SEO Title: Title Commitment vs Title Policy Explained Clearly

Meta Description: Learn the practical difference between a title commitment and a title policy, including schedules, risk signals, and workflow impact.

Meta Keywords: title commitment vs title policy, title commitment, title policy, title insurance, Schedule A Schedule B Schedule C, real estate closing, title defects, proptech title workflow

Confusing a title commitment with a title policy creates real risk because one is only a promise to insure and the other is the actual protection that starts after closing.

For operators, lenders, and proptech teams, that distinction changes how you review documents, route tasks, and decide when a file is safe to fund. The commitment is a pre-closing decision tool. The policy is the post-closing risk transfer instrument. Treating them as interchangeable is how teams miss curative work, misunderstand exceptions, and automate the wrong step.

| Document | When it appears | What it does | What your team should do |

|---|---|---|---|

| Title commitment | Before closing | Commits the insurer to issue coverage if listed conditions are met | Review every schedule, clear requirements, and escalate exceptions |

| Title policy | After closing | Provides the final insurance contract for covered title defects | Store, track, and match coverage to ownership or loan position |

| Operational meaning | Pre-funding | Workflow driver | Use for issue detection, task routing, and closing readiness |

| Risk meaning | Post-funding | Indemnity protection | Use for claims handling and long-tail file governance |

A good closing team reads the commitment as a live defect list, not a formality. If your transaction also involves probate or inherited property questions, understanding how muniment of title works helps explain why some ownership chains need specialized curative review before a title insurer will move to policy. Market context matters too, especially when acquisition teams are prioritizing regions with changing investor activity such as those tracked in the Investor Pulse national report.

Introduction The Critical Difference Between a Promise and Protection

The shortest accurate answer in the title commitment vs title policy debate is this: the commitment tells you what must happen before insurance can be issued, and the policy is the insurance itself.

That sounds simple. In practice, it isn't. Teams lose time because they read the commitment like a finished product when it's really a conditional underwriting memo packaged for closing. Then they store the final policy without mapping its covered risks and exclusions to the loan, owner, or servicing record.

Quick distinction

| Feature | Title commitment | Title policy |

|---|---|---|

| Core role | Promise to issue insurance if conditions are satisfied | Final insurance contract |

| Transaction stage | Pre-closing | Post-closing |

| Main use | Identify requirements and exceptions | Indemnify against covered title defects |

| Primary users | Underwriting, escrow, legal, closing, lending ops | Owners, lenders, servicing, claims |

| Action type | Resolve issues | Rely on coverage |

A commitment is where the work is. A policy is where the protection is.

Practical rule: If your team is still fixing title problems, you're dealing with a commitment problem, not a policy problem.

That distinction drives every downstream workflow, from underwriting queues to exception management to post-close document retention.

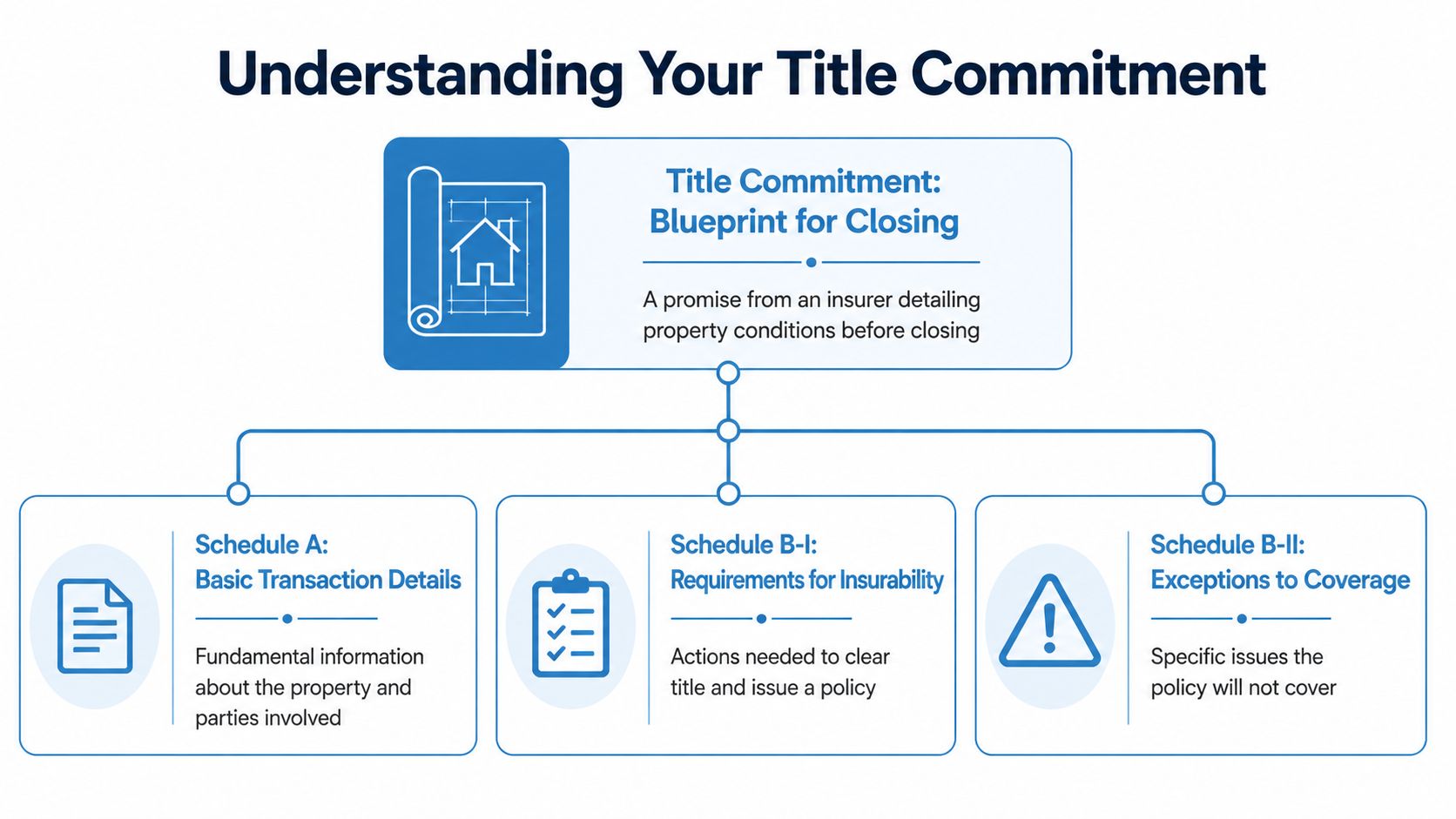

How to Read a Title Commitment

A title commitment is a legally binding promise by the title insurer to issue a final policy once the listed conditions are satisfied.

The document matters because it's structured for action. You don't read it for background. You read it to identify what blocks closing, what survives closing, and what your systems should flag for underwriting and legal review.

A practical title review starts with structure. Standard commitments are organized around schedules. Schedule A covers transaction basics. Schedule B handles exclusions, with B-I for actionable requirements and B-II for non-coverable exceptions such as easements. Schedule C lists prerequisites that must be satisfied before policy issuance. When teams parse those schedules against 155M+ property records, they can flag risks earlier, and handling exceptions before closing can reduce post-closing claims by 40-60% according to the ALTA-linked fact set provided here: ALTA data and statistics reference.

Schedule A holds the identity data

Schedule A tells you whether the file is even pointed at the right property and parties.

Look for these fields first:

- Effective date: This tells you when the commitment speaks. If recordings happen after that date, someone needs an update.

- Policy amount: This often matches the purchase price for the owner's side.

- Current owner: This must match record title.

- Proposed insured: This must match the buyer or borrowing entity exactly.

- Legal description: Bad automations often fail when processing this. Mailing address matches are not enough.

If you're building ingestion logic, don't let your parser rely on street address alone. Match the legal description, owner name, vesting pattern, and parcel-level identifiers where available. If those fields conflict, route the file to human review.

Schedule B-I is the work queue

B-I contains the requirements that must be completed before the insurer will issue the policy.

Expect to find payoff demands, unresolved liens, judgments, tax issues, affidavits, survey requirements, or entity authority documents. In operations terms, B-I isn't a disclosure section. It's a task list.

Use a rules layer that categorizes each requirement by owner:

- Seller-side curative items such as lien payoff or satisfaction.

- Buyer-side items such as entity formation documents or vesting confirmations.

- Lender-side conditions tied to funding or recording.

- Title-agent closing conditions such as updated searches or gap coverage procedures.

A lot of teams flatten B-I and Schedule C into one bucket. That's sloppy. You need separate statuses for "known requirement," "document ordered," "recordable," and "cleared."

Schedule B-II is where surviving risk lives

B-II lists exceptions that generally remain outside coverage unless they are removed or insured over through endorsements.

Typical examples include easements, restrictive covenants, rights-of-way, and other matters that run with the land. These aren't "to-do" items in the same way as payoff requirements. They are risk descriptors that should affect underwriting, valuation review, and, in some cases, product eligibility.

If your platform only extracts lien language and ignores B-II, it isn't doing title review. It's doing debt detection.

For international buyers comparing title systems, this essential guide for Dominican Republic property buyers is useful context because it shows how title-search expectations differ across jurisdictions. That contrast helps developers avoid hardcoding assumptions from U.S. commitment formats into broader real estate products.

Schedule C controls issuance

Schedule C is often the primary gating section because it states what must happen before the policy can be issued.

Read it as a closing readiness checklist. If a requirement in Schedule C isn't cleared, the policy doesn't exist yet. That means your lender shouldn't treat the file as fully insurable, and your automation shouldn't mark title as complete.

Schedule D explains who pays

Schedule D discloses premiums and how charges are allocated among parties.

For systems design, this matters less for legal risk and more for budgeting, settlement integrations, and fee transparency. It also helps reconciliation teams match expected title charges to closing disclosures and internal forecasts.

Understanding the Final Title Policy

A title policy is the final insurance contract delivered after closing. It indemnifies the insured against covered title defects tied to past events affecting the property.

That makes the policy distinctly different from the commitment. The commitment points to issues. The policy responds to covered loss.

Two policies usually matter

Most residential transactions involve two distinct protections:

- Owner's policy: Protects the buyer's ownership interest and equity.

- Lender's policy: Protects the lender's lien position and collateral interest.

They serve different insureds, which means your document management and compliance logic should store them separately. Don't assume the lender's policy protects the owner. It doesn't.

What the policy is meant to cover

The policy can protect against defects such as forgery, fraud, recording issues, and undisclosed heirs if those matters fall within coverage.

The point is long-tail protection. Problems can surface well after the deed records, and the policy exists for that scenario. According to the CFPB fact set provided here, title insurance premiums usually range from 0.5% to 1.0% of the purchase price, and that one-time premium protects against hidden title risks affecting an estimated 30-40% of properties as summarized in the CFPB closing disclosure guide.

What the policy does not fix

A policy doesn't clean up defects by itself. It also doesn't erase every exception carried over from the commitment.

That's why exception review before closing matters. If an easement, covenant, or other listed matter remains excepted, that risk can stay outside coverage unless an endorsement modifies the result.

A bad assumption at commitment stage becomes a permanent coverage problem at policy stage.

Why endorsements matter

Endorsements are where underwriting gets precise.

If the commitment identifies a risk that can be specifically addressed, an endorsement may expand or tailor coverage. For lenders and proptech teams, the operational point is straightforward: your system should track not only whether a policy issued, but which endorsements issued with it. Coverage quality isn't binary.

Title Commitment vs Title Policy The Key Distinctions

The direct comparison is below. This is the fastest way to frame the title commitment vs title policy question in operational terms.

| Feature | Title Commitment | Title Policy |

|---|---|---|

| Purpose | Promise to issue insurance if stated conditions are met | Final contract that provides coverage |

| Timing | Before closing | After closing |

| Legal status | Conditional undertaking | Active insurance protection |

| Key content | Schedules with transaction details, requirements, and exceptions | Insuring provisions, covered risks, exclusions, and endorsements |

| Primary audience | Closing teams, underwriters, lenders, attorneys, buyers | Owners, lenders, servicers, claims handlers |

| Lifespan | Temporary and transaction-specific | Lasts according to the insured interest and policy terms |

| Main question answered | What must be fixed or accepted before closing? | What loss is covered after closing? |

Why timing changes everything

The commitment is time-sensitive because it's part of a live file. If new recordings appear, payoff figures expire, or vesting changes, the commitment may need updating before close.

The policy isn't part of a live checklist. It's the settled insurance instrument for a closed transaction. That means your workflow should treat commitment review as active underwriting and policy review as record governance.

Why content differences matter to automation

Commitments are rich in structured signals. Policies are rich in contractual meaning.

If you're designing extraction models, the commitment is usually better for:

- Task creation

- Exception classification

- Clear-to-close logic

- Escalation routing

The policy is usually better for:

- Coverage verification

- Claims reference

- Post-close audit

- Loan boarding and servicing controls

The trade-off nobody should ignore

A team that over-focuses on the policy tends to react too late. A team that over-focuses on the commitment without preserving policy metadata loses visibility after close.

Good operations keep both. Great operations connect them.

How These Documents Impact Your Workflow

These documents affect different teams in different ways. Buyers need clarity. Lenders need certainty. Proptech teams need structured signals they can trust.

For buyers and investors

A buyer should treat the commitment as the last serious warning document before money moves.

Review points that deserve attention:

- Vesting accuracy: The buyer name or entity name must be right.

- Legal description match: Address-only review isn't enough.

- Requirements list: Any unresolved payoff or affidavit item can delay closing.

- Exceptions list: Easements and covenants may affect use, resale, or development plans.

Investors should go one step further and compare commitment exceptions against intended exit strategy. A rental hold, fix-and-flip, and small development project tolerate different levels of title complexity.

For mortgage lenders

Lenders care about whether title conditions support clean collateral.

A clean commitment shortens the path to final underwriting because it answers practical questions fast. Is the borrower vesting correctly? Is there a prior lien that must be released? Are there exceptions that impair marketability or lien priority? Those are lending questions as much as title questions.

From an operational perspective, lenders should map commitment fields to underwriting gates:

- Borrower and vesting match

- Property identity match

- Lien payoff confirmation

- Exception severity classification

- Policy type and endorsement requirements

Regional market behavior also affects file strategy. Teams pricing acquisition, refinance, or servicing opportunities in California often want broader state context alongside title data, which is why resources like the California Investor Pulse report can help frame where title review speed and certainty matter most.

Underwriting view: A commitment with unresolved title conditions is not a paperwork issue. It's a collateral issue.

For proptech and data teams

Most current guidance falls short at this point. It defines the documents but doesn't tell developers how to use them.

A practical parsing model should separate commitment content into at least four machine-readable buckets:

| Data bucket | Typical source in document | Workflow use |

|---|---|---|

| Identity data | Schedule A | Match owner, vesting, legal description, and property profile |

| Curative tasks | B-I and Schedule C | Create action queues and dependency chains |

| Persistent risks | B-II | Score risk and route for legal or underwriting review |

| Cost allocation | Schedule D | Reconcile title charges and settlement data |

Once extracted, those fields can be joined to property datasets, ownership records, mortgage history, lien data, and internal loan objects.

What works in real workflows

The best title-adjacent automations do three things well:

- Normalize text into issue classes. "Pay off," "release," "satisfaction," and "cancel of record" should not create four different issue types.

- Separate requirements from exceptions. Teams waste time when every title item gets treated as a curative defect.

- Track state transitions. Ordered, received, recordable, recorded, approved, closed. If your system jumps from open to complete, you'll lose files in the middle.

What doesn't work

A few patterns consistently fail:

- PDF-only storage: If nobody extracts fields, the commitment becomes an image archive.

- Address-only matching: This causes false confidence when legal descriptions or vesting differ.

- One-status workflow: "Title reviewed" tells nobody whether title is clear.

- No post-close linkage: If the policy isn't tied back to the commitment and issue log, future claims analysis gets weak fast.

Automating Exception Resolution and the Curative Process

Exception resolution is where title operations either become disciplined or become chaotic.

Most curative work starts with defects identified in the commitment. Common categories include liens, judgments, unpaid charges, authority issues, vesting mismatches, and land-use or access matters that require deeper legal review. Some issues are routine. Others need litigation or specialized counsel. For disputes involving ownership claims or partition, practitioners sometimes need resources like Kona Kealakekua Kamuela Quiet Title Partition Attorneys to understand the legal path when standard curative steps won't resolve the file.

The standard curative path

Classify the defect

Decide whether the issue is a payoff item, a recording issue, an identity problem, or a surviving land matter. Misclassification wastes days.Assign ownership

Some items belong to the seller, some to borrower counsel, some to the title/escrow team, and some to the lender.Order or collect documents

Releases, satisfactions, affidavits, entity documents, payoff letters, or updated surveys are common examples.Validate recordability

A signed release that can't be recorded is not a cleared item.Confirm title acceptance

The underwriter or title agent has to accept the cure. Internal confidence does not equal insurer approval.

Where automation actually helps

Automation is most useful before and during curative work, not after the fact.

Good systems can:

- Pre-screen likely defects by comparing ownership, lien, and mortgage data before the commitment is even ordered.

- Trigger task templates based on issue class so teams don't reinvent the same checklist every time.

- Detect stale conditions when a payoff, affidavit, or search update ages out.

- Surface dependency chains so teams know which unresolved item blocks issuance.

Digital workflow changes are accelerating this shift. According to the provided fact set summarizing recent industry developments, e-recording mandates in over 10 states since mid-2025 are cutting commitment-to-policy timelines from 10-15 days to 2-3 days, AI tools are starting to automate curative document generation for Schedule C items, and blockchain pilots show potential to reduce Schedule B exceptions by up to 40%, as described in this Forbes Technology Council article on AI and blockchain in title insurance.

What still requires human judgment

Not every title defect should be automated to resolution.

Use people for:

- Ambiguous vesting chains

- Probate-linked ownership breaks

- Boundary or access disputes

- Quiet title or partition matters

- Insurability decisions that depend on underwriting discretion

Fast automation is useful only when it preserves underwriting judgment. A wrong release processed faster is still wrong.

The goal isn't just speed. It's cleaner files, fewer reopenings, and better certainty about what the insurer will issue.

The Future of Title From Commitment to Instant Decision

The title process is moving away from linear document handling and toward data-driven decisioning.

That doesn't mean commitments or policies disappear. It means their contents become machine-readable inputs instead of static PDFs passed from inbox to inbox. Teams that still treat title as a manual exception process will keep operating on lagging information.

The next operating model

The likely direction is straightforward:

- Property data gets unified earlier

- Title risk gets scored before closing work starts

- Curative steps get routed automatically

- Underwriters review edge cases instead of every routine item

- Policies issue from cleaner, better-structured files

That future depends on high-quality source data. If ownership history, liens, legal descriptions, and valuation signals don't reconcile upstream, no amount of AI will make the title decision reliable. Geospatial context matters too, especially where parcel boundaries, access, and land-use overlays affect risk, which is why work like how geospatial analysis enhances automated valuation models is relevant to the broader underwriting stack.

What changes for practitioners

The underwriter's job doesn't disappear. It gets narrower and more important.

Routine defects should become easier to classify and cure. Hard files will still need judgment. The practical shift is that title teams will spend less time hunting for obvious issues and more time deciding whether a non-obvious issue is insurable.

What to build for now

If you're building systems around title commitment vs title policy, focus on these priorities:

| Build priority | Why it matters |

|---|---|

| Structured extraction | Commitments are only useful to software if schedules become usable fields |

| Issue taxonomy | Curative work collapses without consistent labels |

| State-aware rules | Recording and underwriting practices vary |

| Commitment-policy linkage | Post-close coverage should trace back to pre-close conditions |

| Human escalation design | Hard title problems still need specialist review |

The firms that win won't be the ones that read title faster. They'll be the ones that convert title data into better decisions before the rest of the market sees the risk.

BatchData helps real estate, lending, and insurance teams work from unified property, ownership, mortgage, and lien data instead of fragmented records. If you're building automated underwriting, due diligence, portfolio monitoring, or title-adjacent workflows, explore BatchData to see how a developer-friendly property data platform can support faster, cleaner decisions.