach the score to a real business action. Don't stop at "low, medium, high." Define what each label does.

| Score Outcome | Typical Action | Operational purpose |

|---|---|---|

| Low concern | Automated pass or standard terms | Preserves analyst time |

| Moderate concern | Manual review or targeted documentation request | Resolves uncertainty efficiently |

| High concern | Inspection, revised pricing, mitigation plan, or decline | Contains exposure before commitment |

Strong workflows also incorporate property condition and change over time. Guidance on property condition in risk assessment emphasizes evaluating roof age, building age, occupancy, and maintenance, then refreshing the assessment after events like renovations or natural disasters because exposure alone doesn't determine loss. The condition of the property shapes realized damage.

This short walkthrough is a useful complement if you're mapping process ownership across teams.

Monitoring is part of the workflow, not an add-on

A property that passed review six months ago may not deserve the same score today. Occupancy can change. Systems can age. Repairs can be deferred. Local rules can tighten.

The practical answer is event-driven reassessment. Instead of waiting for annual reviews, define triggers that re-open the file. That can include major renovations, hazard events, occupancy changes, permit activity, or updated imagery review.

Teams that operationalize this well don't treat monitoring as surveillance theater. They tie it to score refresh, routing, and action.

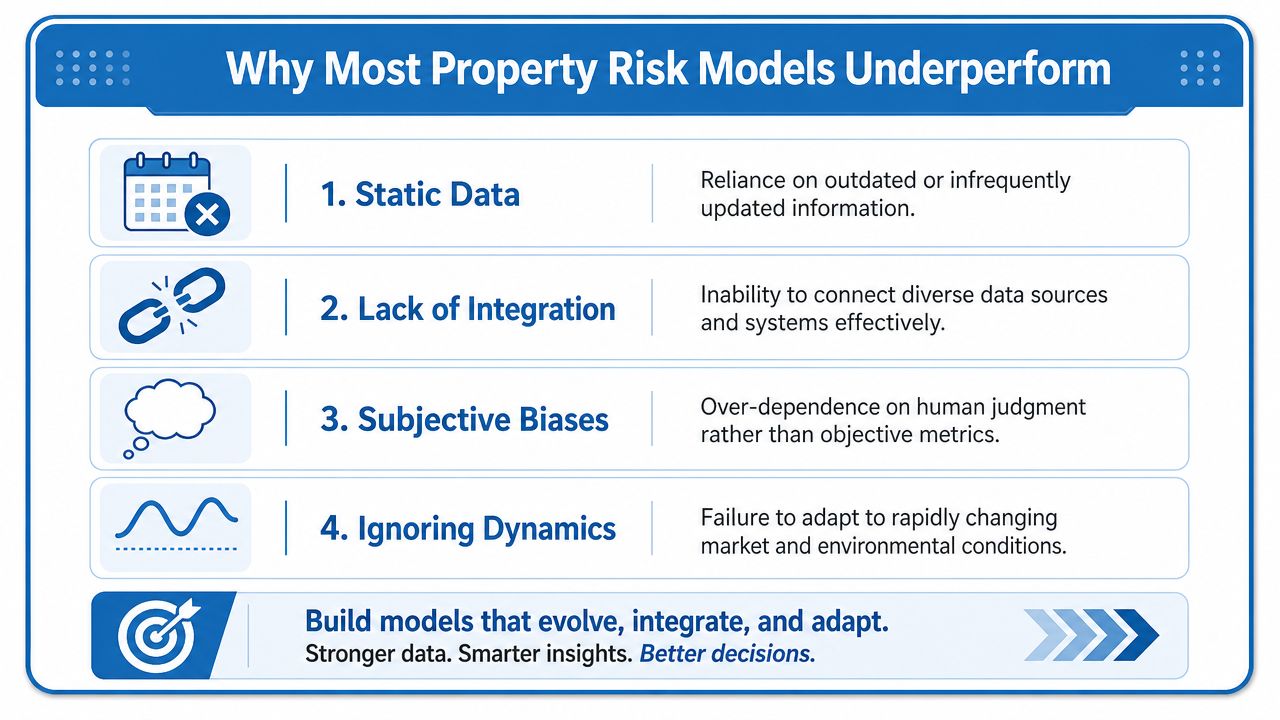

Why Most Property Risk Models Underperform

A large share of model error in property risk work starts before scoring. It starts with bad asset identity, stale records, and workflow gaps that let those issues pass into production.

Teams often blame calibration, feature selection, or model choice. In practice, underperformance usually comes from operational failure. The file points to the wrong parcel. The address was never standardized. Hazard, ownership, and condition records were joined on a weak key. A manual override fixed one deal and inadvertently broke consistency across the next hundred.

The common failure pattern

The failure usually looks ordinary at first. A property enters the pipeline with an incomplete or poorly formatted address. The system returns a near match instead of a verified match. Analysts proceed anyway because the record looks close enough, and the model scores the wrong asset or an outdated version of it.

From there, the errors stack up:

- Static data: The property record reflects a prior state of the asset, not current occupancy, condition, or improvements

- Weak entity resolution: Hazard, parcel, transaction, and servicing data attach to different versions of the same property

- Manual patching: Analysts fill gaps with spreadsheet edits and one-off overrides that do not scale or audit cleanly

- Narrow model scope: The score captures exposure but misses condition, regulatory change, maintenance drift, and market signals

Poor address validation is one of the most expensive examples because it creates false confidence. A model can look precise while scoring the wrong structure, the wrong parcel boundary, or a neighboring asset with a different exposure profile. By the time someone catches it, the bad record has already affected underwriting, pricing, reserve logic, or portfolio reporting.

Staleness is the second recurring problem. As noted in continuous property risk reassessment, a property's profile can change well inside a traditional annual review cycle. Roof age, deferred maintenance, permit activity, occupancy changes, and local code shifts all alter loss potential. If the operating model only refreshes on a fixed calendar, the score degrades long before anyone sees a formal exception.

What better looks like

Strong performance comes from process discipline, data controls, and clear decision ownership.

Property risk assessment works when the system can verify the asset, detect what changed, and route the next action without relying on memory or ad hoc cleanup.

That usually includes:

- Verified asset identity before scoring

- Condition-aware modeling alongside hazard inputs

- Reassessment triggers tied to real events

- Defined ownership across risk, operations, and review teams

- API-first delivery so refreshed data reaches production systems without manual rework

Modern data infrastructure matters at this stage because it reduces reconciliation work and keeps teams focused on judgment instead of cleanup. BatchData provides U.S. property records, ownership history, valuations, lien and mortgage context, and monitoring-oriented delivery options. For dynamic risk programs, that unified property layer is more useful than another disconnected dashboard.

The portfolios that struggle most are rarely missing an advanced model. They are missing reliable identity resolution, current records, and a workflow that turns new information into a fresh decision before exposure changes again.

If you're building or rebuilding a property risk assessment workflow, BatchData is worth evaluating as the property data layer behind it. Teams use it to unify core property records, ownership history, valuation context, and monitoring inputs so scoring, underwriting, and portfolio review can run on the same underlying asset record instead of fragmented files and manual joins.