More title losses come from missed defects, uncured requirements, and stale searches than from exotic headline risks. That is why the title insurance commitment deserves underwriting-level attention the day it lands in the file.

The commitment tells the deal team what the insurer is prepared to cover, what must be cleared before policy issuance, and which matters will stay outside coverage unless someone negotiates a change. For buyers, lenders, and operators, that document sets the actual closing path. It also exposes where the path can break.

A strong review does more than read the PDF. It compares the commitment against current vesting, tax status, lien activity, legal description data, entity authority, and use restrictions. Manual review still matters, but it misses too much when teams treat exception review as a line-by-line clerical task instead of a live underwriting process. Data-enriched workflows now let title and transaction teams verify exceptions against recorded property data, flag requirement gaps earlier, and track curative items before they become closing delays.

| Core takeaway | Why it matters | Practical implication |

|---|---|---|

| Schedule A sets the insured deal terms | Errors in names, vesting, legal description, or policy amount can carry into closing documents and policy issuance | Match it to the contract, entity records, payoff structure, and the current chain of title |

| Schedule B-I is a curative list | Requirements are conditions to issuance, not suggestions | Assign each item to a responsible party, set a due date, and collect written proof of clearance |

| Schedule B-II defines retained risk | Exceptions can limit access, development, financing, or exit value | Evaluate whether the property can be used, financed, and resold subject to those matters |

| The commitment can go stale | New liens, updated taxes, bankruptcy filings, or recording gaps can appear before closing | Confirm whether the search date still works for your timeline and update title if the file drifts |

| Property data tools improve review quality | Cross-checking exceptions and requirements against live records reduces missed issues and speeds curative work | Teams using platforms such as BatchData can verify ownership, lien indicators, parcel data, and recording history faster than manual review alone |

The practical shift in the market is clear. Strong teams do not wait for the closing table to find out whether an exception is acceptable or a requirement is still open. They use property data platforms to test the commitment against current records early, resolve curative work in parallel, and give underwriting a cleaner file before documents are drawn.

Why Your Title Commitment Is a Ticking Clock

A meaningful share of title defects surface late enough to disrupt pricing, financing, or closing logistics. That is why a title insurance commitment should be treated like a dated underwriting file, not a document you read once and park in the folder.

The clock starts on the commitment's effective date. From that point on, every day creates exposure between the title search and the actual closing. New liens can record. Taxes can update. Entity authority can change. A payoff that worked last week can be wrong by the time wires go out.

The practical problem is not the form itself. The problem is drift. A file that sits for two or three weeks without active verification can carry stale assumptions into doc prep, lender approval, and settlement statements. By then, even a fixable issue becomes expensive because it affects people, timing, and money all at once.

Underwriters and experienced closing teams watch this gap closely. ALTA's 2021 Commitment for Title Insurance form standardizes how commitments are presented, but it does not freeze the public record or reduce the need for updated verification. ALTA publishes the current commitment forms and endorsements at https://www.alta.org/policies-and-standards/title-insurance-forms/, and the form structure makes the point clearly: coverage is conditioned on facts that can change before issuance.

Practical rule: A title insurance commitment is only as reliable as its effective date and the team's proof that open items are still accurate.

Strong teams do four things early:

- Check staleness first. If the effective date is aging and the closing timeline has slipped, order an update before the problem reaches funding.

- Assign every requirement. Releases, payoffs, probate items, entity documents, and corrective deeds need a named owner and a hard deadline.

- Test exceptions against the actual deal. Access, use restrictions, recorded easements, and mineral reservations can change lender appetite and resale value.

- Verify against live property data. Public records, parcel history, ownership signals, and lien indicators should be cross-checked while curative work is still manageable.

Manual review alone is slow for this job. Teams that use property data and investor activity reports can compare the commitment against current ownership, recording activity, and market behavior before the file goes stale. That changes the workflow from reactive cleanup to proactive underwriting.

A good review does more than avoid a bad closing. It tells you, early enough to matter, whether the current structure still works.

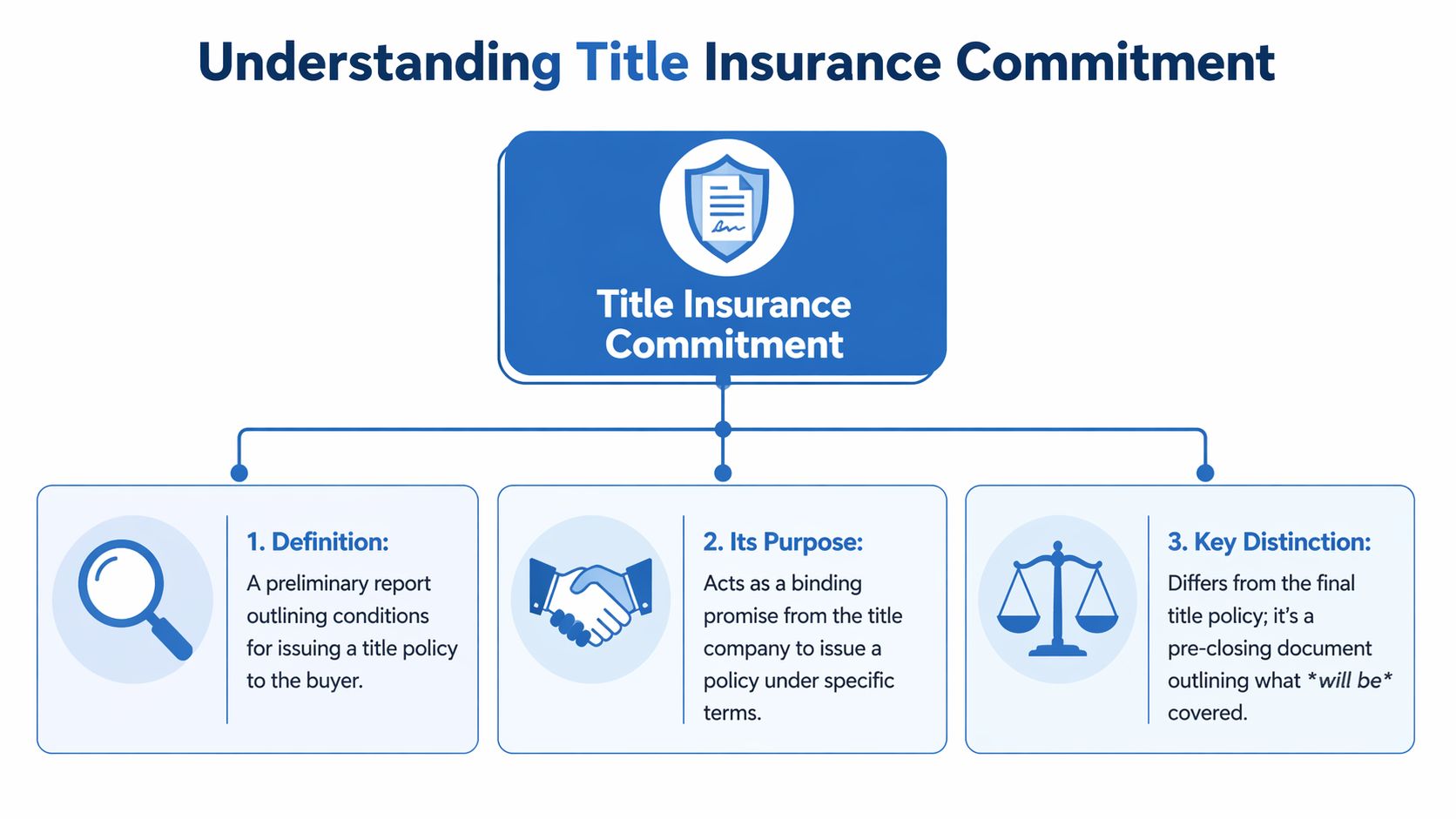

What Is a Title Insurance Commitment?

Analysts at the American Land Title Association report that title professionals conduct tens of millions of title searches each year. The commitment is the document that turns that search work into an underwriting position, with stated conditions, stated exceptions, and a clear line between what will be insured and what will not. See ALTA's industry overview at https://www.alta.org/learn/industry-overview.cfm.

A title insurance commitment is the title company's written agreement to issue a policy if the listed requirements are satisfied and the risk profile does not change before issuance. For a buyer, lender, or acquisition team, that means one thing: the deal is only insurable on the terms shown in the commitment.

What the commitment actually does

A commitment is the underwriter's conditional file memo in public-facing form. It identifies the proposed insureds, the land, the policy amount, the requirements that must be cleared before issuance, and the matters that will stay outside coverage unless changed by endorsement or curative work.

In practice, it does five jobs at once:

- Names the insured parties: Buyer, lender, or both

- Defines the insured land: By legal description, not mailing address

- States the proposed policy amount: Based on the transaction structure

- Lists pre-issuance requirements: Payoffs, releases, authority documents, corrective instruments, tax matters, and recording steps

- Lists exceptions to coverage: Easements, restrictions, reservations, access issues, survey matters, and other recorded or standard exceptions

That is why experienced real estate teams treat the commitment as an operating document, not a formality. It controls curative work, closing instructions, lender conditions, and post-closing claim risk.

Why the ALTA form matters in actual underwriting

The current ALTA commitment form gives parties a common structure, but standardization does not remove judgment. The form tells everyone where to find the key underwriting decisions. It does not tell them whether the listed exceptions are acceptable for the asset, the loan, or the exit plan.

That distinction matters on real deals. A warehouse acquisition and a ground-up multifamily loan may use the same form, but the review standard is different. An access easement that is acceptable on a stabilized retail parcel may be a problem on a development site. A blanket utility easement may be tolerable for a cash buyer and unacceptable for a construction lender.

The stronger approach is to pair the form review with current property data. Teams using platforms such as BatchData can compare the commitment against ownership history, lien signals, parcel data, transfer activity, and related-recording patterns before closing. That shortens the time spent proving whether an exception is old, satisfied, misindexed, or still active. It also helps assign requirements faster because the file is being reviewed against current public-record signals, not just the original search package.

What a commitment is not

A lot of avoidable friction comes from treating the commitment as if it were the policy itself. The commitment is the insurer's present willingness to insure on stated terms. The final policy is the contract issued after the requirements are met and the closing documents are recorded as required.

| Document | What it means | What it does not mean |

|---|---|---|

| Title commitment | Conditional agreement to issue a policy on stated terms | Coverage is already in force or every issue has been accepted |

| Final title policy | Insurance contract issued after closing and satisfaction of conditions | The property has no title issues |

| Title search result | Raw public-record findings | Underwriting has approved the transaction |

One practical point is easy to miss. A clean-looking commitment can still hide real closing risk if the requirements are unresolved, the legal description is wrong, or the exceptions have not been checked against current property data. That is why modern underwriting is shifting away from static document review and toward live verification of exceptions and requirements before the file reaches the table.

How Do You Read and Interpret the Commitment Schedules?

Recording mistakes and unresolved title issues still derail closings every day. The commitment schedules show where those problems are sitting in the file. Read them correctly, and you can assign cure work early, verify exceptions against current property facts, and avoid bringing preventable risk to the table.

I read a commitment in three passes. First, confirm the transaction facts in Schedule A. Second, convert Schedule B-I into a requirement tracker with owners and due dates. Third, test every Schedule B-II exception against the actual asset, the business plan, and current public-record data. That last step is where manual review often falls short.

Schedule A

Schedule A is the underwriting snapshot. It tells you who is being insured, what estate or interest is being insured, the amount of coverage, the current record owner, and the legal description tied to the proposed policy.

Errors here are expensive because they travel through the rest of the file unnoticed. A wrong vesting name can force redraws. A bad legal description can create a recording rejection or insure the wrong land. A mismatch between the contract and the record owner can signal a deeper chain issue, authority problem, or pending transfer that has not been documented correctly.

Review Schedule A against the purchase contract, lender instructions, organizational documents, vesting deed, and survey. If the property is part of a larger tract, compare the legal description to the intended split, access rights, and tax parcel history. Teams using property intelligence tools can check parcel boundaries, ownership history, and related encumbrance patterns faster than a manual file review alone. That matters because a clean Schedule A on paper can still describe a transaction that does not match the dirt.

Key points to verify:

- Proposed insureds: Names, entity status, trust capacity, and vesting must match the closing documents.

- Policy amount: The amount should fit the purchase price, loan amount, or insured interest.

- Estate or interest: Fee simple, leasehold, easement, or another insurable interest must be stated correctly.

- Current record owner: Any mismatch needs explanation before documents are signed.

- Legal description: Compare it to the survey, prior deed, and parcel mapping, not just the situs address.

Schedule B-I

Schedule B-I is the clearance file. These are the conditions the insurer requires before issuing the policy. If a listed item is not cleared, waived, or satisfied to the underwriter's standards, the commitment has not matured into an insurable closing.

Common requirements include mortgage payoffs, lien releases, judgment satisfactions, entity authority documents, death certificates, probate filings, corrective deeds, gap indemnities, and recording of the new deed or security instrument. Every item needs documentary proof. Verbal assurance from a borrower, broker, or payoff lender is not enough.

The practical mistake is treating B-I as an administrative checklist. It is an underwriting checklist. That distinction affects how files should be managed. A payoff letter has to match the encumbered party and collateral. A release has to be recordable in the correct county and indexed against the right name. A corrective deed has to fix the actual defect, not just create a cleaner looking chain.

Good teams assign each requirement to an owner, a document source, and a verification method. Better teams use data to pretest whether the item is still active before they start chasing paper. BatchData-style workflows help by surfacing lien, ownership, parcel, and recording signals that let staff identify stale exceptions, likely satisfactions, and cross-parcel issues before the closer is waiting on a release. The same location intelligence that supports geospatial analysis for automated valuation models also helps title operations verify whether an easement, access point, or parcel configuration in the commitment still matches current reality.

A simple rule improves file discipline: mark a B-I item complete only after the title company accepts the evidence and confirms the item can be removed or satisfied.

Schedule B-II

Schedule B-II lists the exceptions that will remain outside coverage unless the insurer agrees to remove them, insure over them, or modify them by endorsement. At this point, title review turns into asset review.

An access easement may be acceptable for a stabilized industrial parcel and unacceptable for a redevelopment site that needs truck circulation. A declaration of covenants may be routine for a retail condo and a serious problem for signage, parking allocation, or operating hours. A reservation of mineral rights may be tolerable for one lender and a credit issue for another. The text of the exception matters, but so does the planned use.

Read each exception with four questions in mind:

- Does it affect access, buildability, parking, utilities, or subdivision potential?

- Does it conflict with the purchase contract, survey, zoning assumptions, or site plan?

- Can it be removed, narrowed, subordinated, or covered by endorsement?

- Has anyone verified that the exception is correctly indexed, still active, and tied to the insured parcel?

That fourth question gets missed. In practice, some listed exceptions are overbroad, already terminated, misindexed, or attached to related land rather than the insured parcel. A manual reader may not catch that without pulling surrounding records, parcel maps, and chain data. Data-enriched review shortens that process. It also gives underwriting a factual basis to ask for curative documents, survey updates, or endorsement support earlier in the file.

For firms building a more modern review stack, the broader market for best legal tech tools is relevant, but title teams need tools built around parcel history, recording data, ownership changes, and encumbrance validation, not just document storage or generic workflow.

Title Commitment Schedules at a Glance

| Schedule | What it does | What you should verify |

|---|---|---|

| Schedule A | States the transaction facts the insurer is relying on | Proposed insureds, record owner, estate or interest, policy amount, legal description |

| Schedule B-I | Lists requirements that must be satisfied before policy issuance | Payoffs, releases, authority documents, corrective instruments, tax and judgment clearance, recording items |

| Schedule B-II | Lists exceptions that remain outside coverage | Easements, restrictions, declarations, reservations, survey matters, other recorded encumbrances |

What strong review looks like

Strong review produces work product, not margin notes.

Schedule A should become a verified transaction summary. Schedule B-I should become a cure log with responsibility, status, and documentary proof. Schedule B-II should become a risk memo that ties each exception to use, financing, survey, and endorsement strategy. If your team is only reading the commitment and not building those outputs, the file is being reviewed passively instead of underwritten actively.

What Are the Most Common and Costly Pitfalls?

According to the American Land Title Association, title problems that delay or derail closing often come from unpaid liens, recording defects, unknown heirs, and errors in the public record, not exotic edge cases. The costly mistakes are ordinary file issues that no one pinned to a person, a deadline, and a recorded cure.

The first pitfall is treating the commitment as a disclosure packet instead of an underwriting work order. A requirement is not satisfied because someone said the payoff is in process. An exception is not acceptable because it appears in every other file. Title turns on recorded facts, priority, and use impact.

Three problem areas account for a large share of avoidable loss and delay.

1. Exceptions reviewed for form, not for use

A recorded easement, access reservation, declaration, or mineral reservation may be standard in title practice and still be material to the deal. The question is not whether the exception looks familiar. The question is whether it interferes with the buyer's intended use, the lender's collateral position, or the endorsement package.

I see this most often with redevelopment sites and infill assets. The legal team reads the exception. The business team underwrites the site plan. No one puts the two together until survey, zoning, or construction counsel flags the conflict.

That is too late.

A stronger file ties each B-II exception to a concrete business issue:

- buildable area

- legal access

- parking and circulation

- signage rights

- utility placement

- future assemblage plans

- lender endorsement availability

If your team invests in markets with fast-changing parcel activity, county-level trend reporting helps frame where exception review tends to get harder. BatchData's California InvestorPulse market report is useful for seeing how transaction volume and investor concentration can increase the pressure on title and closing operations in active counties.

2. Payoff handled, release ignored

This is the most common operational mistake in closings with debt, judgment, HOA, tax, or UCC-related cleanup. Money moves. Everyone relaxes. The lien remains in the record.

Underwriting does not rely on verbal confirmation that an obligation was paid. It relies on recordable proof that the encumbrance was released, satisfied, terminated, or subordinated in the form required by local practice and the insurer's guidelines.

A payoff resolves the debt. A recorded release resolves the title issue.

That distinction matters in warehouse lines, resale timelines, and refinance transactions. A stale unreleased lien can block funding, prevent a downstream sale, or force an indemnity discussion that should never have been necessary.

This is a useful explainer for teams that need a visual refresher before they start reviewing commitment problems in volume:

3. Static review in a moving record system

The commitment reflects title as of its effective date. The transaction keeps moving after that date. Judgments get entered. Taxes update. New deeds record. Borrowers change entity structure. A missing probate fact surfaces. If the file is not refreshed, the team may be clearing yesterday's title against tomorrow's closing.

In higher-volume operations, manual review starts to break down. Someone has to check owner matches, lien status, open taxes, recording gaps, and parcel-level changes across multiple systems. If that work happens only at the beginning of the file, blind spots are predictable.

Data-enriched review improves this in a practical way. Platforms such as BatchData let teams cross-check ownership history, lien indicators, transfers, mailing data, and parcel attributes against the commitment so B-I items and B-II exceptions can be tested continuously instead of read once. That does not replace underwriting judgment. It gives the underwriter better inputs earlier, and it helps closing teams prove that a requirement was fulfilled.

The files that become claims or post-closing cleanup projects usually show the same warning signs:

- Schedule A parties do not match the vesting deed or signing authority documents

- payoff letters are in hand, but no release path is tracked to recording

- exceptions were accepted without mapping them against survey or planned use

- taxes, municipal items, or judgment searches were not refreshed before funding

- legal description issues were spotted, but no corrective instrument was assigned

The expensive title problems are usually visible. The failure is operational. No one verified the exception against current property data, no one owned the cure, and no one confirmed the record was clear at the point money went out.

How Can You Streamline Commitment Review with Data?

You streamline commitment review by turning the document into a verification workflow, not a reading exercise. Manual review alone is too slow for modern pipelines, especially when your team is touching multiple counties, counterparties, and closing calendars at once.

The gap in most title guidance is obvious. Standard explanations tell people to read Schedules A, B-I, and B-II carefully, but they stop there. First Alliance Title's discussion of title commitment review and property data integration points to a more useful model: API access to 155M+ U.S. property records can automate commitment cross-checks, data-enriched underwriting can reduce closing delays by up to 30%, and API-driven title services rose 22% over the last 12 months.

What data-assisted review looks like

A modern workflow maps commitment fields and exceptions against live property data. The goal isn't to replace title counsel or underwriting judgment. The goal is to remove avoidable blind spots.

Here is what that means in practice:

| Commitment item | Data cross-check | Why it helps |

|---|---|---|

| Current owner in Schedule A | Ownership history and vesting records | Flags chain mismatches before docs are drafted |

| Mortgage payoff requirement in B-I | Recorded mortgage details and lien records | Confirms whether the listed debt matches public encumbrances |

| Exception package in B-II | Permit, lien, ownership, and parcel-related records | Helps surface whether the exception conflicts with actual use or redevelopment plans |

Where manual review still fails

Manual review breaks down in three places.

First, teams don't review at the same level every time. One officer reads the easement language closely. Another assumes it's standard. That inconsistency creates avoidable risk.

Second, title review often happens in a silo. The title unit has one document set. Asset management, servicing, or acquisitions has another. Data systems can force one reconciled view.

Third, stale assumptions survive too long. If a commitment says one thing and current property records suggest another, a system should flag the mismatch before funding, not after an exception dispute.

Operational insight: Good underwriting now depends on both document interpretation and data reconciliation. If you're doing only one, you're accepting preventable exposure.

For legal and compliance teams designing that workflow, broader stacks matter too. A practical reference point is this guide to best legal tech tools, especially if your organization is trying to connect document review, intake, and audit trails instead of treating title as a standalone process.

The advantage for valuation and portfolio decisions

Title review also affects pricing and valuation discipline. An unresolved access issue, restrictive covenant, or lingering lien is not just a legal footnote. It changes the reliability of collateral assumptions and automated valuation outputs.

That is why geospatial and parcel-level context should sit next to commitment review. For teams thinking about how title risk intersects with collateral modeling, this overview of how geospatial analysis enhances automated valuation models is a useful companion read.

The old workflow was reactive. Read the commitment, wait for questions, and fix problems one at a time. The stronger workflow is proactive. Parse the document, cross-check the facts, flag discrepancies early, and push only clean files toward closing.

What Is the Timeline for a Title Commitment?

A delayed file can turn a valid commitment into stale underwriting. The timeline matters because a commitment reflects title conditions as of a stated effective date, not indefinitely. Every day between issuance and closing creates an opportunity for a new lien, a bankruptcy filing, a boundary issue, or a party change that the original search did not capture.

The practical timeline starts once the order is opened and the examiner has enough information to search title and prepare the commitment. In a clean residential file, issuance can happen quickly. In a commercial deal, trust transfer, probate, or multi-parcel assembly, the commitment may take longer because the title plant work and document review take longer. Speed is useful, but accuracy controls the risk.

Issuance and initial review

Once the commitment is issued, the clock is running. Schedule A should be checked the same day. If the vesting, legal description, insured amount, or proposed parties are wrong, the cure process starts from bad inputs.

Schedule B-I should also be turned into a task list immediately. Requirements do not clear themselves. Payoffs need current figures, entity documents need review, satisfactions may need to be recorded, and survey matters may need underwriting approval or revision before closing can stay on track.

Manual review still has a place, but it is no longer enough on its own. Teams using property data platforms such as BatchData can compare ownership, parcel, transaction, and lien signals against the commitment early in the file, which helps identify mismatches before they become closing-day surprises.

Cure period and pre-closing control

The middle of the timeline is where title operations either stay disciplined or drift. This is the period for collecting releases, resolving judgment issues, correcting vesting, confirming tax status, and making sure the closing package satisfies each requirement the commitment sets out.

A commitment is a conditional underwriting position. The policy issues only after those conditions are met and the final gap review supports recording. If the file sits too long, counsel should ask a simple question: is the commitment still current enough to insure this closing, on this date, with these parties and these documents?

Many underwriters also place a time limit on the commitment itself. The American Land Title Association's model commitment form states that the commitment is invalid after the date shown in its Conditions unless the company extends it in writing, as reflected in ALTA commitment materials at alta.org. The exact period depends on the form and local practice, so the safer approach is to diary the effective date, the stated expiration terms, and any required update point at opening.

When you need an update

An updated commitment is usually required when closing is delayed, the transaction structure changes, a new deed or loan is introduced, or someone has reason to suspect an intervening matter. In practice, that includes seller entity changes, revised borrower names, added parcels, substitute trustees, new easement information, or a long gap between signing and funding.

When effectively applied, data improves underwriting judgment. A title team that waits for a party to report a problem is operating reactively. A title team that checks updated lien, transfer, tax, and parcel signals against the commitment before funding can catch issues while there is still time to cure them. For California teams dealing with uneven transaction velocity by county and asset type, BatchData's California Investor Pulse report on transaction tempo and market conditions helps explain why some files age out faster than others.

Ask whether the commitment still matches the file you are closing, not whether it matched the file when it was first issued.

A disciplined timeline

A reliable workflow follows this order:

- Open title as soon as the deal is live

- Review Schedule A and B-I immediately after issuance

- Assign each curative item to a specific owner with a deadline

- Recheck for changes before documents are signed

- Order an update or bringdown when timing or facts change

- Confirm title currency again before funding and recording

That sequence reduces avoidable risk. It also shifts title review from document reading alone to ongoing verification, which is where modern, data-enriched underwriting is heading.

What Is a Sample Underwriting and Closing Checklist?

A useful title insurance commitment checklist turns review into repeatable operations. The file should move from document intake to verified facts, cured requirements, evaluated exceptions, and final pre-close confirmation.

Schedule A verification

Start with identity and land. If Schedule A is wrong, every downstream document can be wrong in a way that is expensive to unwind.

- Match the parties: Confirm buyer, borrower, lender, trustee, or entity names match the contract and organizational documents.

- Check vesting: Reconcile current owner information to the latest recorded deed and any known transfers.

- Validate the legal description: Compare the commitment against the conveyance document and survey materials.

- Confirm policy amount logic: Make sure the insured amount tracks the actual transaction structure.

Schedule B-I cure tracking

This part needs project management discipline, not general awareness.

- List each requirement separately. Don't bundle unrelated items into one task.

- Assign an owner. Seller's counsel, borrower, title officer, lender's counsel, and surveyor each need clear responsibility.

- Set documentary proof standards. A requirement is not cleared because someone emailed an update. It is cleared when the title company accepts the release, satisfaction, correction, or recording package.

- Track dependencies. Some items can't clear until another filing occurs first.

- Obtain final signoff from title. Internal assumptions don't count.

Schedule B-II risk assessment

An expert team earns its keep. Don't ask only whether an exception is "standard." Ask whether it is tolerable for this asset and this strategy.

Use a short internal memo or approval grid:

| Exception type | Review question | Decision path |

|---|---|---|

| Easement | Does it impair access, expansion, parking, or redevelopment? | Accept, seek endorsement, or reprice |

| Covenant or restriction | Does it limit intended use, leasing, signage, or operations? | Accept with business signoff or renegotiate |

| Reservation or prior right | Does it alter value, control, or long-term site utility? | Escalate to underwriting and legal |

Closing discipline: The right checklist doesn't make title easy. It makes missed steps visible before they become losses.

Data verification step

Add one final layer before approval. Cross-check ownership, liens, mortgage history, and parcel-related records against an independent data source. That helps catch mismatches between the commitment and current public record conditions, especially on files that have been open for a while or involve layered vesting.

This matters even more in lender-side workflows where collateral review touches concentration concerns. Teams following pressure points in lenders' commercial real estate loans already understand that weak diligence at file level can become systemic when repeated across a book.

A practical checklist is not glamorous. It is what keeps a commitment from becoming a claim file.

The Final Word on Title Commitments

A title insurance commitment is a conditional underwriting decision wrapped in a closing document. Read it that way and the file becomes manageable. Read it like routine paperwork and you'll miss the very issues the commitment was designed to expose.

The discipline is straightforward. Verify Schedule A like a transaction engineer. Work Schedule B-I like a cure ledger. Underwrite Schedule B-II like retained risk, because that's exactly what it is. Then confirm the commitment is still current when the deal is ready to fund.

The larger shift is just as important. Strong title practice no longer ends with document review. The more reliable model combines legal analysis, underwriting judgment, and data validation against current property records. That is how professional operators reduce friction, close cleaner, and make better decisions about pricing, collateral, and post-close exposure.

The firms that treat title commitments as dynamic risk tools will outperform the ones that still treat them as escrow paperwork.

If your team needs faster, cleaner title-adjacent diligence, BatchData gives you access to 155M+ U.S. property records, ownership history, lien and mortgage detail, valuations, and daily-updated property intelligence that fit naturally into underwriting, servicing, and closing workflows. It's a practical way to move from manual file review to data-backed decision making.