SEO Title: Home Warranty Worth It? Cost, Caps, and Break-Even Math

Meta Description: A data-driven look at whether a home warranty is worth it, including costs, exclusions, break-even math, and better alternatives.

Meta Keywords: home warranty worth it, home warranty cost, home warranty break even, home warranty pros and cons, home warranty alternatives, home warranty claim denial, home warranty coverage, home warranty for older homes

Claim friction is common enough that it should be part of the purchase decision from the start. A home warranty only makes financial sense if the value of smoother repair budgeting outweighs claim limits, service fees, contractor restrictions, and the chance that a failure falls into an exclusion.

That changes the usual framing. The question is not whether a warranty sounds reassuring. The question is whether prepaying for capped repair access beats keeping the same dollars in reserve and paying market rates only when something breaks.

The answer shifts over time. Early in a system's life, failure odds are lower, so the warranty often functions like expensive budget insurance. As equipment ages, failure risk rises, but so does exclusion risk tied to maintenance history, rust, corrosion, or pre-existing conditions. That means the value proposition can improve for a few years, then weaken right when homeowners expect coverage to matter most.

A useful starting point is simple: home warranties sell payment predictability, not open-ended protection.

Quick takeaways

- Break-even math matters more than headline coverage. Annual premiums, service call fees, payout caps, and denied or partial claims all affect whether you come out ahead.

- The strongest use case is narrow. Owners of older homes, buyers with limited post-closing cash, and households that prioritize repair budgeting over contractor choice tend to get the most practical value.

- The value can erode as systems age. Older equipment raises the chance of a covered failure, but it also raises the chance of disputes over condition and exclusions.

- Control has a cost. Many plans limit who does the work and how repairs are approved, which can reduce flexibility even when a claim goes through.

Introduction

A home warranty is worth it only when predictable repair budgeting matters more to you than maximizing payout value.

That's the core conclusion once you strip away the marketing language. The product exists to cover wear-and-tear failures that homeowners insurance usually doesn't cover, but the economics hinge on three variables: how old your systems are, how much cash you can keep liquid for repairs, and how much control you're willing to give up.

Most buyers ask the wrong question. They ask, “Will this pay for itself?” The better question is, “Would I rather pay a known annual cost, plus service fees, than absorb the risk of a large repair on my own terms?”

Practical rule: If you can comfortably self-insure and your major systems are newer, a warranty usually looks more like convenience spending than financial protection.

Three conclusions matter most:

- For owners of older homes: the warranty can function as a hedge against concentrated failure risk.

- For first-year buyers with thin reserves: it can smooth cash flow after closing.

- For disciplined owners with maintenance savings: self-insuring often preserves more control and can produce a cleaner financial outcome.

What Exactly Is a Home Warranty?

A home warranty is a service contract, not a homeowners insurance policy.

It usually covers repair or replacement of certain home systems and appliances when they fail from normal wear and tear. That distinction matters because homeowners insurance generally responds to named perils like fire or theft, while a warranty is aimed at mechanical breakdown and aging equipment.

The confusion starts because both products involve claims, contractors, and limits. But they solve different problems. Insurance handles sudden damage events. A warranty handles a narrower class of routine breakdown risk, with more exclusions than many buyers expect.

Coverage scope in plain English

The simplest way to evaluate a warranty is to separate common inclusions from common exclusions before you ever compare prices.

| Category | Typically Covered | Typically Excluded |

|---|---|---|

| Major systems | HVAC, plumbing, electrical, water heater | Failures tied to lack of maintenance, rust, corrosion, mismatched components |

| Kitchen and laundry appliances | Dishwasher, oven/range, garbage disposal, some built-in appliances | Cosmetic defects, pre-existing conditions |

| Structural and exterior items | Limited in many standard plans | Roof structure, landscaping, structural components, many exterior issues |

A lot of frustration comes from buyers assuming “home systems” means “anything expensive in the house.” It doesn't. Contracts often narrow coverage with definitions, caps, and maintenance requirements.

For plumbing-specific questions, local explanations can be more useful than national marketing pages. This guide for Big Bear plumbing warranty is a good example because it focuses on what homeowners usually want to know first: where plumbing coverage tends to apply and where contracts often draw the line.

Why this distinction matters before you buy

If you're purchasing a property and the seller offers coverage, you should treat the plan as a negotiable risk tool, not a blanket promise. BatchData's own guide to buying a house with a home warranty is useful for that stage because it frames the warranty as part of due diligence, not just a closing freebie.

A warranty can make a transaction feel safer while still leaving the buyer exposed on exclusions, caps, and contractor control.

That's why the first analytical step isn't “Which company is cheapest?” It's “Which systems in this house are old enough to matter, and are they the kinds of failures this contract pays for?”

How Much Does a Home Warranty Actually Cost?

Advertised pricing understates the decision. The premium is only the fixed cost of entry. The full number includes service fees on each claim, optional coverage for items the base plan excludes, and the risk that a paid claim still leaves part of the bill with the homeowner.

A useful way to price a warranty is to separate fixed costs from claim-driven costs.

| Cost layer | Typical structure | Why it matters |

|---|---|---|

| Base premium | Annual or monthly contract charge | You pay it whether you file a claim or not |

| Service fee | Charged each time a technician is dispatched | Every claim increases your annual spend |

| Add-ons | Extra charge for pools, spas, well pumps, second refrigerators, and similar items | The quoted price often excludes the items owners care about most |

| Coverage limits and exclusions | Contract terms, not headline pricing | A low premium can still produce a high out-of-pocket bill |

Calculating the full cost

The number that matters is total annual outlay, not the monthly teaser rate in the ad.

Start with the annual premium. Add the service fee multiplied by the number of claims you realistically expect to file. Then ask a harder question that marketing pages usually avoid: if a covered item fails, how much of that repair or replacement cost would the contract absorb after caps, exclusions, and denied components?

That last piece changes the math. A warranty with a moderate premium can still be expensive if the claim process produces partial approvals or repeated service fees without a full fix.

How usage changes the economics

The break-even point moves with claim volume and claim size.

A homeowner who files no claims bought budget stability and received no direct repair value that year. A homeowner who files one small claim may still spend close to, or more than, the cost of paying for that repair without a contract. The economics improve only when the plan pays for enough covered work to offset the premium and the claim fees.

That is why warranties tend to look better on older rental stock with several aging systems than on homes with newer equipment. Owners comparing this choice for tenants should review how a home warranty for rental property affects both repair budgeting and contractor control, because those trade-offs matter as much as the headline price.

Why sticker price is the wrong comparison

Monthly affordability is mostly a sales frame. The financial comparison is broader.

If the likely claims are minor appliance repairs, the contract can be a poor value because the premium and service fees consume a large share of the expected benefit. If the concern is a higher-cost failure on a covered system, the contract may make sense for a limited period, especially when cash reserves are thin. But that value often declines over time. Once the homeowner has rebuilt reserves, replaced older equipment, or learned that the contract excludes the failures they face, the warranty can shift from risk management tool to recurring overhead.

The decision is less about peace of mind than about expected payout versus total annual spend. That is the number to test.

Who Actually Benefits from a Home Warranty?

A home warranty makes the most financial sense when expected annual repair costs on covered systems are likely to exceed the contract's premium plus service fees.

That framework comes directly from FBFS guidance on whether home warranties are worth it, which notes that annual premiums commonly run about $500 to $900, while service fees often add $50 to $150 per claim. The same guidance is clear about the best-fit profile: older homes and households without enough liquid savings to self-insure.

The best-fit homeowner profiles

Different owners buy the same product for different reasons. The logic isn't identical.

| Homeowner type | Why a warranty can make sense | Why it may not |

|---|---|---|

| First-time buyer | Preserves cash after closing and reduces first-year repair shock | Weak value if systems are newer or still under manufacturer coverage |

| Owner of an older home | Transfers some risk from aging HVAC, plumbing, or appliances into a known annual cost | Exclusions can matter more as systems age |

| Landlord | Creates a more predictable repair budget and can simplify vendor coordination | Less attractive if speed, contractor choice, and unit turnover timing matter more |

| Seller | Can reduce buyer hesitation as a transaction tool | Doesn't change the physical condition of the systems |

First-time buyers with thin reserves

This is one of the strongest use cases.

A buyer may have enough cash to close but not enough extra liquidity to absorb a sudden mechanical failure comfortably. In that situation, the warranty isn't an investment. It's a cash-flow stabilizer. That can be rational even if the expected long-run value is imperfect.

Owners of older homes

This is the second strong use case.

If several major systems are already well along in their life cycle, failure risk becomes more concentrated. You're not buying certainty that the company will fully pay. You're buying a contract that may absorb part of the shock if the breakdown falls within coverage rules.

Rental property owners

Landlords often care about predictability and coordination more than perfect economic efficiency on any single claim. That makes the product easier to justify in some portfolios, especially when the owner wants to reduce maintenance administration. For a transaction-focused view, BatchData's home warranty for rental property guide frames where that tradeoff can fit within a rental operating model.

If your main problem is “I can't handle a surprise bill right now,” a warranty can solve a real problem even when it doesn't maximize value.

Who usually shouldn't buy one

Some owners are poor candidates:

- Owners of newer homes: manufacturer warranties often do the job first.

- Households with strong repair reserves: they can self-insure and keep contractor control.

- Owners who replace low-cost appliances quickly: service fees and friction can outweigh benefits.

That's the hidden point many articles miss. A home warranty isn't “good” or “bad.” It's capital structure for household repairs. If you have cash and want control, self-insurance is often cleaner. If you don't, risk transfer can be worth paying for.

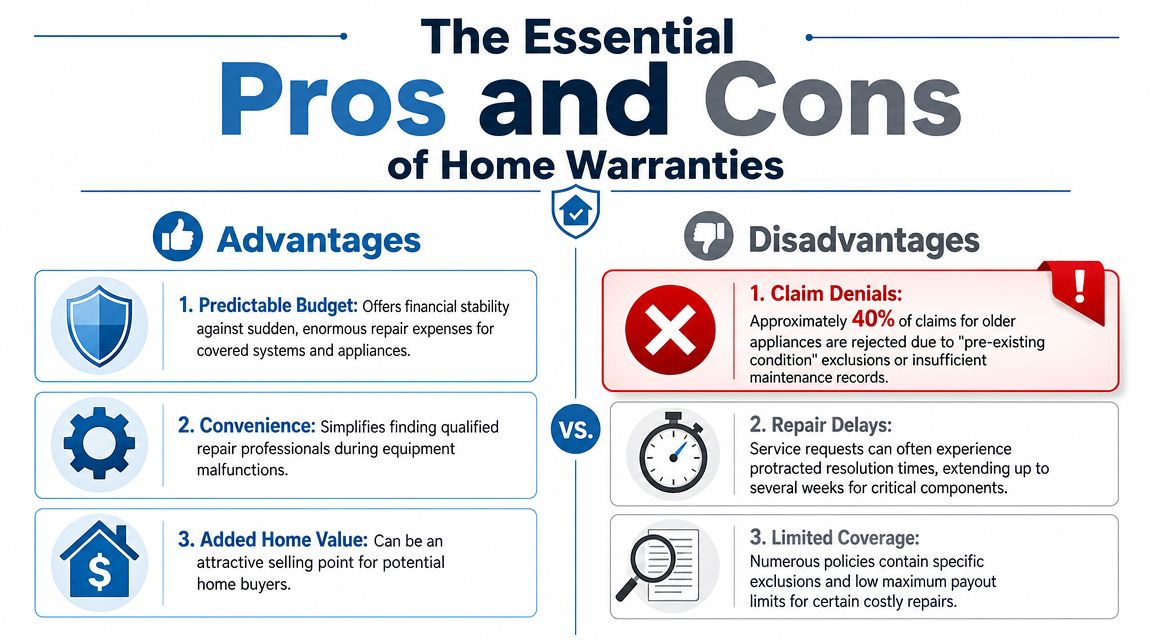

What Are the Real Pros and Cons?

The main benefit of a home warranty is cost predictability. The main hidden cost is loss of control.

That second point gets glossed over constantly. According to Call Mattioni's discussion of home warranty tradeoffs, the homeowner usually can't choose the contractor and must accept the warranty company's assigned technician. That matters because speed, workmanship, parts availability, and the repair-versus-replace decision affect the outcome more than marketing copy does.

Side-by-side tradeoffs

| Dimension | Potential advantage | Real drawback |

|---|---|---|

| Budgeting | More predictable annual repair spending | Premium plus service fees can still be expensive |

| Convenience | One place to submit service requests | You often lose contractor choice |

| Claims | Some expensive failures may be partially offset | Exclusions, caps, and denials can limit value |

| Home sale | Can help reassure buyers in a transaction | Doesn't fix old equipment or change deferred maintenance |

The upside is real, but narrow

Some homeowners do get real utility from these plans.

- Budget stability: a surprise repair becomes easier to absorb when annual costs are partly fixed.

- Administrative convenience: the company handles dispatch rather than the homeowner searching for a vendor.

- Transaction support: sellers sometimes use a warranty to calm buyers after inspection.

The downside is where most buyers misprice the product

The non-financial costs are substantial.

- Contractor control is limited. If you already have a trusted HVAC or plumbing company, the warranty can force a different process.

- Approvals can slow the repair cycle. That may be tolerable for a dishwasher, less so for heat, cooling, or active leaks.

- Repair quality decisions may not align with your priorities. A warranty company may approve a repair where you would prefer replacement.

For roof-related damage, buyers also need to separate warranty logic from insurance logic. A practical reference is this explainer on when roof damage is covered by insurance, because roof failure often belongs in the insurance analysis, not the home warranty analysis.

A warranty works best for owners who value predictable process over maximum choice. If you care most about speed and picking your own contractor, the trade may feel bad even when the claim is technically covered.

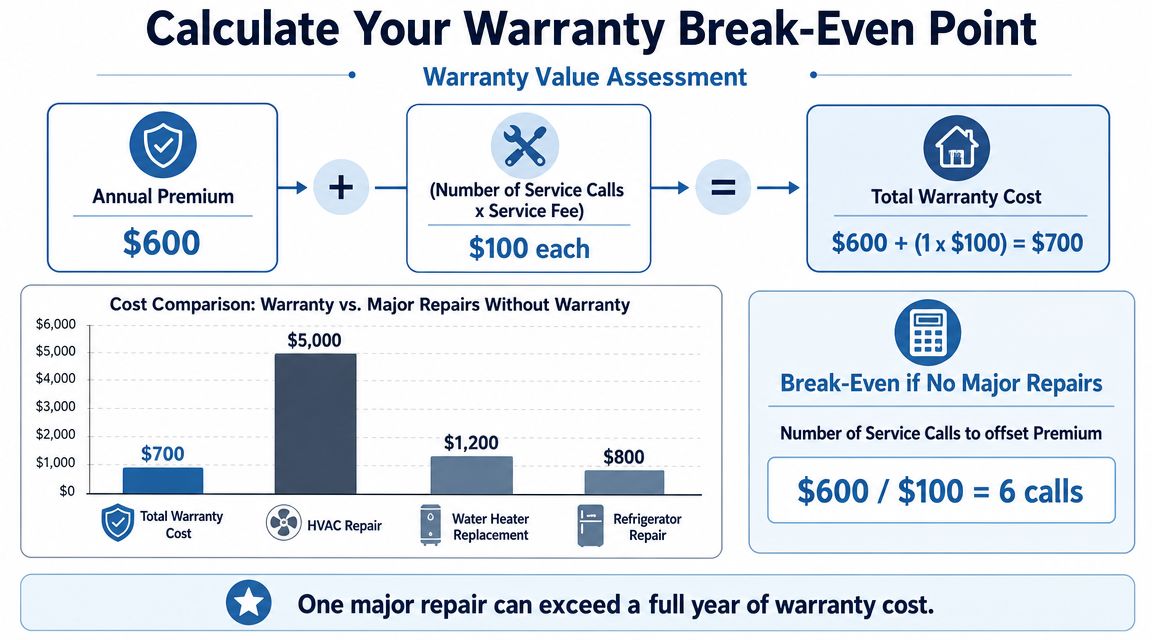

How to Calculate the Break-Even Point

A home warranty is worth it when your expected covered repair cost is higher than your premium plus expected service fees.

That sounds obvious, but the important wrinkle is that the calculation changes as systems age. According to First American's discussion of when coverage stops working well, home warranties are typically one-year contracts and often exclude failures tied to lack of maintenance, rust, or corrosion. It also notes that service fees often run about $65 to $150 per claim. So the break-even question isn't static. It shifts as equipment gets older and denial risk rises.

Use this formula

Break-even test:

Annual premium + (expected claims × service fee)

versus

expected out-of-pocket cost for covered repairs

That's the whole model.

How to apply it in real life

- List the major systems and appliances. Focus on HVAC, plumbing, electrical, water heater, and kitchen appliances.

- Estimate which items are old enough to worry about. Older equipment raises failure risk, but it can also raise exclusion risk.

- Assign likely claim count. Be conservative. More claims mean more service fees.

- Stress-test exclusions. If the item has maintenance issues, corrosion, or mismatch concerns, discount your expected payout value.

- Compare against self-insuring. If your likely out-of-pocket cost still looks manageable, the warranty may not add much.

The video below shows the kind of consumer decision process many homeowners struggle with.

When the math gets worse over time

A lot of owners assume an aging house automatically makes a warranty more valuable forever. That's incomplete.

Older systems do raise breakdown risk. But they also raise the odds that the contract points to maintenance exclusions, rust, corrosion, or other condition-based reasons to narrow payment. In other words, the same aging process that makes you want protection can also make the protection less reliable.

The break-even point isn't just about failure probability. It's also about the probability that the contract says no when the failure finally happens.

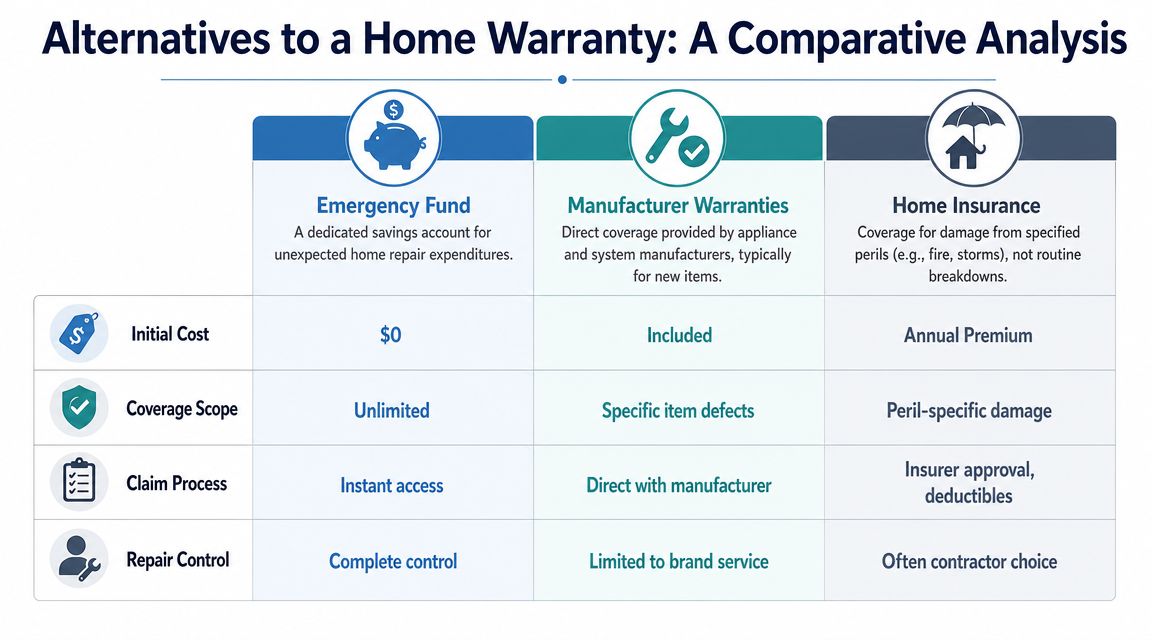

What Are the Alternatives to a Home Warranty?

The main alternatives are self-insuring with a repair fund, relying on manufacturer warranties for newer items, and using homeowners insurance for peril-driven losses.

Those options solve different problems, and they offer different levels of control.

Best alternatives compared

| Option | Initial cost | Coverage scope | Claim process | Repair control |

|---|---|---|---|---|

| Emergency fund | $0 to start beyond your own savings discipline | Broad because your cash can pay for any repair | Immediate access to your own funds | Complete control |

| Manufacturer warranties | Often included with new items | Narrow to specific defects and covered periods | Direct with manufacturer | Often limited to authorized service |

| Homeowners insurance | Annual premium | Peril-based damage, not routine wear-and-tear breakdown | Insurer approval and deductibles | Often more contractor flexibility than a home warranty |

| Home warranty | Annual premium plus service fees | Covered systems and appliances, subject to exclusions and caps | Warranty company dispatch and approval | Usually limited contractor choice |

Emergency fund versus warranty

This is the purest comparison.

An emergency fund gives you full flexibility. You choose the contractor, the timing, and whether to repair or replace. There's no service fee and no argument over wear-and-tear language. The drawback is obvious. You need liquid cash and the discipline to leave it untouched.

Manufacturer coverage versus warranty

For newer homes and recently installed systems, manufacturer coverage often makes third-party warranty coverage less compelling. If the item is already protected by the maker's own terms, layering another contract on top may add less value than buyers think.

Insurance versus warranty

These products get mixed together constantly, and that leads to bad decisions. Insurance covers damage from specific events. It doesn't generally cover the ordinary mechanical failure that home warranties target.

If you're evaluating a storm-related or roof-related issue, an insurance-specific resource is more helpful than a warranty pitch. Four Seasons Roofing's claims guide for roof insurance is the kind of reference that helps separate peril claims from routine breakdown questions.

Which alternative fits which owner

- Cash-strong owner: emergency fund is usually the cleanest option.

- Owner of newer systems: manufacturer coverage often handles the immediate risk window.

- Owner worried about disasters: homeowners insurance is the relevant tool.

- Owner needing predictable routine-repair budgeting: warranty may still fit.

The deeper point is that a home warranty is only one method of handling repair risk. It's often not the most efficient one. It's the one that converts uncertainty into a recurring bill.

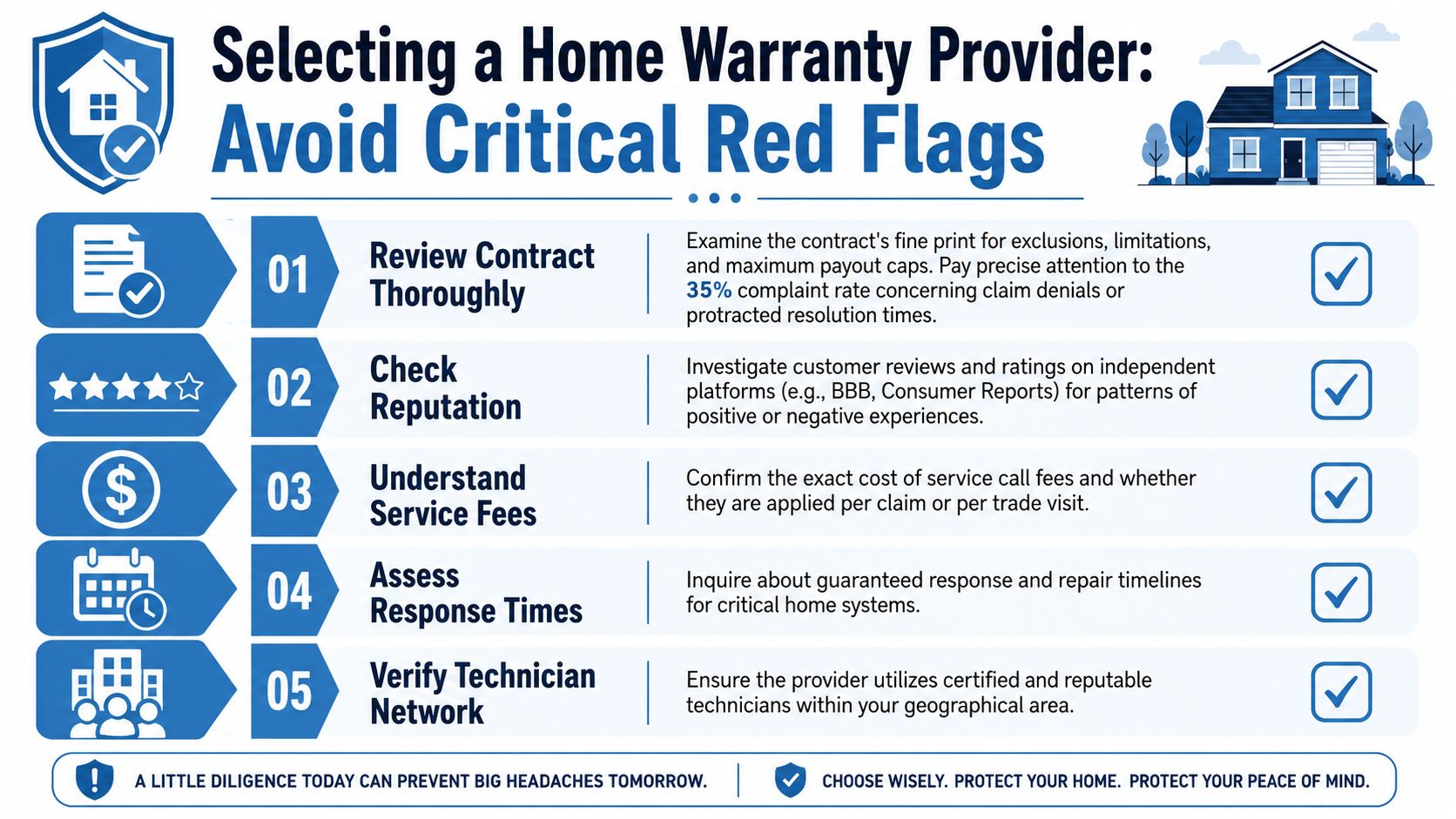

How to Choose a Provider and Avoid Red Flags

A low monthly premium often distracts buyers from the fundamental underwriting question: how much of a repair bill the contract will ultimately absorb once exclusions, service fees, and payout caps apply. Provider selection matters because the value of a home warranty is determined less by the brochure price than by claim approval standards and contract limits.

The practical test is simple. If a provider caps reimbursement well below the replacement cost of your highest-risk system, the contract stops functioning as meaningful risk transfer and starts functioning as a partial discount plan. That distinction matters most for older HVAC systems, electrical work, and plumbing failures, where labor and code-compliance costs can push total bills far above what marketing summaries imply.

Ask these questions before you sign

- Coverage caps: What is the maximum payout for each system and appliance, and is there also an annual aggregate limit?

- Denial triggers: How does the contract define pre-existing conditions, improper installation, maintenance failure, rust, corrosion, or code violations?

- Repair versus replacement: Who makes that call, and what happens if the proposed fix is temporary but replacement is the economically rational option?

- Service fee mechanics: Is the fee charged per claim, per contractor visit, or each time a different trade is dispatched?

- Technician network: How large is the local network, what are average response times, and can you use your own licensed contractor if the company cannot place one promptly?

Read the sample contract before you compare brands. If the company will not provide one up front, treat that as a screening failure.

Red flags that should stop you

- Vague exclusions: Broad phrases like “not properly maintained” can be used to deny routine claims after the fact.

- Thin disclosure on limits: If caps, waiting periods, and excluded components are hard to find, expect friction at claim time.

- Complaint patterns focused on delays or repeat dispatch fees: A cheap contract gets expensive if one breakdown triggers multiple paid visits.

- Sales language centered on budget predictability without equal detail on denial standards: That usually signals weak transparency where it matters most.

If you are evaluating a property before closing, a warranty should sit behind inspection and condition analysis, not replace them. A practical real estate due diligence checklist helps frame that sequence, because the better you understand system age, permit history, and deferred maintenance, the easier it is to judge whether a warranty has positive expected value or is just masking known risk.

For investors and operators reviewing homes at scale, BatchData provides property records, ownership history, permits, valuations, and related housing data that can help estimate condition risk before a warranty is used as a repair-budget tool.